If there is one sector that has had a steep V-shaped recovery during the ongoing pandemic, it’s the textile sector. The textile sector, which was massively hit by Covid-19 with both local and international markets closed down was also one of the first sectors to recover. Recovery has been two folds. Not only has resumption of the sector’s operations domestically versus the restrictions in competing regional countries diverted export orders to Pakistan, but the country has also benefitted the US-China trade war.

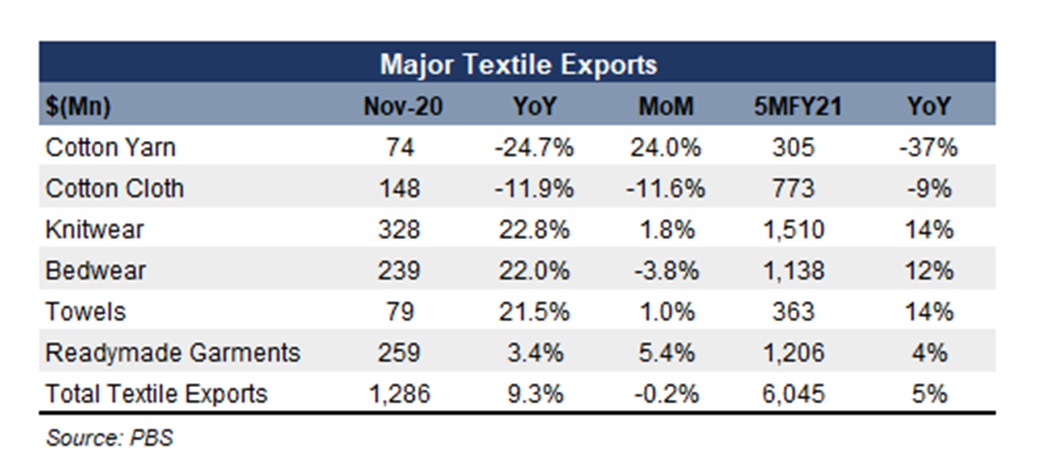

Though the month-on-month exports during November 2020 remained flat, recent export numbers from Pakistan Bureau of Statistics show that textile exports in November 2020 touched $1.286 billion, growing by over 9 percent year-on-year. The improvement in sector’s exports have been visible since June 2020, and since after August 2020 when the torrential rains impacted trade, exports have been growing for three consecutive months. 5MFY21 textile exports were up 5 percent year-on-year.

The growth in textile exports is being led by value-added segments: knitwear, bedwear and towels, while growth in the readymade garments has been tepid. On the other hand, exports of cotton yarn and cotton cloth has been declining due to low cotton production at home and shortage created as a result. Sources tell BR Research that amid the shortage of cotton the in value added segment has been able to take up export orders partially due to cotton imports that have gone up as a result of elimination of regulatory duty on them.

Growth in export value amid falling volumes particularly of bedwear and readymade garments is showing signs of shift towards value-addition. Today, the sector is operating at full capacity as exporters are reportedly fully booked for the next 5-6 months and have expansion plans to take on the growth, which means FY21 will end better for the sector. However, it’s too early to celebrate the export growth. For one, what should now be worked upon rigorously is sustaining the export volume and markets; Once the pandemic is or (or the US-China trade war miraculously ends with mutual benefits), there is a risk that the orders will pivot back to the most competitive in the region. In an interview with BR Research, MD Al-Karam Textile- Fawad Anwar highlighted two key challenges besides the delay in refund payments that must be dealt with to retain new customers and propel export growth: falling cotton productivity and volatile energy prices. The long-term sustainability of textile sector relies on what Pakistan once had a competitive advantage in: cotton production that stands halved this year versus India’s output that has doubled from similar levels. And while the new textile policy is said to be looking at the energy cost component diligently, retaining the GSP plus status expiring in 2023 should also be a priority. And last but not the least, value addition in the textile value chain is what will secure export orders now – competition is too fierce for banal and low-end products

Comments

Comments are closed for this article.