Bestway Cement Limited (BWCL) was set up in Pakistan in 1993 under the Companies Ordinance, 1984 (repealed with the enactment of the Companies Act, 2017). The company is a subsidiary of Bestway International Holdings Limited (BIHL). The former produces and sells cement at its manufacturing plants located at Hattar, Farooqia, Chakwal and Kallar Kahar.

Shareholding pattern

As at June 30, 2021, over 60 percent shares are held by the associated companies, undertakings, and related parties. Within this, Bestway International Holdings Limited, Guernsey is a major shareholder holding over 56 percent shares. The local general public holds over 21 percent shares, while the directors, CEO, their spouses and minor children own 17 percent shares. Within this category, the Chairman holds 3.6 percent shares, director Mr. Dawood Pervez holds 6.3 percent shares and director Mr. Haider Zameer Choudrey holds another 3 percent shares. The remaining roughly 1 percent shares of the total shares, are with the rest of the shareholder categories.

Historical operational performance

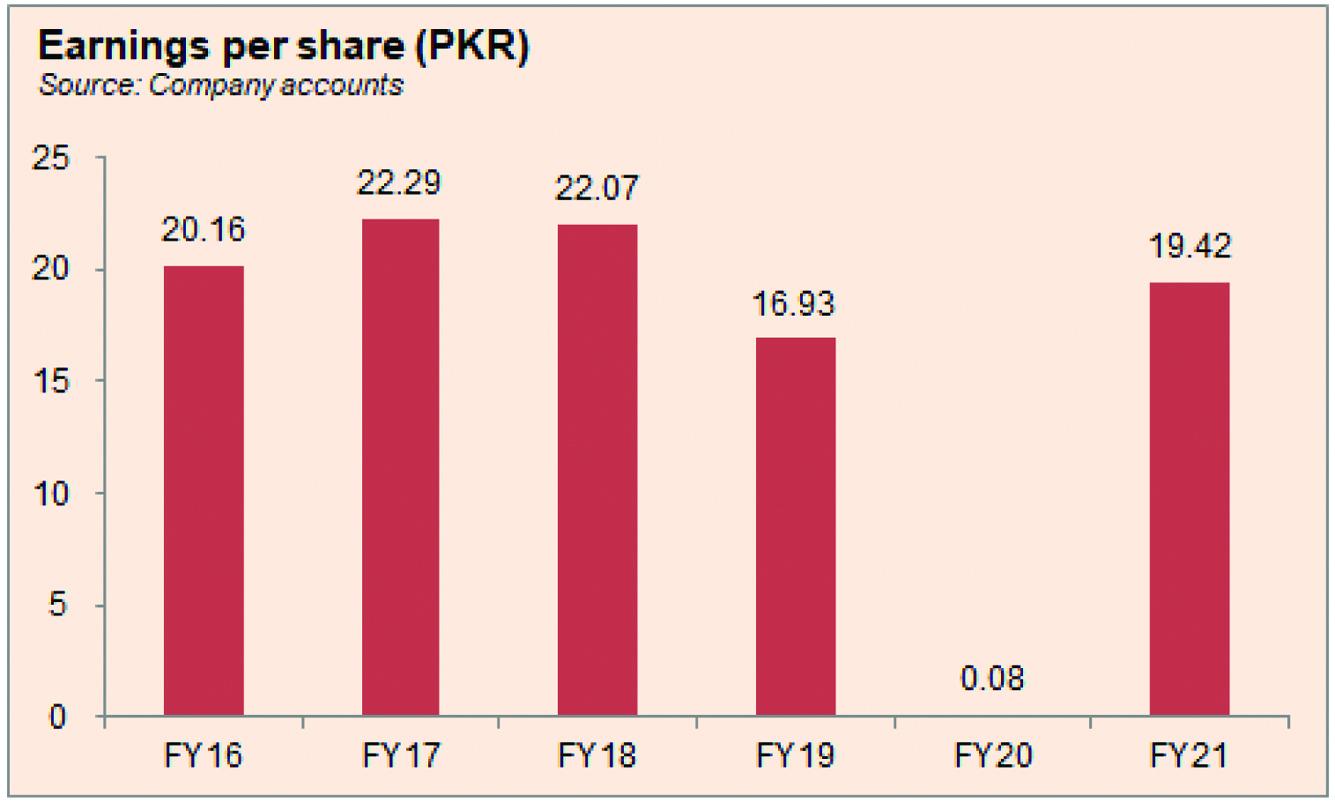

Bestway Cement has largely seen a growing topline with profit margins, in the last six years declining after FY16 till FY20, and improving recently, in FY21.

