On the 6th of July 2018, as the US imposed 25 percent tariffs on $34 billion worth of Chinese imports, it signalled a drastic change in the great power rivalry between the two economic giants. Behind Trump’s China policy were Peter Navarro, the economic advisor to Trump and Steve Bannon, the then Chief Strategist to the President. The brunt of the US pushback relied heavily on the huge bilateral trade deficit with China, which the administration believed was a fair indicator of China’s unfair trade policies. However, beyond the bilateral trade deficit, China’s savings rate is a much broader indicator and in fact, the cause of the plethora of imbalances facing the economy.

China has one of the highest savings rates in the world. The high savings rate is at the heart of China’s internal and external imbalances. While a low savings rate can pose a financing constraint on domestic economic development, high savings can lead to financing of unproductive investments and large external imbalances. To turn this savings into demand, China has two options. 1) Lend it internally and it comes back in the form of investment, 2) Lend it overseas and it comes back in form of export demand.

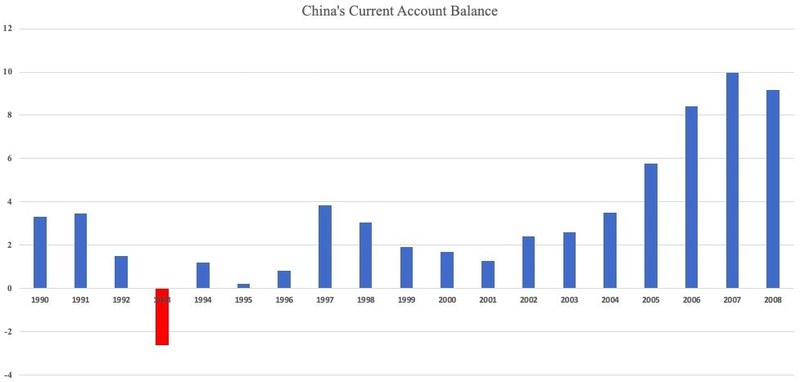

In late 1990s, the savings and investment rate moved in tandem but from 2001 onwards, the savings rate took a flight from an already high level, while the investment rate fell behind. The S-I gap grew wider. The current account mirrored these movements in Savings-Investment gap. The current account surplus too took a flight from 2001 onwards. 2001 was a turning point as China joined the World Trade Organisation and its economy started to open up to the global economy. With higher savings rate than investment, the Chinese economy was producing more than it could consume, thus as global markets opened up to Chinese products, China’s CA balance grew exponentially.

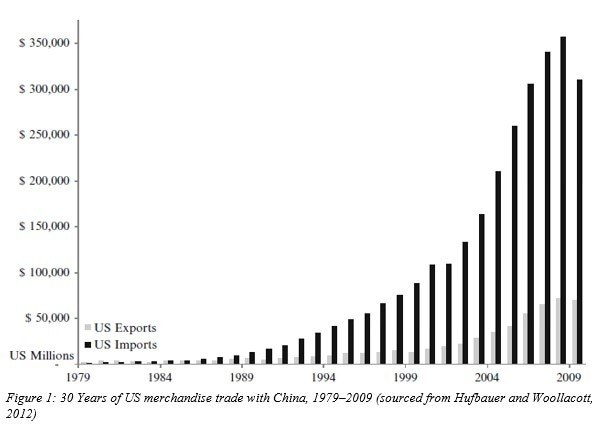

Back to the US-China bilateral trade, China was exporting more than it was importing, hence the CA surplus. More importantly, its bilateral surplus with the US skyrocketed. US imports from China far exceeded its exports to China. More money was flowing in China from the US as export payments than the other way. This presented a problem, who is going to pay for this gap? But China had a solution. Recall those two options I mentioned earlier. Well, China chose the second. It bought US treasuries through all this export money flowing from US into China.

China was basically fuelling America's appetite for Chinese goods. China's export-oriented growth model makes this relationship a necessity. If the Americans have no money to buy Chinese goods, then it spell trouble for China too. Hence, it is in China's interest to keep this relationship going.

This naturally leads to questions of American dependence on China and its vulnerability. “Surely, China can dump its dollar assets anytime to induce a run on the currency?". Well, theoretically yes, it can. But practically, it would mean disaster for China too. Chinese dollar holdings have continued to rise despite frequent threats to seek alternatives. China’s purchase of Treasury bonds has become a compulsion generated by its export-led model and its dumping of these bonds is unimaginable. Owing to the cost it would bear upon the Chinese economy, it is a cost China can ill afford.

