Archroma Pakistan Limited (PSX: ARPL) is a subsidiary of Archroma Textiles GmbH. It manufactures, imports, and sells chemicals, dyestuffs and coating, adhesive and sealants. Some of the company’s key markets include apparel, home textiles, technical textiles, carpet and transportation.

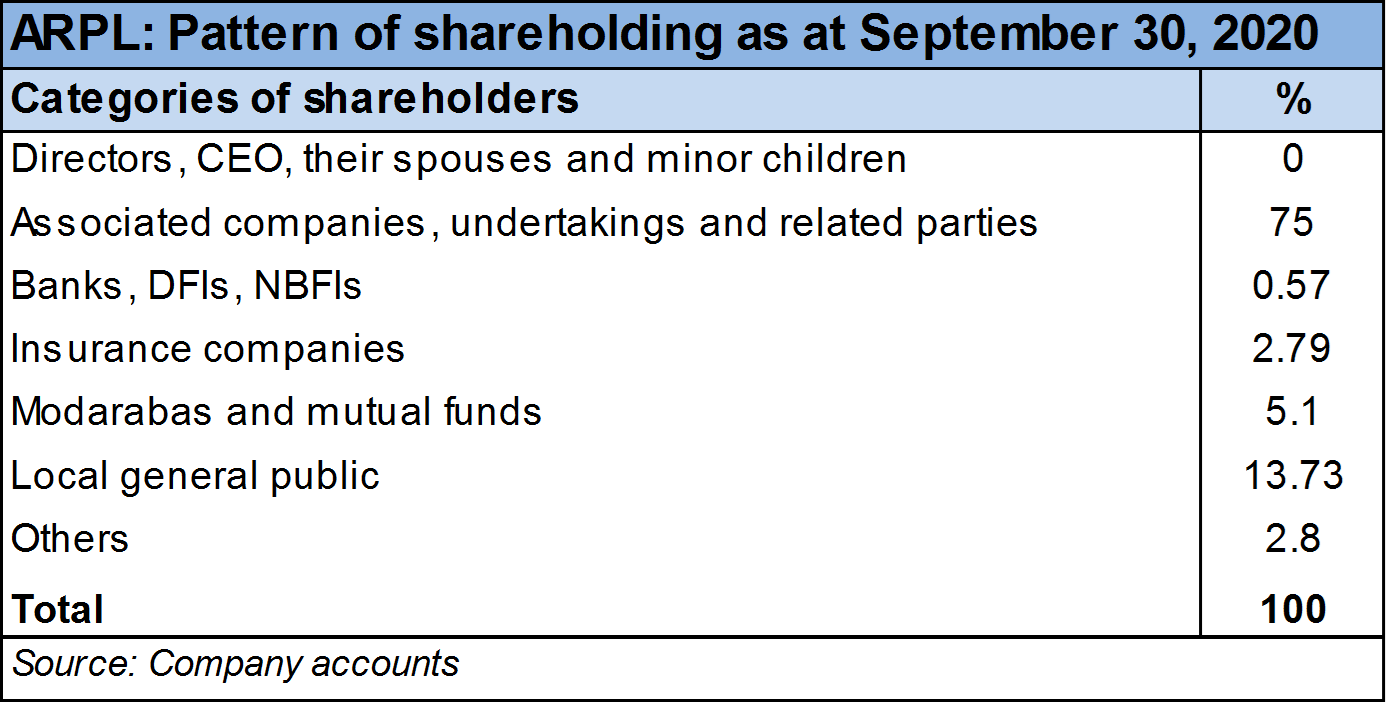

Shareholding pattern

About 75 percent of Archroma Pakistan’s shares are held under the category of associated companies, undertakings and related parties; this solely includes Archroma Textiles S.A.R.L. close to 14 percent shares are held by the local general public followed by 5 percent held in modarabas and mutual funds. The directors, CEO, their spouses and minor children hold negligible shares in the company. The remaining about 6 percent shares are distributed with the rest of the shareholder categories.

Historical operational performance

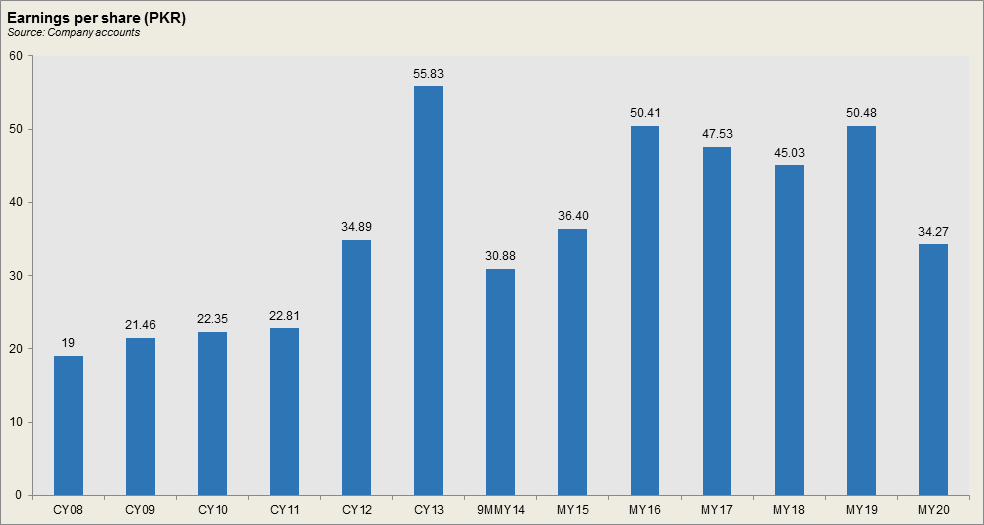

Throughout the decade, Archroma Pakistan has mostly seen positive growth in topline, with the exception of a few years whereas profit margins have largely remained stable, reaching a peak during MY16 and has been on a gradual decline since then.

