Mandviwala Mauser Plastic Industries (PSX: MWMP) was incorporated in Pakistan as a public limited company in 1988. The principal activity of the company is the manufacturing and sale of plastic and allied products.

Pattern of Shareholding

As of June 30, 2025, MWMP has a total of 28.748 million shares outstanding which are held by 2584 shareholders. Public sector companies and corporations have the majority stake of 74.41 percent in the company followed by local general public holding 18.84 percent shares.

Directors, CEO, their spouse and minor children account for 4.61 percent shares of MWMP while foreign general hold 1.5 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2021-25)

MWMP recorded no revenue in 2020. In the following years, it revenue posted growth. The company registered net loss in 2020 and 2021 followed by net profit in the subsequent years.

The company’s bottomline and margins attained their optimum level in 2024 followed by a downtick recorded in 2025. The detailed performance review of the period under consideration is given below.

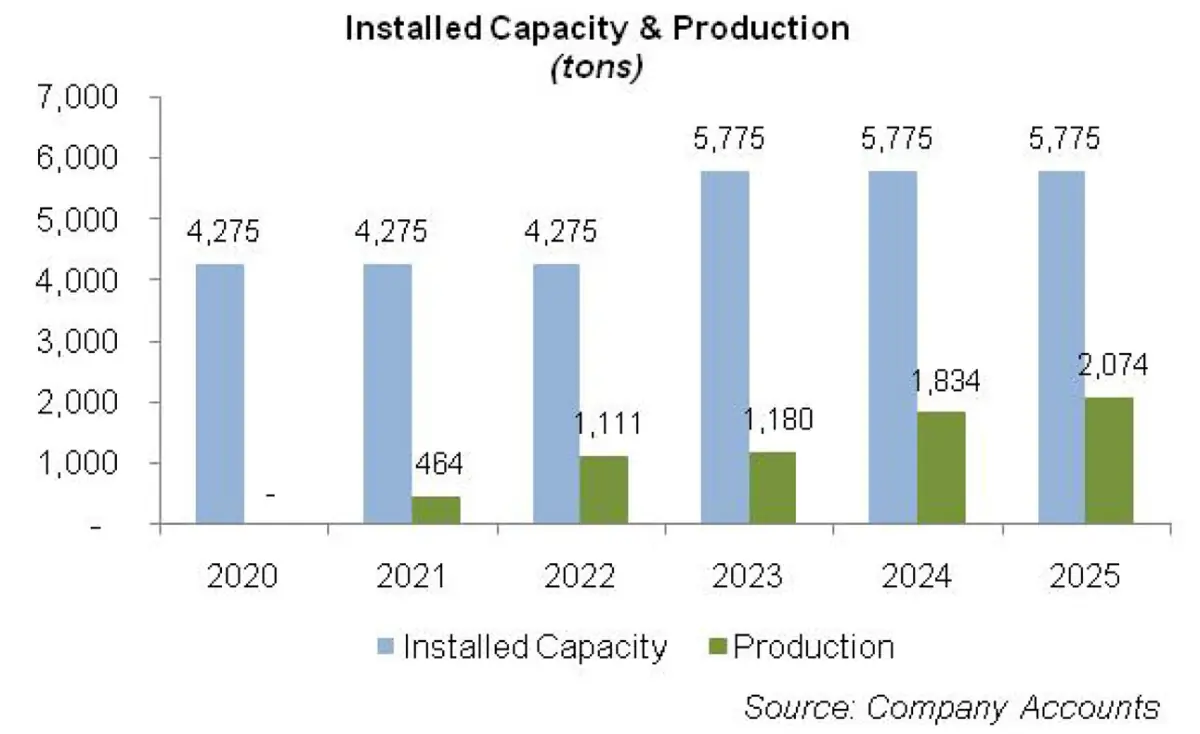

In 2021, MWMP recorded net sales of Rs.123.106 million compared to no sales recorded in the previous year. Production volume clocked in at 464 tons which translated into capacity utilization of 10.85 percent in 2021. This was against no production undertaken in the previous year.

The company had discontinued its commercial production with effect from July 01, 2013 due to uncertain conditions, geographical isolation and excessive power disruption in Uthal, Baluchistan, where the company’s plant was located.

