Exide Pakistan in association with Chloride Group Plc of the UK was first incorporated in 1953 as a private limited company and went public in 1982. Chloride has associated across 35 countries in the world. Exide Pakistan is mainly in the business of manufacturing and sales of batteries, chemicals and acid with its manufacturing facilities for batteries located at SITE Karachi and Hub Balochistan while facilities for chemicals and acid located at SITE and Bin Qasim Karachi. In 2008, the company merged with Automotive Battery Company Limited.

Exide offers automotive, industrial and household solutions by providing a wide range of batteries-from cars, tractors, rickshaws, SUV's trucks, buses and marine transport to earth moving equipment and off-the-road vehicles. The company also manufactures special application industrial batteries for standby power, locomotive engine starting and train lighting systems. Meanwhile, the batteries also have household applications-by providing reliable backups in case of power cuts and voltage fluctuations.

Exide Pakistan serves its outlets in Pakistan through regional offices in Karachi, Sukkur, Multan, Faisalabad, Lahore, Rawalpindi, and Peshawar. These regional offices provide after sales service to customers and have a vast network of dealerships all over the country. The company's primary customers are major automotive companies and the sector drives the demand for Exide. The company's major competitors include Atlas Battery and Volta batteries.

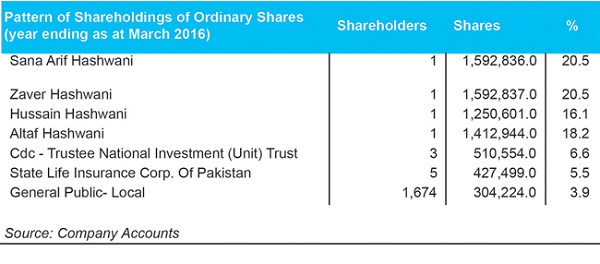

Owners, holdings and investments

Keeping it in the family, majority shares are held by the directors and family of the company-with 20.5 percent held by Sana and Zaver Hashwani each; 16 percent held by Hussain Hashwani and 18.2 percent held by Altaf Hashwani both of whom are part of the board of directors. Meanwhile, State life insurance corps holds 5.5 percent of the company's shares while National Investment (Unit) Trust holds 6.6 percent of the company's shares.

Exide Pakistan has a wholly owned subsidy Chloride Pakistan (Private) Limited which was first established in 1994 but the subsidiary never started manufacturing. The Company was incorporated to utilize the tax exemption offered by the government in Hattar. However, exemption was taken off after the company's incorporation and so the company did not commence its operations. The company was meant to manufacture and market automotive batteries and industrial cells.

In order to diversify its business activities, Exide set-up a sulphuric acid manufacturing plant at Port Qasim Industrial Area. The plant has an installed capacity of 50 metric tons of sulphuric acid per day.

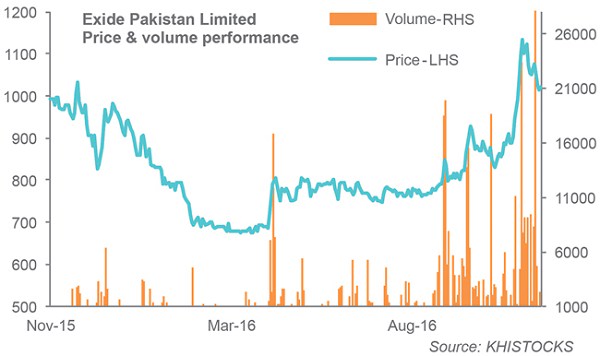

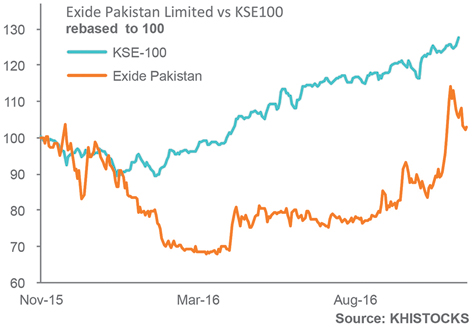

Despite a strong financial performance (read below), the company's stock price against the benchmark index has not followed an upward pattern and faced a significant down time between Jan to November of 2016, though nearing the start of 2017, volume traded is improving. Investors will keep a keen eye on this stock though as earnings go up with the company boosting a strong growth in this bottom line.

Financial and operational performance over the years

The main driver for the company is the automobile sector and Exide has been a leading player in the country with a strong footprint for many years. Growth in sales was phenomenal in 2010 and 2011 but sales grew slower in the later years. In 2011, production was affected as a result of major re-layout and shifting of machineries in order to streamline and improve production facilities. The company was concerned by expansion and installation of new facilities, training of manpower and harnessing the technology that faced initial problems.