The company’s financial end is in September. During M16, the company witnessed about 28.6 percent growth in its topline. This was brought about by increase in local sales in textiles and emulsion divisions. In value terms, emulsion division contributed the highest to the total revenue pie, while textile division saw the highest growth in its sales- almost 36 percent. During MY16, the decision and approval to amalgamate Archroma Textiles Chemicals Pakistan Pvt Limited (ATCPPL) into Archroma Pakistan Limited also took place. Cost of production as a percentage of revenue went down significantly to 67.7 percent, from last year’s more than 71 percent. Thus, gross margin peaked at 32 percent. This was also reflected in the bottomline as net margin was also recorded at its highest of 15 percent.

Topline growth was a little subdued close to 8 percent in MY17 when compared to that seen in the previous two years. Textile division was the major contributor to the total revenue pie whereas export sales also picked up notably; total export sales saw growth of 49 percent. There was a marginal increase in cost of production that reduced gross margins to similar effect. However, administrative cost’s consumption of revenue increased that further squeezed profit margins; salaries expense and outside service charges was mostly responsible for the increase in administrative expense. Thus, net margin was a little lower at 13 percent during MY17.

The company was back to its double-digit topline growth in MY18 as net sales grew by almost 17 percent. While brand performance and textile division were still the biggest contributor to the total revenue, export sales had gained tremendous momentum as they saw growth of more than 50 percent. Despite the significant inflationary impact, currency depreciation and increase in interest rates, it is commendable that the company maintained its cost of production at roughly 68 percent which kept gross margin also stable at around 31 percent. However, distribution expense jumped to claim 10 percent of revenue; this was largely due to royalty charges. In addition, finance cost also rose due to exchange loss and high short-term running finances. Thus, net margin decreased to 10.75 percent.

In MY19, topline grew consistently- at 21.4 percent. Brand and performance textile specialties continued to dominate the total revenue; export sales also continued to increase, reaching Rs 4 billion for the year. While cost of production increased slightly to 69 percent of revenue, keeping gross margin close to 31 percent, other elements also remained more or less similar. However, net margin was adversely impacted due to impairment loss on trade debts recorded at Rs 143 million during the year that previously stood at Rs 60 million. Thus, net margin decreased to almost 10 percent.

Recent results and future outlook

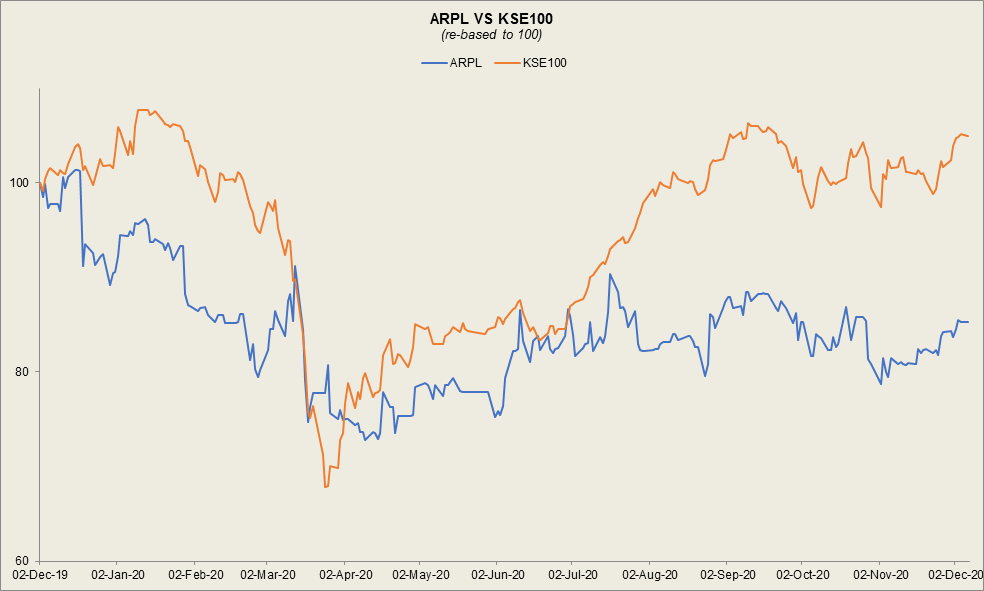

The company recently announced its MY20 results that showed a topline contraction of 13 percent, after experiencing rising revenue for five consecutive years. The decrease was seen in local sales of “others” category that are the non-core business activities of Archroma Pakistan while export sales of brand and performance textile specialties division reduced significantly; the decrease in export sales offset the minute rise in local sales of the same. During the year, with the onset of Covid-19 in the country, the company shifted its strategy to “cash collections over sales” in light of liquidity difficulties witnessed globally, given the reduced business activity during Covid-19.

Cost of production was also higher at 72 percent that brought gross margin to 28 percent, lowest seen since CY11 (financial year changed in MY14). Operating and net margin was further lowered due to increase in administrative expense brought about by salaries expense and legal and professional charges.

With the outbreak of a pandemic, consumption patterns have changed, for instance, preference for denim and casual wear as opposed to fashion and clothing. Moreover, the company also has a good flow of orders in the pipeline that would allow sales improvement in the first quarter of MY21.

Comments

Comments are closed for this article.