Post Global Financial Crisis

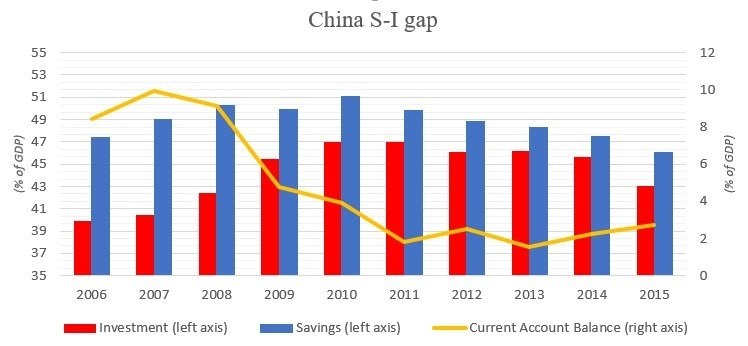

China's savings and investment gap was quite high prior to the crisis which was mirrored by its current account surplus. The CA surplus was increasing prior to the crisis, until it peaked in 2007 and then it started to decline. During the crisis, global trade took a big hit, far larger than aggregate output. China, whose growth model, relied heavily on exports, saw a sharp decline in its growth rate. Without context, China’s growth rate seemed perfectly fine however, for Chinese policymakers and their deadly obsession with GDP growth targets, it was a warning sign. As growth faltered, the Chinese begin to rethink their options.

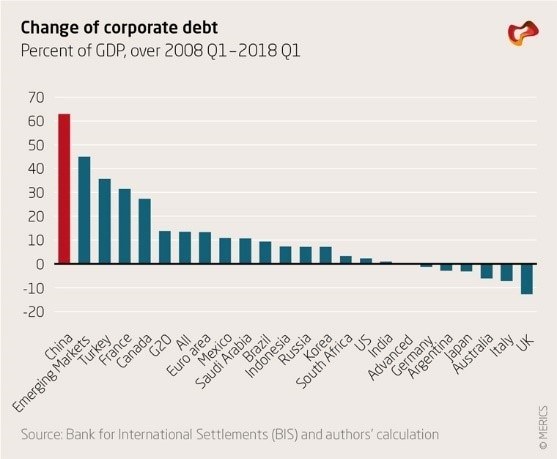

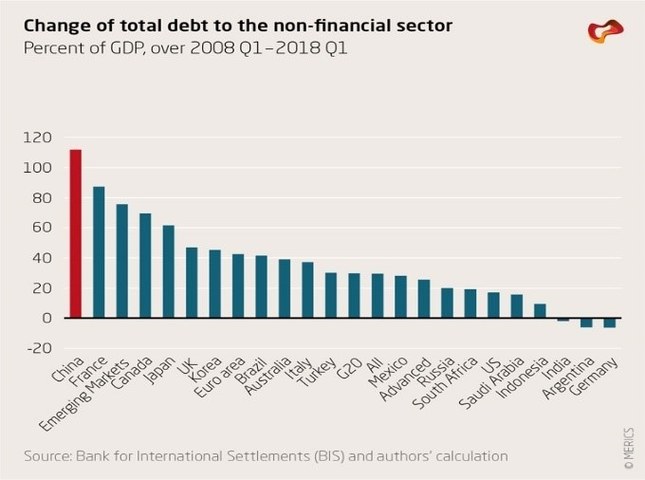

Recall again the two options they had to turn savings into demand. Well this time around, they choose option 1, lend savings internally. As a result, investment rate soared to catch up with the savings rate and the S-I gap narrowed, CA balance fell. To stimulate the economy, the Chinese enacted an expansive monetary and fiscal stimulus. This resulted in an unprecedented rise in debt, especially corporate debt. Even as the crisis faded these developments continued.

Chinese growth model shifted to a high intensity domestic investment led model, which was fuelled by their huge savings rate. But this high investment was not without its cost. It was fuelling unproductive investments in the economy to prop up GDP growth at cost of high debt build up. Because of the CCP's social contract with its people, the government encouraged state-led banks to lend to SOEs so they can finance their operations and keep people employed even when it makes little to no economic sense (i.e. steel dumping). A tale that started with high savings evolved into a multidimensional blend of imbalances that continue to date, while the CCP plays ‘whack a mole’ hammering a problem, only for another to appear elsewhere.

Saihan Mohammad is a student at LSE studying International Political Economy and Finance.

Comments

Comments are closed for this article.