Waves Corporation Limited (previously known as Waves Singer Pakistan Limited) (PSX: WAVES) is incorporated in Pakistan as a public limited company.

The principal activity of the company is the manufacturing and assembly as well as trading and retailing of domestic consumer appliances.

The company is also engaged in the trading and retailing of light engineering products.

Pattern of Shareholding

As of December 31, 2024, WAVES has a total of 281.406 million shares outstanding which are held by 6408 shareholders. Local general public have the majority stake of 52.07 percent in the company followed by Directors, CEO, their spouse and minor children by holding 40.17 percent shares.

Joint Stock companies account for 4.55 percent of the outstanding shares of the company. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

Over the period under consideration, WAVES’s topline posted an uptick only in 2019 and 2021. Conversely, its bottomline posted a downtick in 2019 and 2020 followed by a staggering rebound in 2021. In 2022, WAVES’s bottomline once again tapered off however posted growth in 2023 and 2024.

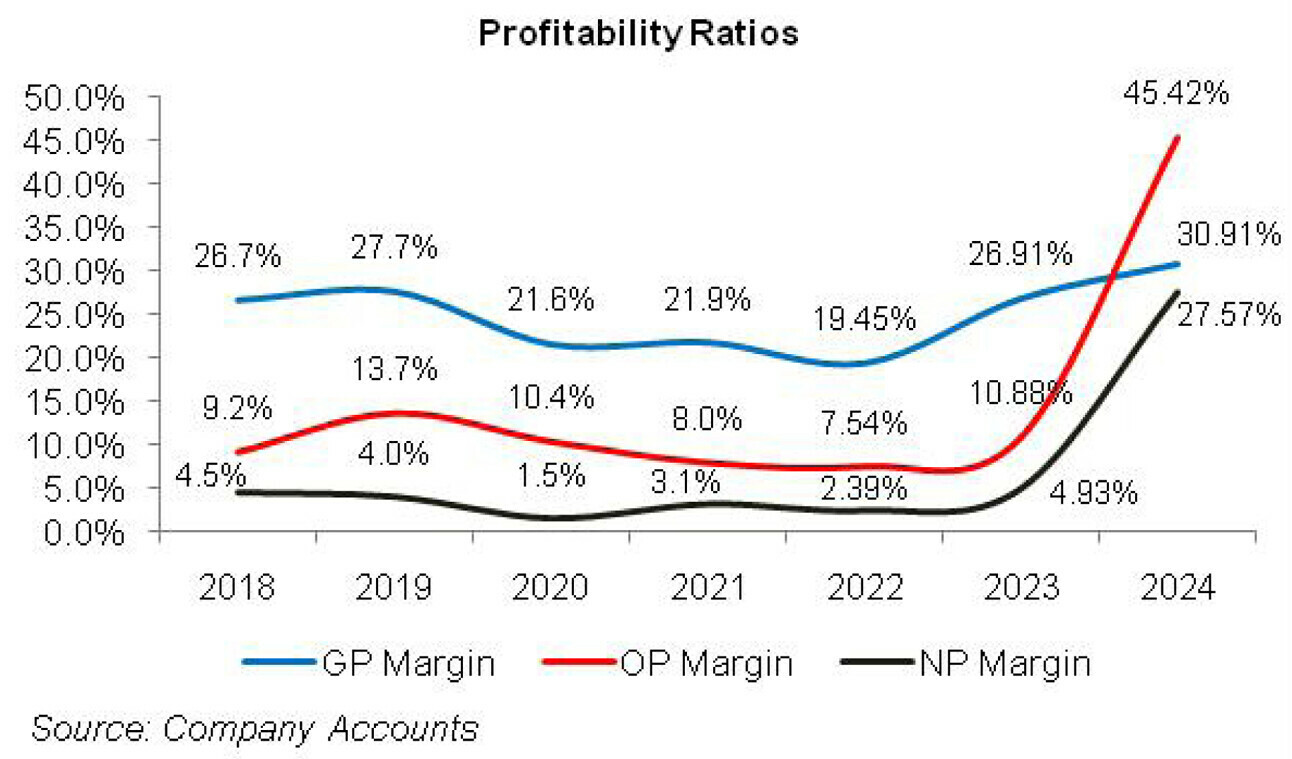

The company’s margins which oscillated over the period under consideration attained their optimum level in 2024 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, WAVES topline grew by 11.37 percent year-on-year to clock in at Rs.9483.97 million. This was on the back of rise in sales volume coupled with systematic price increase to make up for the surging cost of production on account of inflation, Pak Rupee depreciation and spike in the prices of components of appliances.

During the year, the government made it compulsory to print the CNIC of the buyer on the sales tax invoice along with the inclusion of home appliances in the third schedule of sales tax. This affected demand and pricing, yet the company was able to muster reasonable sales volume.

