Power generation: RLNG returns, coal remains

Pakistan's power sector found relief in May from hydel and LNG, but faces growing challenges from solar's "duck curve" effect, demanding greater grid flexibility and leading to elevated fuel costs.

- May's power generation trends and mix.

- Increased hydel and RLNG contributions.

- Solar boom's "duck curve" and grid flexibility challenges.

- Persistent reliance on imported coal and fuel costs.

May brought some much-needed relief to Pakistan’s power sector. After two months of severe RLNG shortages, widening generation deficits, and growing concerns over supply adequacy, the system finally caught a break.

Higher-than-expected hydel generation and the arrival of additional LNG cargoes helped narrow the gap between actual and reference generation. Yet for all the improvement, the month’s numbers also served as a reminder that the sector’s biggest challenge is no longer simply fuel availability. It is increasingly about flexibility.

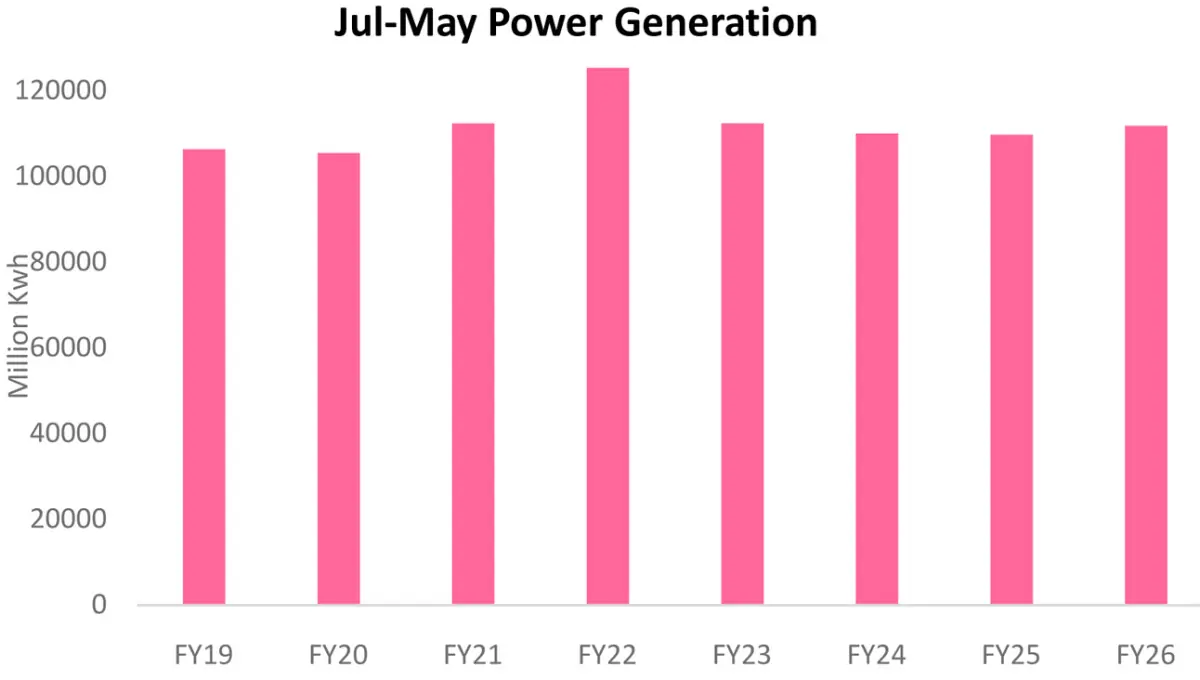

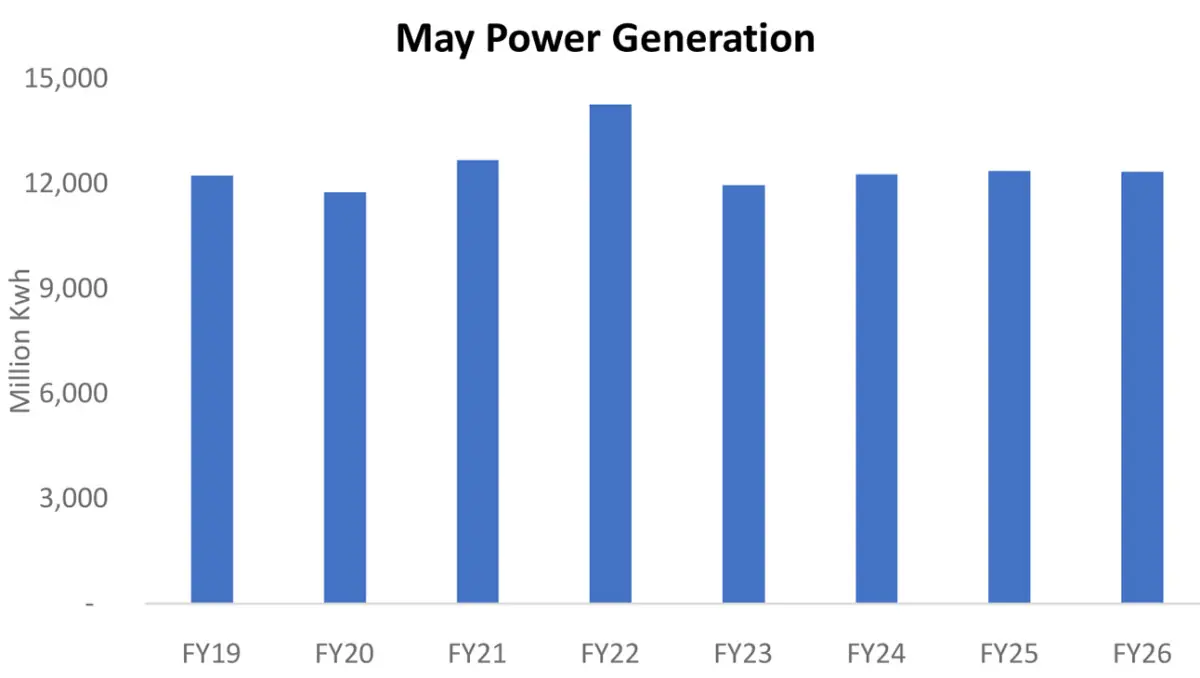

National grid generation stood at 12.3 billion kilowatt hours during May 2026, down 2.2 percent year-on-year. Cumulative generation during 11MFY26 reached 111.7 billion kilowatt hours, just 1 percent higher than last year.

More tellingly, generation remained roughly 8 percent below the peak levels recorded during FY22, underscoring how far demand still remains from its historic highs despite repeated tariff cuts and the return of industrial consumers to the grid.

