Pakistan stocks end FY26 on a high as KSE-100 jumps 44%

- Benchmark index records 335% gain in three fiscal years (FY24, FY25 and FY26)

The Pakistan Stock Exchange's KSE-100 Index surged 44% in FY2025-26, driven by improved macroeconomic stability under an IMF program and strong investor confidence.

- Macroeconomic stability and IMF program's influence.

- Significant IPO market growth and capital raised.

- Key economic indicators, including inflation and remittances.

- Future economic outlook and critical influencing factors.

Pakistan Stock Exchange’s (PSX) benchmark KSE-100 Index surged 44% in FY2025-26, capping the fiscal year on a strong note as improved macroeconomic stability under the IMF-supported programme boosted investor confidence and fueled a sustained stock market rally.

The KSE-100 closed the year’s last trading session at 180,301, up by 44% from 125,627 at the end of FY25.

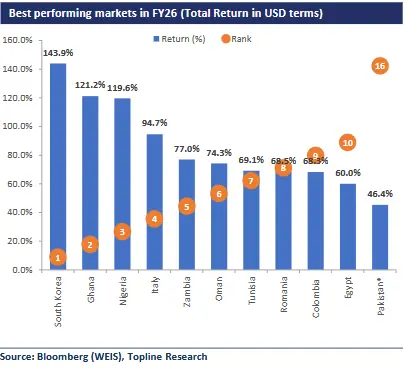

Over the three fiscal years (FY24, FY25 and FY26), the KSE-100 Index recorded a total gain of 335% in PKR terms (USD terms 347%).

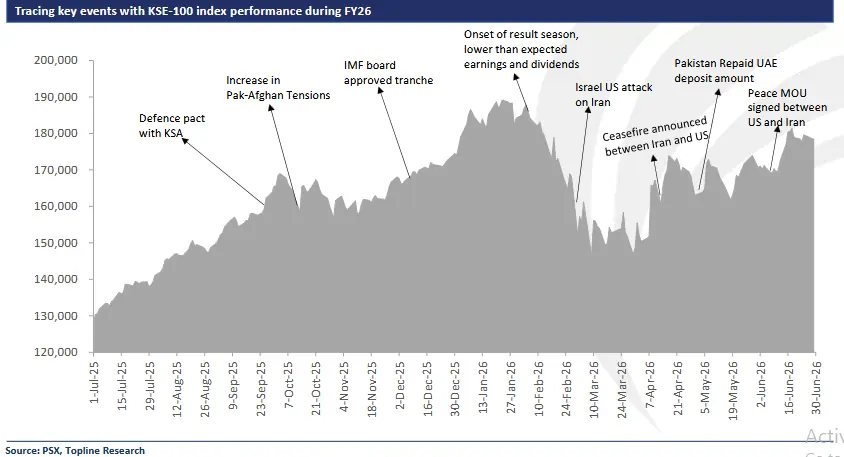

Despite escalating geopolitical tensions in the Middle East, the index posted strong gains in FY26, driven by improved macroeconomic stability.

Market performance during FY26 can be divided into two halves. During 1HFY26, the market posted a return of 39%, while in 2HFY26, it posted a return of 4%.

“The 1HFY26 performance was driven by improving economic indicators despite floods in July-August 2025. Meanwhile, 2HFY26 was quite eventful, with the index testing a low of 146,480 on March 9, 2026 and a high of 189,167 on January 23, 2026, representing a variance of 29%,” brokerage house Topline Securities said in a report.

“The significant volatility factor in 2H was due to Iran–US/Israel war which resulted in sharp surge in petroleum prices. Since Pakistan imports over 80% of its energy requirement, the concerns over slippage on external account increased.

“These concerns were further amplified when Pakistan decided to return UAE deposits of $3.5 billion in the month of Apr 2026. However, later, Pakistan managed to avert both the risk of higher oil prices and the repayment pressure by announcing proactive measures to manage petroleum demand and securing additional financial support from KSA.”

Pakistan also managed to raise $750 million in Eurobond and $250 million in Panda bond during month of Apr 2026 and May 2026, respectively.

“These measures helped market to return to pre-war level of over 168,000+ points index in mid of April 2026. Thereafter, on successful signing of MoU on Iran-US conflict and all time high monthly remittances of $4.3 billion in May 2026, the index reached +180,000 level.”

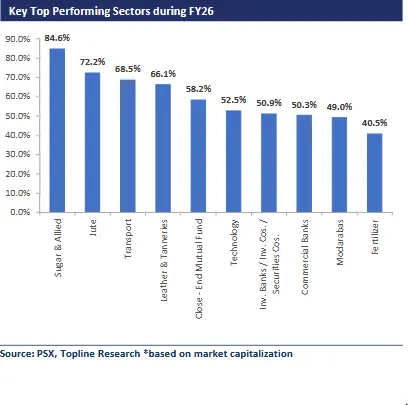

Sugar, Jute, Transport sectors outperformed the market during FY26, while Vanaspati, Synthetic rayon, and Woollen sectors lagged behind, the report said.