Gross profit grew by 15.43 percent year-on-year with GP margin growing up to 27.72 percent in 2019, up from 26.75 percent in 2018. The company undertook cost rationalization and was able to reduce its operating expense by 1.42 percent year-on-year in 2019.

Other expense also dropped by 21.62 percent year-on-year as no provision was booked against doubtful debts. Moreover, the company had incurred loss on property, plant and equipment due to fire and disposal in 2018 which created a high-base effect and culminated into shrinkage in other expense in 2019. Other income grew by 321 percent in 2019 which was the result of reversal of loss allowance against trade debts.

Operating profit grew by 65.75 percent in 2019 with OP margin climbing up to 13.70 percent, up from OP margin of 9.2 percent posted in 2018.

Finance cost grew by 101.59 percent in 2019. On account of higher discount rate coupled with increased borrowings. Finance cost was somewhat offset by 21.17 percent higher earned carrying charges. Profit before tax grew by 21.76 percent in 2019; however, 89 percent increase in tax charges mainly on account of changes in tax rate, translated into 0.99 percent dive in net profit in 2019.

Net profit for 2019 clocked in at Rs.378.3 million with NP margin of 4 percent, down from NP margin of 4.49 percent recorded in 2018. EPS also marched down from Rs.2.04 in 2018 to 2.02 in 2019.

In 2020, WAVES’s topline slid by 10.11 percent year-on-year to clock in at Rs. 8525.48 million. This was because the company’s peak summer season was compromised due to nation-wide lockdown on account of COVID-19.

Cost of sales plunged by only 2.53 percent on account of Pak Rupee depreciation, fuel price hike and an increase in the prices of raw materials and components in 2020. This resulted in 29.85 percent decline in gross profit with GP margin sinking to 21.63 percent in 2020.

The gross margin would be even leaner had the authorities not reduced the custom duties on high value imported raw materials in 2020. The operating expenses collectively dipped by 1.53 percent in 2020. Other expense also posted 49.94 percent nosedive on account of no exchange loss incurred during the year coupled with lesser provisioning for WWF and WPPF in 2020.

Other income continued to shine and multiplied by 196.15 percent in 2020 which was primarily because of reversal of loss allowance on trade debts and liabilities no longer payable written back during the year. Despite cost control and operational efficiency management, operating profit slumped by 31.76 percent year-on-year in 2020 with OP margin slipping to 10.40 percent.

Finance cost barely grew by 1.36 percent in 2020 as the SBP took monetary easing stance during the year. Earned carrying charges magnified by 37.58 percent during the year. Net profit narrowed down by 66.31 percent in 2020 to clock in at Rs.127.468 million with NP margin of 1.5 percent and EPS of Rs.0.61 – the lowest among all the years under consideration.

2021 appears to be the most fortunate year for WAVES whereby its net sales grew by 22.44 percent to clock in at Rs.10,439.01 million – the highest ever net revenue mustered by the company. Increase in urbanization and the trend of nuclear family setup with multiple sources of earning have greatly improved the lifestyle of people, resulting in a staggering revival in the demand of home appliances.

The topline growth was the result of 20 percent rise in local sales and 21.6 percent growth in the retail business. The export sales somewhat dropped in 2021 as geopolitical tension owing to Russia-Ukraine crisis spurred macroeconomic uncertainty in many countries.

Cost of sales also grew by 22 percent due to Russia Ukraine crisis which increased the prices of raw materials in the international market. Nevertheless, robust sales volume and upward revision in prices resulted in 23.75 percent growth in gross profit with GP margin slighting inching up to 21.86 percent in 2021.

Marketing and administrative expenses grew by 10.84 percent and 20.97 percent respectively on the back of higher sales volume and inflationary pressure. Higher provisioning against WWF, WPPF as well as loss allowance on trade debts and exchange loss translated into 186.90 percent higher other expense in 2021.

Other income which had been growing tremendously in the past two years slumped by 46.34 percent in 2021 on account of lesser reversals of loss allowance against trade debts. Despite a staggering growth in topline, operating profit thinned down by 6.10 percent in 2021 with OP margin contracting to 7.97 percent in 2021.

Finance cost dropped by 19.86 percent in 2021 which coupled with 47.68 percent hike in earned carrying charges culminated into 157.23 percent growth in net profit. Net profit clocked in at Rs.327.89 million in 2021 with EPS of Rs.1.13 and NP margin of 3.14 percent.

WAVES’s topline receded by 4.79 percent year-on-year decline in 2022 to clock in at Rs.9,938.67 million. Overall, the appliances industry suffered during the year due to restrictions imposed on the import of basic raw materials.

WAVES took the timely decision of switching to local raw materials which not only allowed it to continue its operations amidst supply chain impediments but also evade the negative effect of steep depreciation of Pak Rupee.