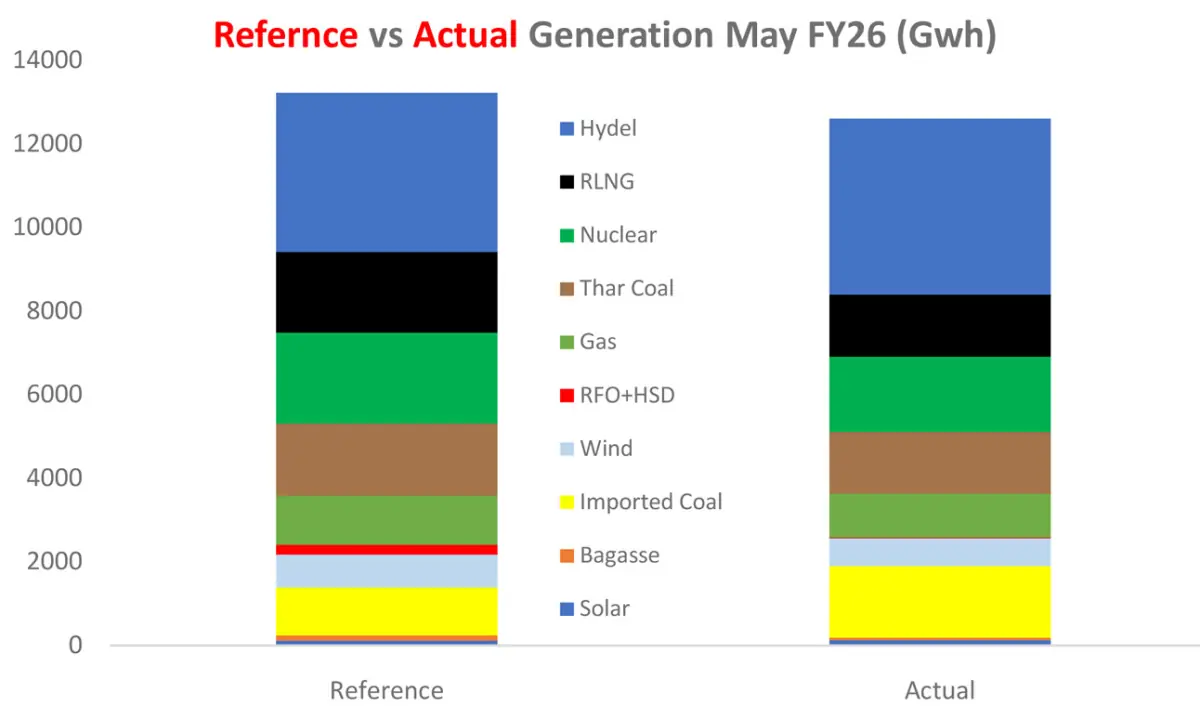

The generation deficit against reference levels narrowed materially from April. Actual generation came in roughly 5 percent below reference compared to an 11 percent shortfall a month earlier. The improvement owed largely to hydel generation, which once again emerged as the system’s savior.

Hydel’s share in the generation mix climbed to 33 percent and exceeded reference levels by roughly 10 percent.

In a system increasingly dependent on imported fuels and vulnerable to external shocks, hydel provided exactly the sort of low-cost relief policymakers would have hoped for. Without the stronger hydel contribution, the fuel cost picture would have looked considerably worse.

The second source of relief came from RLNG. After collapsing to its lowest level since the start of LNG imports a month earlier, RLNG-based generation staged a partial recovery as Pakistan managed to secure LNG cargoes despite ongoing disruptions in global energy markets. RLNG’s share improved to 12 percent of the generation mix. While still about 23 percent below reference levels, the recovery marks a notable turnaround from April’s near-disappearance of RLNG from the system.

The return of RLNG and stronger hydel output would ordinarily be enough to ease concerns over fuel costs. Yet the fuel mix tells a different story.

Imported coal remained the most significant deviation from planning assumptions.

Despite improved hydel availability and a partial RLNG recovery, imported coal generation remained nearly 48 percent above reference levels, accounting for roughly 14 percent of total generation. The persistence of imported coal’s elevated role suggests the challenge facing the grid is no longer merely one of energy availability. The issue increasingly revolves around when electricity is needed rather than how much is needed.

This is where Pakistan’s solar revolution enters the conversation.

The country’s rapidly expanding base of behind-the-meter and off-grid solar continues to suppress daytime grid demand. Midday generation levels remain markedly lower than those seen two or three years ago despite overall electricity consumption moving in the opposite direction. The result is a deepening duck curve that is fundamentally altering system operations.

As the sun sets, demand on the grid returns abruptly. The system must ramp up generation at a pace that would have seemed extraordinary just a few years ago. That responsibility traditionally falls on flexible generation sources, particularly RLNG-based plants. But even with the recent recovery, RLNG availability remains well below planning assumptions.

The consequence is that other sources are increasingly being called upon to perform tasks they were never designed to handle efficiently. Imported coal plants are running harder and longer. More expensive generation is being dispatched. Fuel costs remain elevated. And the monthly fuel cost adjustment remains positive for the fifth consecutive month, with nearly Rs1 per unit sought for May.

The operational stress is becoming increasingly visible. The shape of Pakistan’s daily load profile now bears little resemblance to that of the pre-solar era. Demand is increasingly concentrated in evening hours, creating steep ramping requirements that test both generation flexibility and transmission capability.

This challenge extends beyond fuel availability. Transmission constraints continue to limit the movement of electricity from generation-rich regions to demand centers. Years of investment have undoubtedly improved the system, but periodic stress episodes continue to expose lingering bottlenecks. The issue becomes particularly evident during evening peaks, when even modest increases in demand can stretch the system.

The irony is difficult to miss. Pakistan’s solar boom has arguably shielded the country from a far greater energy crisis. Without it, the disruption to LNG supplies and broader geopolitical uncertainty could have translated into significantly higher fuel imports and greater pressure on foreign exchange reserves. Yet the same solar boom is also creating a new set of operational challenges that the grid was never designed to accommodate.

May demonstrated that the sector can still find temporary relief when hydel conditions improve and LNG cargoes arrive on time. But it also showed that the underlying challenge remains firmly in place. The duck curve is getting deeper. Evening ramps are getting steeper. Imported coal continues to play a larger role than planners anticipated. And despite a more favorable fuel mix than April, consumers are still looking at another positive fuel adjustment.

The crisis may have eased. The balancing act has not.

Comments