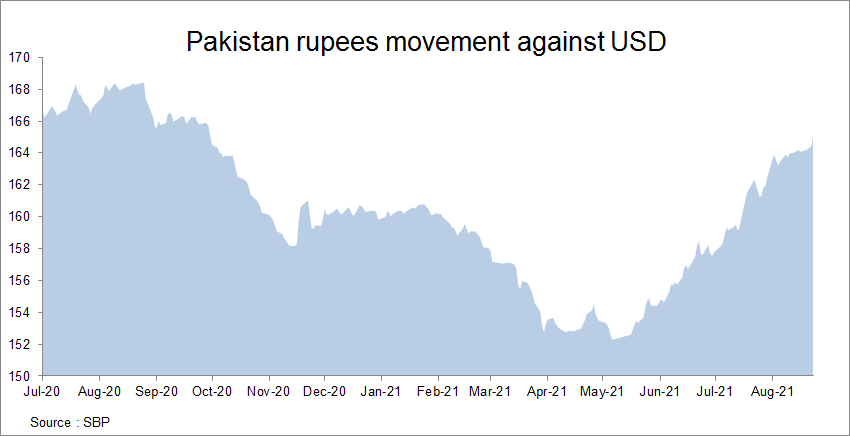

The pressure on PKR depreciation persists as the currency moved from its recent peak of 152.28 to 165.2 in fourteen weeks. The prime reason for the pressure is dwindling current account deficit. Though, the number is falling in the manageable range, the reliance of funding on short term liabilities is making the market uncomfortable. With flexible exchange rate regime, SBP is only managing the volatility, but not the direction.

Market worries are not at the ongoing level of CAD, but it is on the building levels of imports. The risk to the growth in remittance with global travel re-opening as well as the risk of global interest yields moving up are both keeping market participants on foot along with higher commodity prices. The market (banks) is not really seeing interest hike anytime soon (based on secondary market yields). The market believes that imports in the short term need to be curbed through currency adjustment, or by fiscal measures.

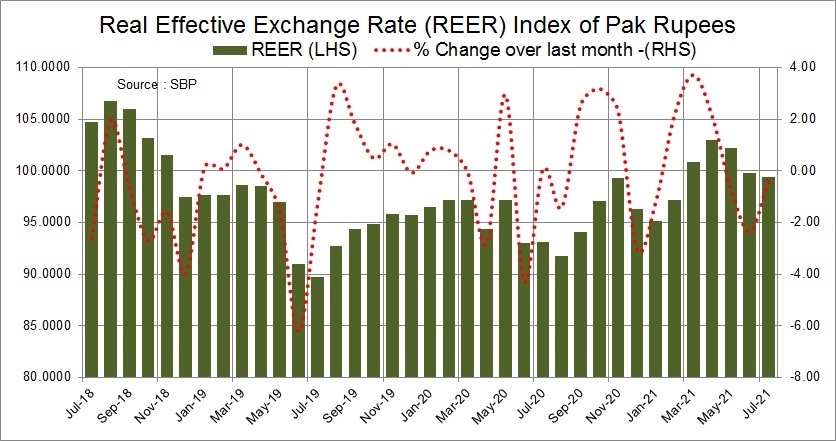

Having said that, the movement of currency in the last two working days is perhaps due to the Real effective exchange rate (REER) number of July 21, and the market was expecting REER to come down to 97-98 due to some depreciation in July, but the reported number stood at 99.42 – just a few basis points (bps) better than June number. That is making the currency adjust.

Some people are surprised on the currency movement yesterday after receiving $2.75 billion from IMF under SDR allocation. They say if reserves building is the case, why let the currency depreciate when the country is sitting at an all-time high reserve level in the history. Another set of people wonder why SBP is financing current account from its reserves – which is building on debt –and not letting the currency find its real value, also allowing the market to finance it. Between the two extremes, the market is moving in between.

First people need to realize that there is no way to finance current account deficit without dwindling reserves or raising debt in the absence of foreign investment – direct and portfolio. Even, if banks are making oil payments by themselves, these will be reduced by the inflows of remittances and exports to the SBP. Pick ear from one side or the other, the outcome is same. The key to keeping reserves high is to curtail current account at manageable levels. That is done by curbing imports in the short run and the tools SBP has are the exchange rate and interest rates. The rest falls in the domain of ministry of finance.

SBP is using its first line of defense i.e., currency. Its depreciation in the last two months would have an impact in the next 2-3 months. And based on that and other factors, SBP would have its next line of action. Meanwhile, policy makers in Islamabad should see what they have in the kitty to cut import. MoF is jubilant about better performance of FBR. FBR’s better performance is due to higher imports – both due to international prices, currency depreciation and growing volumes. Growing imports is a worry for SBP. They both should come on one page. MoF must curtail the demand through taxes and duties.

The other factor which not many are realizing is the wealth effect of real estate boom. The prices in cities like Islamabad and Lahore are doubled in the last year or so in many areas. That has boosted the demand for those who have become overnight (over year) rich. This needs to be curtailed through applying capital gain taxes and higher tax on holdings of empty lands. Then lower interest rates are further fueling the asset bubble. This must be checked.

Under the current circumstances, SBP must protect reserves. These should be built further to have sustainable growth. The short liabilities need to be converted to long term debt and investment. The business as usual cannot continue. The only different (and better) policy then the past is flexible exchange rate, and it’s hard for people to digest it.

Right now, the CAD is at manageable level despite growth in imports. This is due to continued better remittances. The prime reason for exceptional remittances growth lats year was restricted travel – especially to Middle East – UAE and KSA. This space is not a health expert to comment on when the travel will open, but once it does, the remittances flow from formal channels will surely get tested. That can slip current account. That risk must be managed by bringing some imports down.

The other risk is of global yields which are still too low. There are inflationary pressures, but the world is not responding yet with monetary tools. Sooner or later, there will some pressure on the yields and that may put pressure on interest rates at home, and in absence, on the currency. Then the inflows – like RDA, can be tested with better returns in the host country.

Things are uncertain, but there is no panic call. SBP is letting the currency to move a bit to have smooth landing. In the past, Pakistan never had a smooth transition from boom to bust and that is why higher volatility in interest rates, exchange rate, inflation, and economic growth. Slow adjustments are warranted to not let the history repeat itself.

Nonetheless, there is no immediate pressure on currency to go further south. The remittances flows are better usually around the month end. This may ease some pressure of depreciation in the next few days. But the overall direction is of slow depreciation unless global commodity prices revert. The PKR/USD may hover around 163-168 in the next few weeks.

Comments

Comments are closed.