Bank of Punjab (BOP), Pakistan Telecommunication Company (PTC), and Askari Bank Limited (AKBL) were among top stocks in the KSE-100 during the year, while S.S.Oil Mills Limited (SSOM), TPL REIT Fund I (TPLRF1) and Ibrahim Fibres Limited (IBFL) were notable underperformers, according to the report.

Meanwhile, foreign corporates remained net sellers in the market with net selling of $895 million in FY26. Excluding Pioneer Cement Limited (PIOC) and Rafhan Maize Products Company Limited (RMPL) divestment, the selling by foreign corporates was $542 million, Topline said.

Among the local participants, mutual funds and companies were key buyers during the year while Banks, Insurance, and Brokers were top sellers.

IPOs in FY26

The initial public offering (IPO) market in FY26 continued to gain traction, as PSX recorded total of 13 IPO approvals, of which 11 had been listed and 2 were yet to be listed, according to an Arif Habib Limited report.

The total amount raised by currently listed IPOs amounts to Rs18.4 billion, the report said.

Also read: Tasdeeq set for PSX IPO, a first for South Asia’s credit information industry

Of the IPOs that were listed, the activity highlighted a diverse range of sectors, including Automobiles Parts and Accessories with SLM Tires Limited, raising Rs7.77 billion (the largest ever private sector IPO in Pakistan’s history), Food and Personal Care Products with Ghani Dairies Limited, contributing Rs3.43 billion, and Oil and Gas Marketing Companies with Sitara Petroleum Services Limited, adding Rs4.8 billion, it added.

“This shows increasing investor participation in Pakistan’s capital markets, along with improving regulations from SECP that has enabled companies from various sectors to raise equity capital with ease,” the report said.

Pakistan economy: key developments in FY26

Pakistan’s economy maintained macroeconomic stability in FY26, supported by prudent fiscal and monetary policies under the IMF programme. Inflation remained contained, the current account stayed broadly balanced, foreign exchange reserves improved, and the Pakistani rupee remained relatively stable despite external challenges, including geopolitical tensions in the Middle East.

The improved macroeconomic environment strengthened investor confidence and contributed to a broad-based recovery in economic activity and financial markets.

In March 2026, Pakistan authorities and International Monetary Fund (IMF) staff reached a staff-level agreement on the third review under Pakistan’s Extended Fund Facility (EFF) and the second review under the Resilience and Sustainability Facility (RSF), paving the way for inflow of $1.21 billion.

Inflation remained contained during the year, with May 2026 reading standing at 11.7%. During the first eleven months of the fiscal year, inflation stood at 6.69% against 4.61% recorded in the same period last year.

The government expects average inflation at 8.2% in FY27.

The inflow of overseas workers’ remittances into Pakistan stood at $4.251 billion in May 2026. In terms of growth, remittances increased by 20.2% on a month-on-month basis and 15.4% on a year-on-year basis.

Cumulatively, workers’ remittances increased by 9.2% to $38.1 billion during July-May FY26, compared to $34.9 billion received during the same period last year.

Foreign exchange reserves held by the State Bank of Pakistan (SBP) stood at $15.916 billion during the week ended June 19. The reserve would increase with a GoP inflow of $0.7 billion from multilateral institutions and about $1.7 billion as refinancing of GoP commercial loan, according to the central bank.

The central bank projected its foreign exchange reserves to reach approximately $18 billion by the end of FY26.

Pakistan rupee also maintained its marginal rally against the US dollar, gaining around 2% in FY26. Meanwhile, the real effective exchange rate (REER) – the value of rupee compared to basket of currencies of trading partner countries – hit over seven-and-a-half-year high at 106.15 points on the index in May 2026.

The SBP maintained the policy rate at 11% during most of 1HFY26 before cutting it by 50 bps in December 2025 amid contained inflation and improving economic activity. However, a resurgence in inflationary pressures driven by higher oil prices prompted a 100 bps hike in April 2026. The policy rate was subsequently kept unchanged in June 2026, ending FY26 at 11.5%.

The road ahead: Pakistan’s FY27 outlook

Looking ahead to FY27, Pakistan’s macroeconomic trajectory will largely depend on a combination of domestic policy execution and external developments.

According to Topline Securities, investors and policymakers should closely monitor several key indicators that are likely to shape the country’s economic performance over the coming year.

Among the most important factors are regional geopolitical developments and global commodity prices, particularly oil, as they directly influence inflation, the import bill, and the external account.

The level of foreign exchange reserves will also remain critical in determining Pakistan’s ability to meet external financing needs and maintain exchange rate stability.

The continuation of the IMF programme will be another major pillar supporting macroeconomic stability, as it is expected to facilitate external financing and reinforce investor confidence. In addition, any changes in Pakistan’s sovereign credit ratings will be closely watched, as upgrades or downgrades could affect the country’s borrowing costs, access to international capital markets, and overall investment sentiment.

Comments