WAVES’s wholly owned subsidiary Waves Marketplace Limited (WML) showed growth in 2022 while its home appliances business which was handed over to its subsidiary Waves Home Appliances Limited (WHALE) posted a plunge due to decline in the purchasing power of the consumers owing to high inflation and discount rate.

During the year, a scheme of arrangement was signed between WAVES and WAVESAPP. Under the arrangement, the home appliances business was transferred to WAVESAPP while WAVES retailed the retail and real-estate business.

Consequently, WAVESAPP issued 199,724,956 shares to WAVES and 56,281,240 shares to the shareholders of WAVES. WAVESAPP became the subsidiary of WAVES under the arrangement. Cost of sales slid by a lesser magnitude of 1.85 percent year-on-year in 2022 on the back of a spike in fuel and electricity charges and high indigenous inflation.

Gross profit slashed by 15.30 percent year-on-year in 2022 with GP margin falling down to 19.45 percent – the lowest among all the years under consideration. Lower sales volume culminated into 6.44 percent dip in the marketing and selling expense in 2022 while administrative expense inched up by 0.64 percent during the year. O

ther expense also plummeted by 10.32 percent in 2022. While exchange loss was relatively higher in 2022, lesser provisioning against WPPF and no allowance booked against debts did the trick.

Recently, WAVES has started recording its earned carrying charges as a part of its other income. If we incorporate earned carrying charges, other income mounted by 76.73 in 2022. Operating profit slumped by 9.93 percent in 2022 with OP margin of 7.54 percent – the lowest since 2018.

The company was able to trim down its finance cost by 38.16 percent in 2022 despite multiple rounds of monetary tightening during the year. While profit before tax was 39.17 percent lesser as compared to 2021, reduction in the tax charge for 2022 due to prior year tax charge and differential under normal and final tax regime, net profit posted 27.57 percent decline in 2022 to clock in at Rs.237.478 million with NP margin of 2.39 percent and EPS of Rs.0.84.

In 2023, WAVES’s topline plunged by 47.62 percent to clock in at Rs.5,206.33 million. This was on account of overall slowdown of white appliances during the year due to shrunken pockets of consumers on account of soaring inflation.

Cost of sales declined by 52.47 percent in 2023 as lower production volumes resulted in reduced consumption of raw & packaging materials, fuel & power as well as disbursement of lesser salaries due to streamlining of workforce.

Gross profit receded by 27.52 percent in 2023, however, GP margin recovered to clock in at 26.91 percent. Marketing & distribution expense took 30.16 percent year-on-year slide in 2023 due to lower payroll and commission expense incurred during the year.

Employee headcount plummeted from 1575 in 2022 to 1236 in 2023, resulting in lower payroll expense. This pushed down administrative expense by 24.37 percent in 2023. Other expense escalated by 13.13 percent in 2023 due to higher allowance booked for ECL.

Other income dropped by 13.86 percent in 2023 due to lesser gain recorded on modification/termination of lease, lesser earned carrying charges and no reversal for ECL booked during the year.

Operating profit shrank by 24.42 percent in 2023 with OP margin inching up to 10.88 percent. WAVES was able to cut down its finance cost by 39.10 percent in 2023 despite high discount rate. This was on account of reduced working capital requirements related borrowings owing to sluggish demand.

