The SBP and the government have signed a new deal where the government will finance a mark-up subsidy for housing finance under the Naya Pakistan Housing Program. In July, the government had announced a cash subsidy for 100,000 houses amounting to Rs30 billion (read more: “Naya Pakistan Housing: The plot thickens”, July 13, 2020). The mark-up facility will further bring down the monthly payment that households can pay for up to 20 years via mortgage, instead of paying upfront to the developer in 3-5 years, which is the typical scenario.

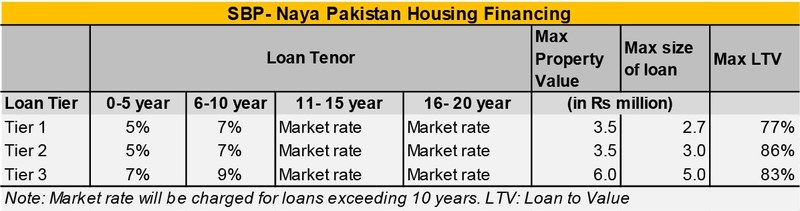

For certain, the subsidized facility at concessionary rates of 5-9 percent across loan tenors of up to 20 years (though subsidy will only cover up to 10 year of the loan), will make first-time home purchases more affordable, given the alternative. However, in the interest of transparency, two questions need to be revisited that question the efficacy of this scheme.

One: about 2 million applications were received by the Naya Pakistan Housing Development Authority (NPHDA); of which 1.6 million were long-listed (based on some mysterious criteria by NADRA, assumingly just eliminating multiple applications from the same households and so on.) for a lucky draw. A decided 100,000 households will be selected from the 1.6 million total; the “lucky” ones will be eligible to purchase a house built under the various projects of the scheme. However, the authorities are hush-hush on the eligibility criteria of this entire scheme.

Aside from the fact that the government has no idea where the demand exists (no substantial research backs the innerworkings of this scheme) and the property values assigned under this program are fairly arbitrary; how is the government whetting applicants and what is the wealth/demographic/geographic criteria for the award across which the two types of subsidies will be awarded.

If low-income is the target market for this scheme, what is low-income? And why is that not defined? Last checked, the SBP defined a “low cost” house to value below Rs 3 million; whereas property values under the subsidized scheme can go up to Rs 5 million.

Two: What is affordability? Once again, the government can claim to “boost affordability” through a one-time cash subsidy and a long-term financing facility but there is no understanding of what affordability means for a Pakistani household. Without this understanding, how can any subsidy be targeted enough?

Subsidies are temporary and often inefficient, but most of all, they can be discriminatory. Since there are limited funds available, the government needs to be up front about the mechanism and the eligibility criteria. Going by the oft-quoted number of 12 million as the housing shortage in the country, if 100,000 families are availing this tight subsidy, who are these 100,000 people?

In its haste to make the program successful in numbers, the government must not forget to ensure the subsidy—and housing supply in turn across the country—is well-distributed and optimally utilized. Otherwise, what’s the point?

Comments

Comments are closed for this article.