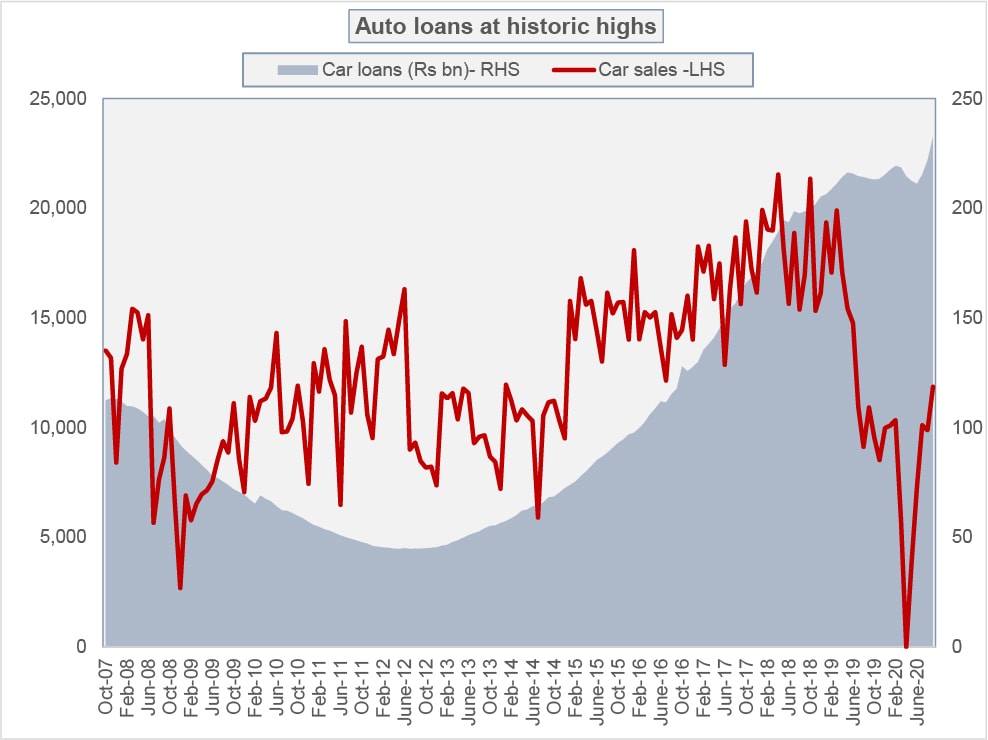

Auto loans are trailing their historic highs as November rolls in. That certainly is (good) news as the country trudges out of the covid-19 wreckage with consumption seemingly reviving against all odds. In Sep-20, car sales have grown 18 percent against the same month last year, and auto loans are demonstrably tinkering with excitement after the interest rate reduction. Numbers however point towards something curious.

Auto makers have been periodically—and without fail—raising prices since FY17 as rupee depreciated. Weaker rupee translates to expensive imports which in the case of automobiles is specially concerning since local production depends on high import content of inputs and CKD kits. In the beginning, car sales remained unperturbed, but starting FY20, volumes began to decline fast (read more: “Car prices: Is there method to the madness?” April 17, 2020).

Over the past year too, despite covid-related lockdown and reduced organic demand, automakers have continued to raise price. Sales are rising again as consumers are hankering to absorb the higher price tag (evidenced also by the increasing premiums in the market that consumers are paying once again). It helps that interest rates have declined considerably which has made auto loans really cheap. But who is benefiting from it?

Just looking at volumetric growth, one emerging trend is obvious: affordable cars are not affordable enough. If Suzuki represents the so-called affordable segment, sales are not growing. In fact, in Sep-20, Suzuki sales declined by 24 percent, against Toyota’s exceptional growth of 106 percent and Honda’s 87 percent. This is despite competitor SUV and other options being offered by new players including Kia, Hyundai and Changan in Toyota/Honda segments.