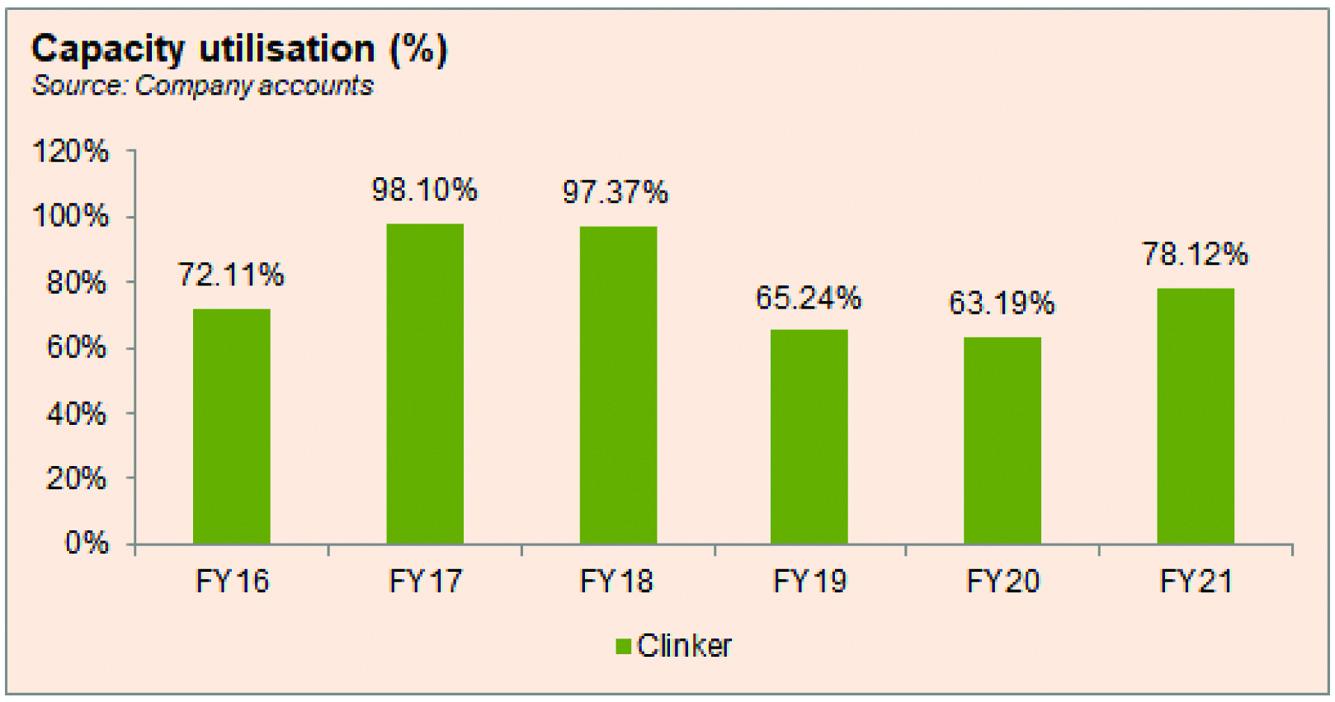

Revenue in FY18 grew by a marginal 2.4 percent, to reach nearly Rs 53 billion, while export sales remaining more or less flat, the increase was majorly seen in sales revenue. The company’s cement dispatches were higher by 15 percent while the clinker sales by Bestway Cement dominated 60 percent of the industry’s clinker sales. Despite the rise in volumes, revenue growth was relatively subdued due to lower selling prices and higher excise duty and sales tax. Moreover, cost of production increased to over 64 percent of revenue that reduced gross margin to almost 36 percent. This was largely attributed to the rise in energy costs. However, the decrease in net margin was more contained at almost 25 percent, due to a major reduction in tax expense that was nearly Rs 5.4 billion in FY17, versus Rs 1.8 billion in FY18.

In FY19, revenue grew by a lower rate of 1.36 percent. Local sales continued to dominate the revenue pie, with majority of the increase seen in local sales, while export sales saw a reduction of 23 percent. The decline in exports is attributed to imposition of import duty of 200 percent and restriction by the Indian government since February 2019. The company’s overall cement dispatches reduced by 5 percent. On the other hand, cost of production further increased to 70 percent of revenue due to rising input costs. Thus, gross margin fell to nearly 30 percent. Net margin saw a greater decrease year on year to 18.8 percent due to a rise in finance expense coupled with a higher taxation expense of Rs3 billion.

