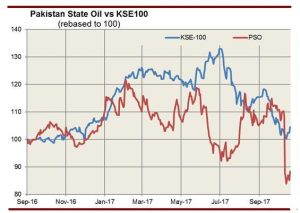

FY17 was a year of focus on retail fuels for the OMC segment, and the theme will continue in 2018, so it seems. Pakistan State Oil (PSX: PSO) is also matching the industry’s burgeoning retail sales. The firm’s top-line boasts as increase of 34 percent year-on-year, which largely comes from the increased volumetric sales.

Trend in recent quarters and the monthly volumetric sales numbers from Oil Companies Advisory Council (OCAC) show that PSO has seen its motor gasoline and high speed diesel volumes grow, while furnace oil volumes have taken a backseat. This has been due to increase in LNG usage in the power sector, which along with coal is likely to eat away a major chunk of furnace oil’s share by 2020.

Both motor gasoline and petrol sales are expected to have risen by around 30 percent, year-on-year for PSO. The increase in sales revenue was however, matched by a higher rise in cost of products sold due to inventory losses in the diesel segment.

While the margins shrunk in 1QFY18 versus 1QFY17, the firm’s earning for the quarter up by 15 percent year-on-year, were slightly higher than the market expectations. This was after a significant decline in finance costs, which came from the OMC’s recent payment of its short-term borrowings against the maturity of PIBs that it subscribed to under the partial circular debt resolution plan of the government.

PSO’s overall market share in FY17 at 55 percent has been lower compared to 65 percent in FY11-12. However, it has planned capex, which according to Elixir Securities is around Rs40-45 billion over the next three years as a growth strategy to combat any decline amid intensifying competition. In FY17 alone, PSO built and commissioned over 60 retail outlets in line with its New Vision Retail Outlet program. The OMC also plans to secure its supply chain through backward integration by doubling the refining capacity of PRL.

Praise and criticism for PSO go hand in hand. PSO is going all out for retail network, storage and pipelines, which however can be disrupted by built of circular debt. Despite lower oil prices, circular debt continues to haunt PSO and the receivables build-up showed no respite. Also huge capex plan will also strain the firm’s balance sheet. But where the increase in receivables is a concern for the OMC as circular debt intensifies the extent of this threat can somewhat be restrained as the firm makes a strategic shift in its fuel mix i.e. away from furnace oil and towards retail.

Comments

Comments are closed.