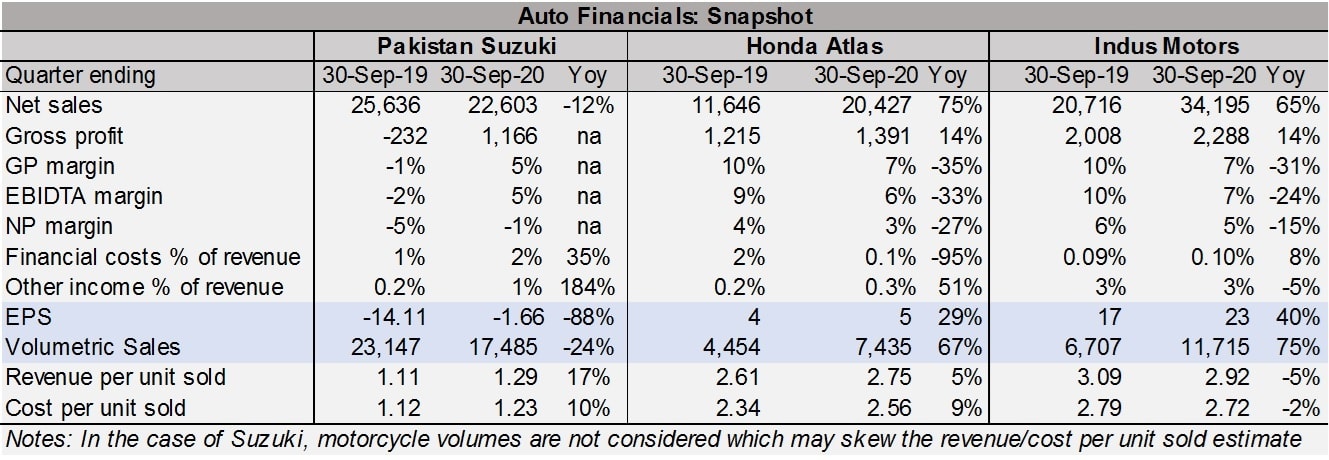

Brokerage analysts are revising their earnings forecasts for automobile companies, this upcoming growth spurt attributed to blooming volumetric sales and reduced pressure from input costs. Save for Pakistan Suzuki, that has been in losses for at least the past five quarters, prospects for Honda and Toyota are signalling happy days. What could potentially derail this progress?

Consider the industry dynamics over the last two years. Demand was growing during FY17 and FY18 but car prices were also going up. In fact, prices were raised across variants every few months as rupee depreciated against the dollar. On average, Honda prices have gone up by 51 percent, Toyota by 54 percent and Suzuki by 40 percent since Jan-18. However, the hike in car prices was higher than the rupee depreciation during this period while inflation of local parts was also lower (read more: “Car prices: One-way traffic”, Nov 18, 2020).

That indicates low level of localization—in general—and an increasing level of dollar-valued imported content for every new model that is being introduced. Soon, as economic growth receded and interest rates increased, consumer appetite to absorb the ever-rising car prices reduced. As this slump continued, the world was hit was Covid-19 which came with its own troubles leading to factory close downs and eventually the industry recording zero sales for the first time ever in April.

Six months in, many of these trends have reversed. Cities came out of lockdowns, production resumed and substantial reduction in interest rates caused cost of car lease to slide down considerably. Car buyers also have more options with offerings from Kia and Hyundai that have piqued new interest. Corporate and consumer buys has evidently recovered as sales for both Toyota and Honda have grown by more than 50 percent in the post-lockdown quarter Jul-Sep 20.

It will likely take longer for Suzuki to turn its losses into profits. Given Suzuki operates in the middle-class segment, consumers are more sensitive to price and income changes (read more: “Curb your enthusiasm”, Oct 26, 2020). The rise of Careem and Uber had inflated demand for Suzuki cars that has simmered down over the last year. Suzuki also has a strong contender in the form of Kia Picanto, not to mention, used imported cars, though the latter is also experiencing depressed growth due to government regulations.

But as Suzuki waits in the bleachers for its turn, lower cost of leasing is giving a new lease of life to mid-range and high-end auto sales evidenced by sky-rocketing auto financing numbers. Another factor multiplying optimism is a strengthening rupee which would reduce pressure on costs and spring back margins. There is no incentive for car makers to cut-down prices at this point, even if cost of imports is down, since demand is on a growth path but it should come into consideration if the country goes into lockdown again and inventories start to pile up.

Toyota seems to be the shining star and its balance sheet is testament to that. Its new launch Yaris is selling more units than all of the Corolla variants combined last year. Yaris is in the mid-range category in terms of price point which is becoming a very popular pick (side note: Toyota’s revenue per unit sold has come down-see table- primarily because of higher Yaris sales this quarter against higher Corolla sales last year). The company’s bottom-line is buttressed by virtually no finance costs, and a substantial level of other income. In fact, other income constituted 41 percent of the company’s before-tax profits during 1QFY21 against 39 percent last year.

While projections are looking good for the industry, subsequent lockdowns as covid comes calling again and shut down of factories thereafter; an upward tick in kibor; and more price hikes may curtail the industry’s growth trajectory. So far, it seems Honda and Toyota are shielded from the forces of competition due to the strength of their brands, but as the market develops and consumers get familiar with new models, some market share may get chipped off.

Comments

Comments are closed for this article.