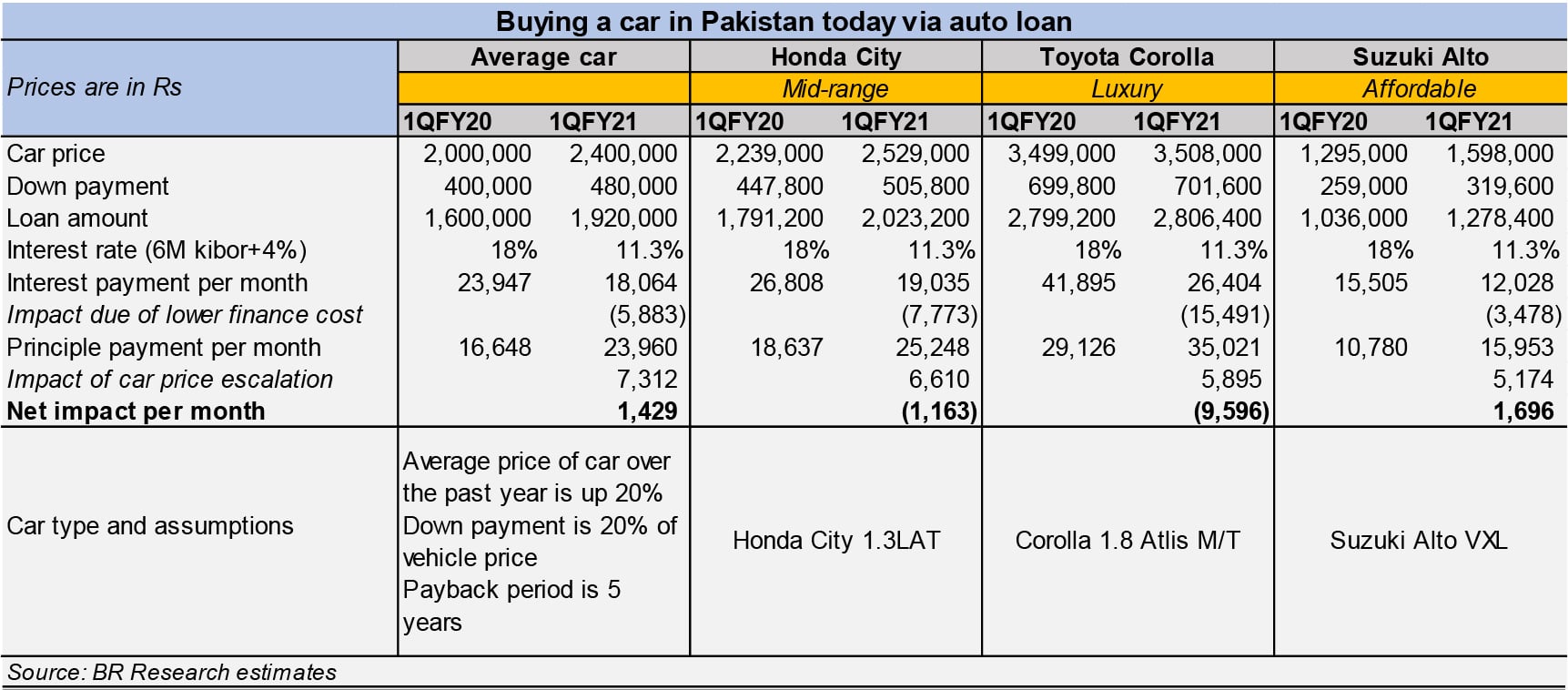

Calculations also suggest that the net impact of price hikes but reduced financing cost favors high-end cars more than the affordable segment. In fact, despite lower interest rates, an average car will incur a higher monthly charge on an auto loan today than last year due to higher prices. But in the luxury and mid-range segments, the reduced financial cost has more than offset the price hikes. There is a sense of disparity here, though the incremental burden for the affordable segment (~Rs1500 to Rs2000 per month- see table) is not too much and car buyers typically are not as price sensitive.

But wait. Let’s walk back into the pre-covid era where price hikes were more frequent—the impact then should be more visible. In Jan-18, Wagon-R cost about Rs1.1 million (when 6M Kibor was 6.23%). By Jan-20, price had increased by 55 percent for the car (6M kibor: 13.48%). On average, prices have increased over 44 percent across different passenger car variants (not including jeeps and SUVs) over this period.

So while the current year-on-year increment on monthly payment for a car does not seem like a lot; comparing today’s price from two years ago, car buyers are noticeably worse off. Taking Wagon-R’s example alone, quick calculations suggest, the extra amount a Wagon-R buyer would pay today versus what they paid in FY18 on an auto loan is ~ Rs11,000. That’s a substantial monthly burden. Have middle-class incomes grown by that much?

Comments

Comments are closed for this article.