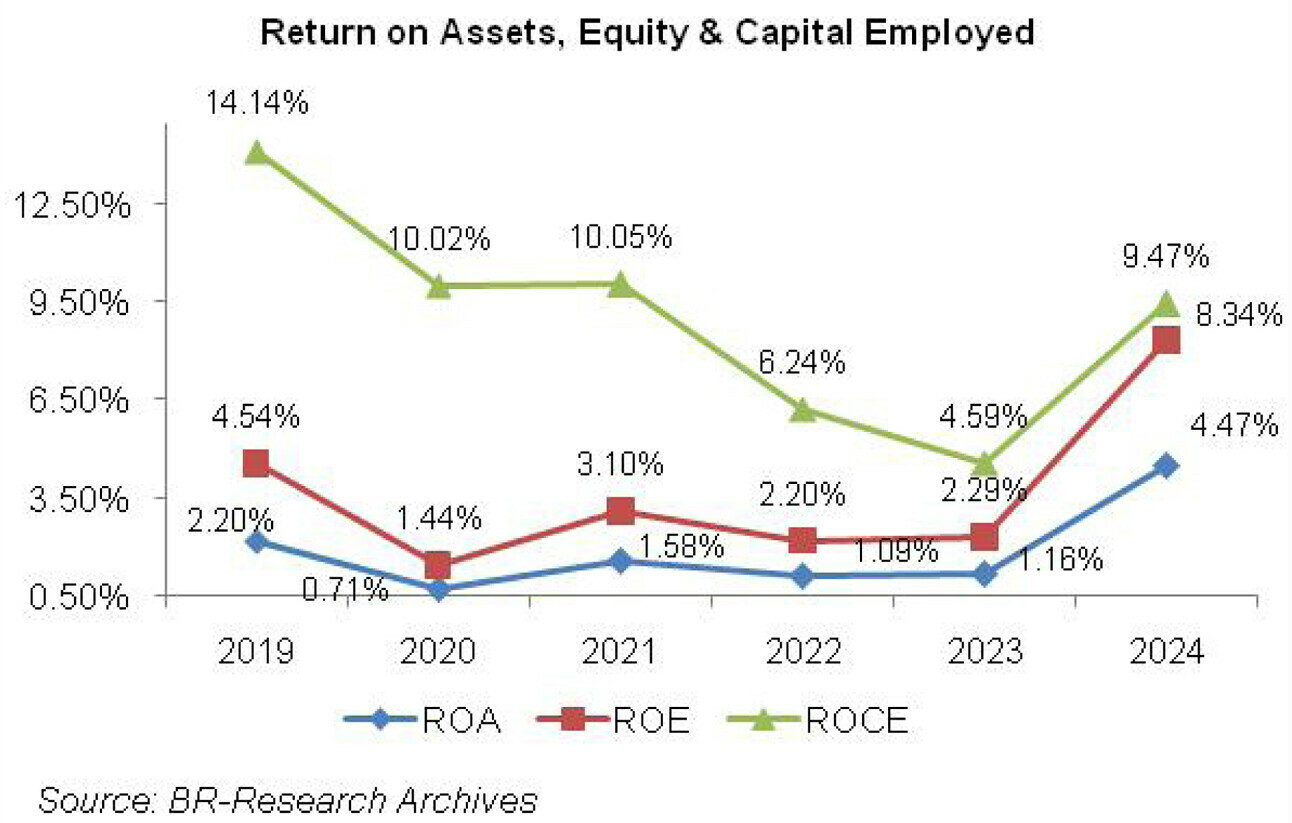

WAVES’s debt-to-equity ratio fell from 41.66 percent in 2022 to 39.53 percent in 2023. Profit before tax went down by 3.99 percent in 2023; however, the impact of deferred taxation resulted in 8.13 percent uptick in net profit for 2023. WAVES’s net profit stood at Rs.256.781 million in 2023 with EPS of Rs.0.91 and NP margin of 4.93 percent.

Net sales narrowed down by 24.23 percent in 2024 to clock in at Rs.3944.76 million. Waves Marketplace Limited, Waves Builders & Developers (Private) Limited and WAVES Appliances business suffered during the year due to subdued market demand owing to a slash in the purchasing power of consumers.

Cost of sales tumbled by 28.37 percent in 2024 due to considerable decline in raw and packing materials consumed during the year, lesser freight charges as well as fuel & power charges incurred during the year.

Gross profit shrank by 12.98 percent in 2024; however, GP margin attained its optimum level of 30.91 percent in 2024.

Distribution expense slid by 10.81 percent in 2024 due to lower salaries of sales force, lesser warranty expense, decline in travelling & conveyance charges as well as rent, rates & taxes incurred during the year.

Administrative expense inched down by 9.92 percent in 2024 particularly on the back of lower payroll expense as the company streamlined its workforce from 1236 employees in 2023 to 822 employees in 2024.

Other expense mounted by 51.33 percent in 2024 due to allowance booked on ECL and debt balances written off during the year. WAVES recorded a staggering 356.55 percent rebound in its other income in 2024 which was the effect of present value discounting of accrued markup as well as fair value gain on investment property recognized during the year.

During the year, the management of the company decided to classify its projects as investment property because of delay in the implementation of project development for an indefinite period. The discounting income will be reversed in the coming years as the liabilities unwind.

WAVES’s operating profit strengthened by 216.36 percent in 2024 with OP margin jumping up to 45.42 percent. Finance cost surged by 163.70 percent in 2024 due to higher discount rate and a massive increased in long-term financing obtained during the year. Net profit boosted by 323.47 percent to clock in at Rs.1087.394 million in 2024 with EPS of Rs.3.86 and NP margin of 27.57 percent.

Future Outlook

The changes in the weather conditions over the years call for an increase in the demand of refrigeration and air conditioning. Moreover, changes in lifestyle and increase in double income nuclear families also point towards the same.

However, the appliances industry in Pakistan has a household penetration rate well below the world average due to lower purchasing power of consumers. Steep rise in the prices of appliances coupled with sky-rocketed electricity prices keep the potential consumers at bay.

The company plans to modernize its manufacturing facilities to achieve operational efficiency and reduce its cost. Furthermore, with the decline in inflation and interest rates, the demand of home appliances and real-estate is expected to grow.

Comments

Comments are closed for this article.