The power regulator Nepra has finally issued hearing notices for monthly fuel price adjustments which have been long pending. The government had initially issued a notification to suspend the monthly Fuel Price Adjustment (FPA) till June 2020. The Nepra notifications and even decisions do not essentially mean that the government will not extend the arrangement to a specified or even an unspecified period, should it wish so.

Last monthly FPA was levied in November 2019, adjusted for September 2019 fuel costs. Ever since, the monthly fuel cost has mostly surpassed the reference fuel cost. The average increase since September 2019 FPA has been 83 paisas per unit – which is consistent with the preceding 12 -month average monthly FPA.

It is highly likely that the government may want to delay the notifications further. Not that 80 paisas is big deal, but because lower international oil prices have created an opportunity for the government. The last three months have seen FPAs in negative territory at an average of 53 paisas. This gives the government time to spread the pending FPAs over 12 months instead of nine, where next three months should also bring relatively stable FPAs, if not in the negative zone.

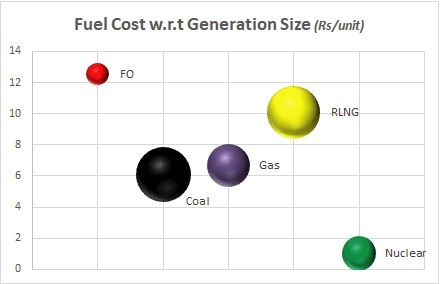

The power generation fuel cost for FY20 at Rs600 billion, down from Rs654 billion from FY19 – for almost similar level of power generation. Improved generation mix has been the biggest factor for reduced fuel cost, as coal and RLNG per unit cost stayed almost at yesteryear level, while that for natural gas went higher. Currency depreciation played its due role, and the state contract in the case of RLNG ensured Pakistan missed cheaper gas in the spot market at almost half the rate.

While the generation mix improvement and the reduced fuel price component are welcome – the other component of the tariffs that is capacity payments has not allowed the consumers to benefit from better mix. The central bank had also lamented the very fact earlier in these words, “If we compare the tariffs between 2013 and 2018, it becomes clear that while the fuel charges have certainly softened due to lower oil prices and a shift in domestic fuel composition, capacity charges have actually increased. For nearly all the discos, the increase in capacity charges have completely offset the fall in fuel charges”

The problem is twofold at this level. One is the capacity charge, which is going to stay on the higher side (unless there is large scale withdrawal of contracts and revision in policies, which is highly unlikely). Second is the demand, which has failed to be meet the capacity additions. Consider this: for the capacity cost to not increase from FY20 levels, the energy dispatched should have grown by at least 30 percent year-on-year. It did not even grow by 1 percent.

Looking at how things have stacked up. Any improvement in energy tariffs will have to come from the fuel price component in the medium term however insufficient it may be. Keeping power demand at pace with capacity additions or restricting capacity charges – both appear unlikely at this point. Affordable energy bus may well have been missed.

Comments

Comments are closed.