In FY20, the company saw the biggest contraction in revenue by almost 31 percent to reach Rs37 billion. The company witnessed a 10 percent reduction in total cement dispatches due to a reduction in export sales volumes as well as local sales. This in turn, was attributed to excess capacity coming from industry expansions and halt in exports to India. It was further worsened by the outbreak of Covid-19 that resulted in lockdowns. Thus, gross margin fell to an all-time low of 3 percent, whereas the bottom line was also at its lowest at Rs 49 million with a net margin of less than 1 percent.

Revenue bounced back in FY21 as it experienced a growth of over 53 percent to reach an all-time high of almost Rs 57 billion. The company’s total cement dispatches grew by 18 percent due to pent-up demand from last year, the construction package announced by the government, among other reliefs that provided a boost to the economy. Prices also improved that also contributed to improved profit margins. Gross margin rose to over 29 percent as cost of production reverted to a level near 70 percent of revenue. This also trickled down to the bottomline, with a net margin of over 20 percent.

Quarterly results and future outlook

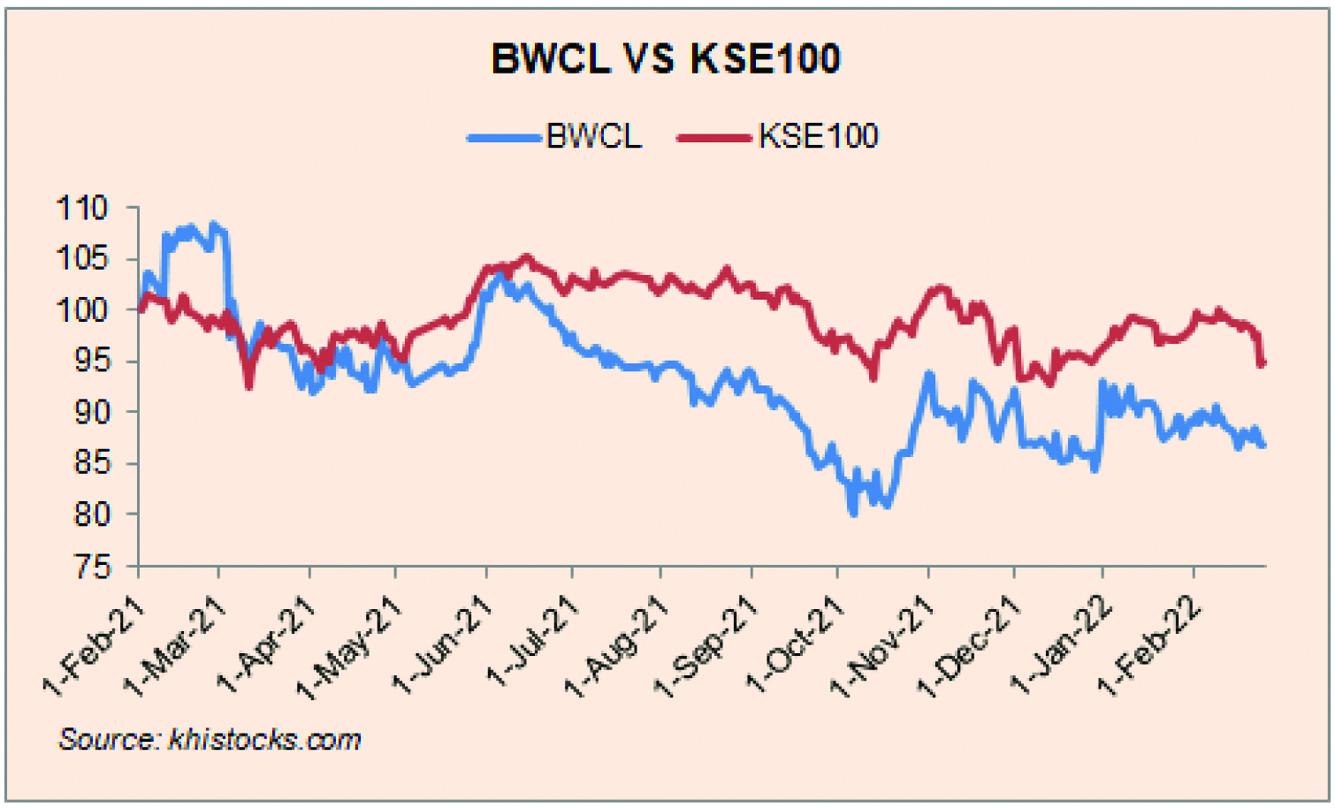

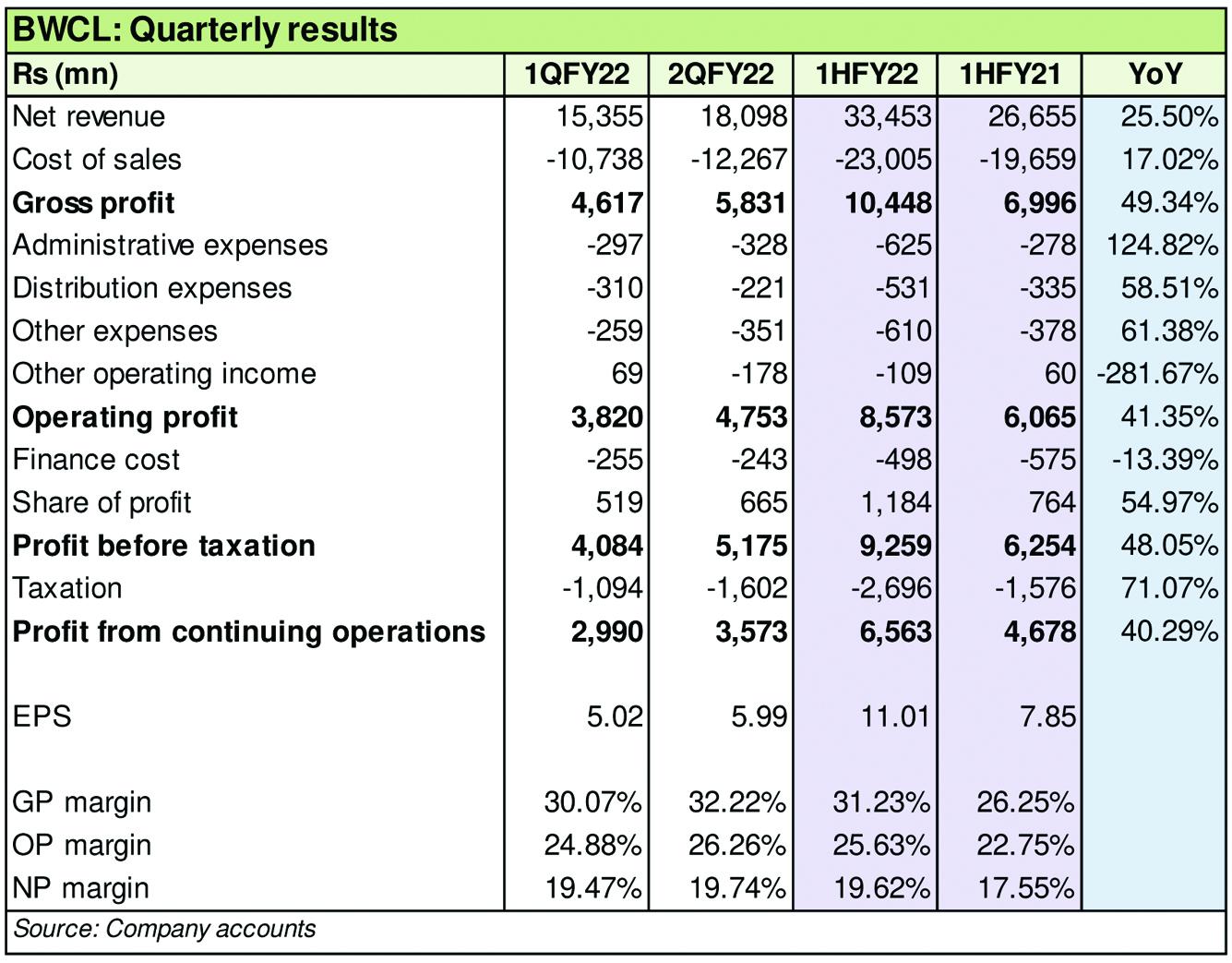

Revenue in the first quarter of FY22 was higher by nearly 27 percent year, while cement dispatches was lower by 7 percent. Export sales by the company fell by 51 percent owing to political instability in Afghanistan. For the industry too, exports were lower due to rising cost of inputs that made the products uncompetitive in the international market. Thus, the increase in topline for the quarter was attributed to an increase in selling prices. This also reflected in the net margin that was higher at 19.6 percent for 1QFY22 compared to 16.5 percent in 1QFY21. For the second quarter of FY22, revenue was higher by over 24 percent year on year. However, net margin for both the periods is same at 20 percent, whereas cumulatively, net margin at 19.6 percent for 1HFY22 is higher compared to 17.5 percent seen in 1HFY21. While prices have fared well, the industry faces challenges of rising input costs due to dependence on imports for energy that is worsened by currency depreciation.

Comments

Comments are closed for this article.