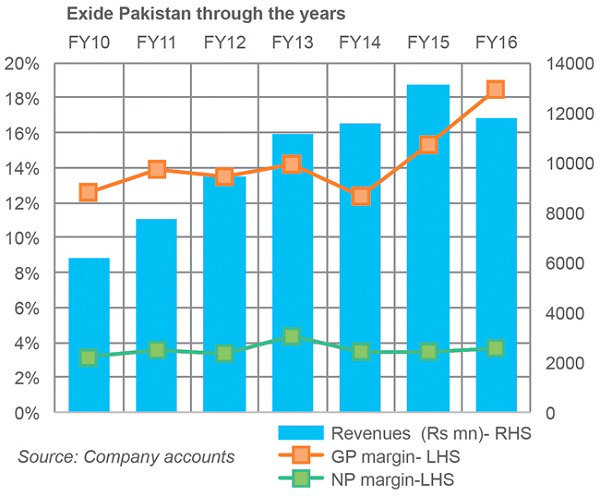

Between 2010 and 2016, total revenues went up from Rs 6 billion to nearly double at Rs 11.7 billion; though 2016 was a less than exciting year for the company having its revenues fall by 10 percent from Rs 13 billion in 2015.

The year prior to 2016 had its own challenges but the company worked more with less. It had to hire a new workforce and faced natural gas load shedding and low gas pressure that had to shift company's reliance on SNG based LPG which substantially increased the fuel expenses.

The company has two plants: battery and chemicals, with batteries capturing bulk of the company's business. According to the company's annual reports, it is difficult to ascertain the capacity of the battery plant because the capacity largely depends on the proportion of different types of batteries produced which varies in relation to the consumer demand, so the actual production for batteries followed market demand.

The installed capacity of the chemical plants is 33,000 tons actual production was 28,005 tons in 2016 , 26,674 tons in 2015, 26,932 tons in 2014 and 28,668 in 2013; going between 78 percent to 84 percent of capacity utilization.

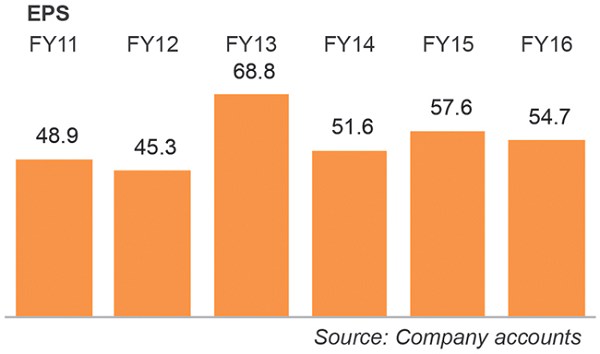

Profits soared until 2013; going from Rs 197 million in 2010 to Rs 485 million in 2013 but later dropped to Rs 424 million in 2016 year ending March. Profit margins however do not have any drastic fluctuations, inching up from 3.19 percent in 2010 to 3.6 percent in 2016. Gross margins on the other hand have had a better rally, having improved from 13 percent to 18 percent between these time periods, with cost of sales compressing over the years.

Snapshot of recent Half Yearly statements

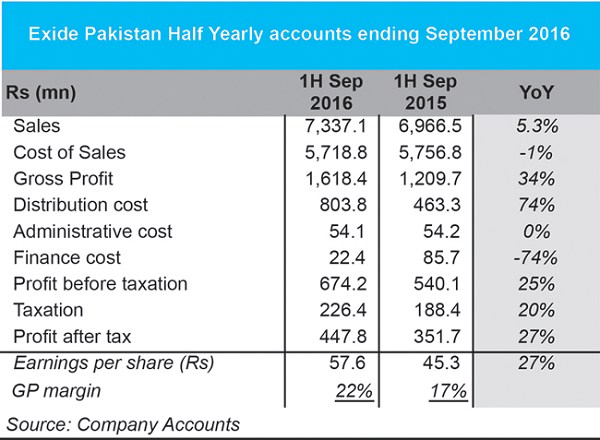

The company is kicking off its new fiscal with a promising boost in its bottom line despite less than expected sales revenues. The company reported a 5.3 percent growth in the top line, year on year for half yearly accounts ending September 2016, nudging sales up from Rs 6.9 billion to Rs 7.3 billion. Administrative costs have remained unchanged while distribution costs more than doubled during this time. Profit after tax for 1H of this year stood at Rs 447 million against Rs 351 million, while margins encouragingly increased from 17 percent to 22 percent which is a solid improvement.

Opportunities and threats

The future of the company does depend largely on how well the local automobile sector does in harnessing its demand forecasts. There are some good news. Many new players might be entering the market which will boost the car segment significantly. Meanwhile, the trucking sector in particular will see massive growth which is evident in new trucking investments and new entrants in the field that would boost the battery segment of Exide. Tractor sales have also been moving. The overall upward economic outlook bodes well for the company.

Potential threats remain cheaper energy prices, smuggling of batteries, the movement of raw material prices and the potential of new players entering the battery sector which is becoming an attractive market though bordering on oversupply. Atlas Battery is a prominent and close competitor that is also marketing its product vehemently to create a niche.

Exide must focus on improving technology and competitiveness. Despite having strong brand recognition across Pakistan, it must cater faster to new players that are entering in the car and trucking sectors.

Comments

Comments are closed for this article.