December numbers are not available yet, but by November, cumulative auto sales (including passenger cars, LCVs and SUVs) grew 65 percent year on year. Auto financing is at its very peaks with share of auto loans in consumer financing at its highest ever—44 percent—in Nov-21. In addition to all that, this government has come out with a fresh new policy on automotive development which is meant to boost volumes and localization. This set of information has all the makings of an expanding industry, except, maybe not really!

Demand for vehicles had become really robust earlier this year due to slashed car prices (as a direct result of government cutting back on FED and sales tax) together with cheaper cost of borrowing due to lowered interest rates. But since July, the month-on-month sales do not instill quite the same confidence. In the month of Nov, sales for passenger cars have dropped 24 percent compared to July, 16 percent for SUVs, and 23 percent for LCVs. After cutting down prices, nearly all the OEMs (old and new alike) raised price last month after a round of rupee depreciation. The higher cost of imported inputs (CKD kits and other parts) clearly began to pinch automakers. Any “affordability” that consumers could enjoy in July, was retracted only 4 months later.

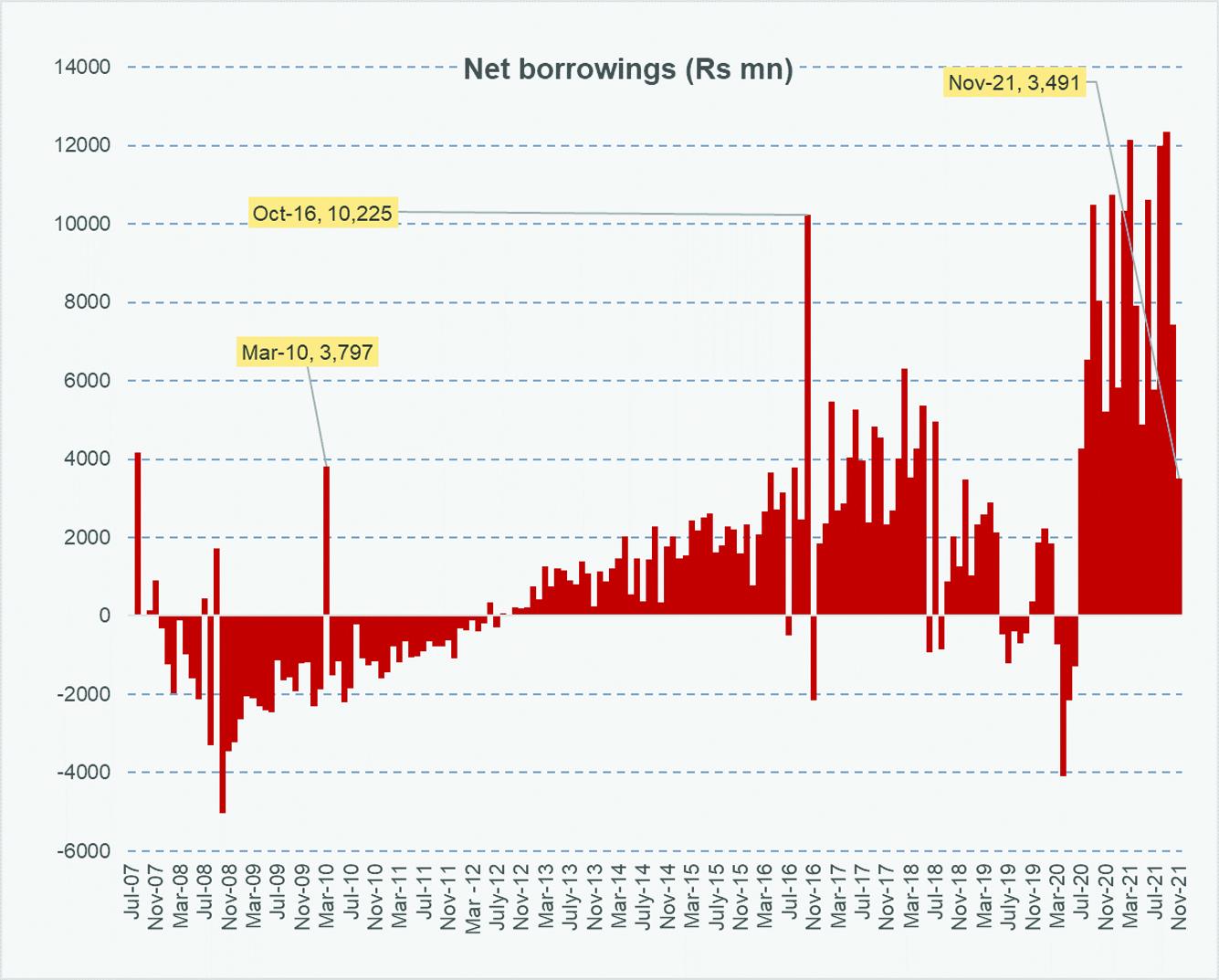

At the same time, policy rates have now gone up. A simple analysis of increased car price since July and higher interest rates charged on auto financing shows that a Suzuki Alto 660 buyer would be paying Rs5,000 per month more against an auto loan today. The same is about Rs8,400 for Cultus, Rs7,000 for Picanto A/T and Rs9,500 for Corolla. Naturally, expensive cars will bear the higher burden but even vehicles in the affordable category—which is a segment the government is heavily trying to boost—will become expensive to buy. Since demand for this segment is more sensitive to price and income changes, the dual effect of price increase and interest rate hike would affect demand. Preliminary, one can argue looking at data that there is a clear relationship between Kibor movements and overall car sales (as depicted in the graph) and while the affect of higher interest rates may be delayed, it eventually materializes in reduced demand. Already, after SBP slapped new restrictions on auto financing, data shows net borrowings thinning out.

While some measures under policy such as FED and sales tax cuts were already implemented during the budget period, other measures such as cuts in additional customs duties, WHT, additional sales tax etc. could potentially coax car makers to bring down prices. The grapevine however suggests that the FBR may be raising FED on cars and taking back some of the earlier implemented measures to shore up its revenues. If that happens, car prices will go up, not down. But even if that were not the case and the new auto policy measures go through, evidence from the last similar exercise suggests, such price declines only last a few months, as they are an outcome of tax cuts, rather than market forces. Automakers dependence on expensive imported content (and stagnant localization) makes car prices very responsive to rupee-dollar parity. When rupee depreciates, cost of imports rises which pushes OEMs to raise prices.

Inevitably so, the larger goal under the policy of substantially enhancing localization within the industry can only come when significant volumes are coming in. But, such dramatic changes in the way the market forces function will not happen overnight. Right now, no matter what hopefuls are saying, incremental car volumes will continue to weaken.

Comments

Comments are closed for this article.