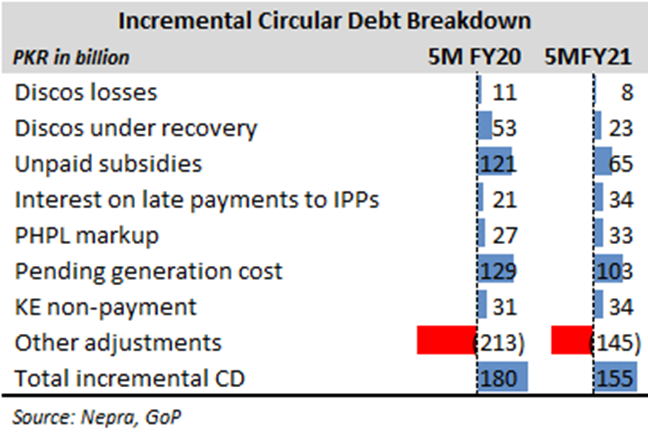

The circular debt stock had crossed Rs2300 billion by November 2020. The incremental flow of circular debt in five months of FY21 stands at Rs155 billion – slightly lower than Rs179 billion accumulated in the same period last year. The pace of growth may have slowed down slightly but remains worrying at Rs31 billion per month.

The key contributing factors remain age old – delays in tariff notifications, unbudgeted and unpaid subsidies, and the ever-present under recoveries and distribution losses at the power discos. Combined, they account for three-fourth of the circular debt accumulation. The failure to timely determine, and notify the impact of quarterly tariff adjustments alone caused Rs103 billion towards circular debt in Jul-Nov FY21.

The IMF clearly wants the power tariffs to be revised upwards, as has been confirmed by none other than the man steering the power sector – Tabish Gauhar, the SAPM on power. How much political capital the government has to undertake a base tariff revision exercise is anyone’s guess, but it surely will not be a walk in the park.

Recall that the government has openly opted for cheaper power to industries, and considerably cheaper for export-oriented sectors. Bulk of the domestic sector consuming up to 300 units is also largely insulated from price increase. Then the agriculture consumption for tube wells too is heavily subsidized and would need a massive increase for it to be anywhere close to the average national tariff, let alone the generation cost. There is very little room for the government to come close to the average distribution cost of the system.

While efforts are underway to clear some of the circular debt stock as negotiations with the IMF have entered a meaningful round. But mind you, the efforts to clear Rs450 billion stuck, must not be confused with reforms or a step that will arrest the build up of circular debt going forward. Yes, part of the incremental flow will slowdown with reduction in interest charges on late payments, altered indexation agreed upon by a few IPPs, and take and pay mechanism in other cases.

That said, the core of the problem would require more commitment from the government’s end. It is no secret that the bleeding of discos, especially that caused by under recoveries continues to be a major problem. Add the distribution losses over and above the allowed limit by the regulator, and you have a Rs170-200 billion in incremental circular debt stock.

The other major issue is the unpaid and unbudgeted subsidy. In FY20, the government ran a differential of Rs135 billion in terms of subsidy claims versus subsidy disbursed. In the five months of FY21, the unpaid subsidies over and above the amount budgeted already amount to Rs65 billion. There is a visible lack of planning and coordination, as various support schemes announced mid-year often remain unbudgeted and unpaid.

For the flow of circular debt to be arrested, the aforementioned key issues need serious focus. Negotiating with the IPPs is a herculean task and must be lauded, but that will only do very little to stem the flow of circular debt. Budgeting realistically, reforming discos and notifying timely tariffs are the answer to the circular debt question.

Comments

Comments are closed for this article.