During the period ranging from 2013 to 2020, the company shifted its plant and machinery to Karachi and resumed commercial production with effect from July 25, 2020.

Cost of sales surged by 360.26 percent in 2021 mainly on the back of raw materials consumed and utility expense incurred during the year. This resulted in gross profit of Rs.0.027 million in 2021 versus gross loss of Rs.26.74 recorded in the previous year.

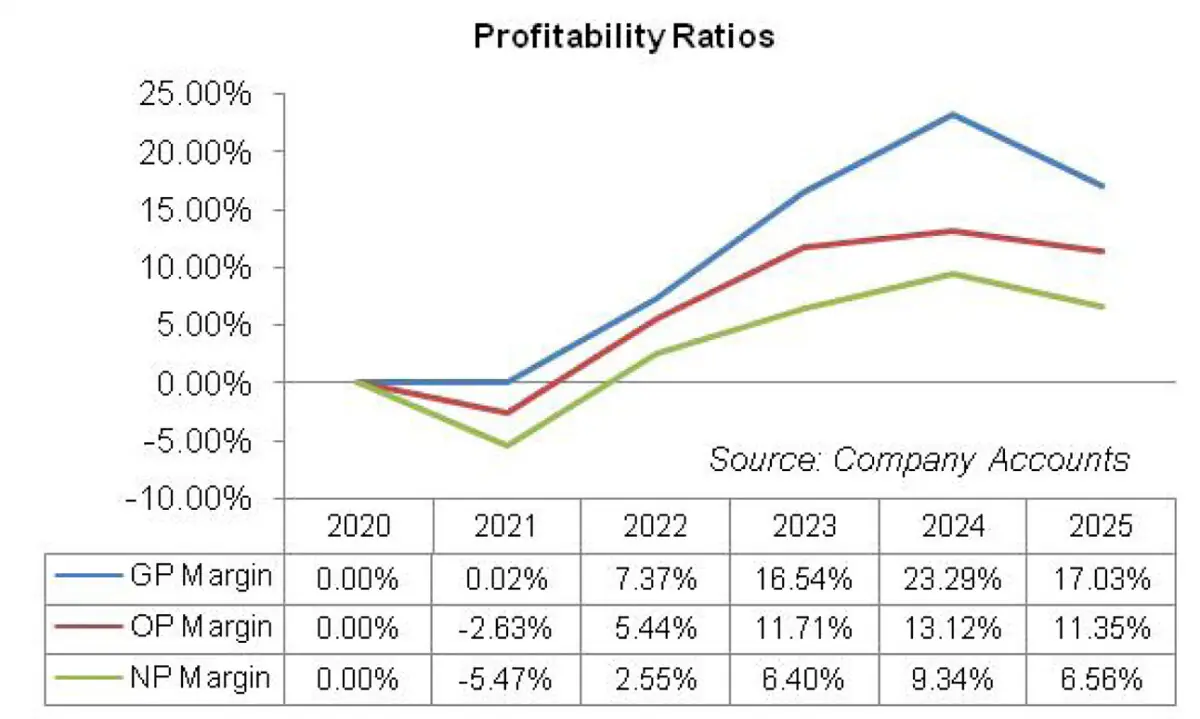

GP margin was recorded at 0.02 percent in 2021. Administrative expense ticked up by 12.71 percent in 2021 mainly on the back of payroll expense as well as fee & subscription charges incurred during the year. Selling & distribution expense surged by 1679.14 percent in 2021 due to freight charges which were not being incurred until the previous year.

MWMP posted net other income of Rs.9.588 million in 2021 versus net other expense of Rs.0.191 recorded in 2020. This was due to the fact that in the previous year, the company recorded loss on assets destroyed in transit versus recovery of insurance claim in 2021. The company registered operating loss of Rs.3.243 million in 2021, down 91 percent year-on-year.

Finance cost spiked from Rs.0.007 million in 2020 to Rs.1.597 million in 2021. In the previous year, the company’s finance cost comprised of only bank charges while in 2021, it obtained short-term loan from a bank, hence incurred interest expense along with higher bank charges.

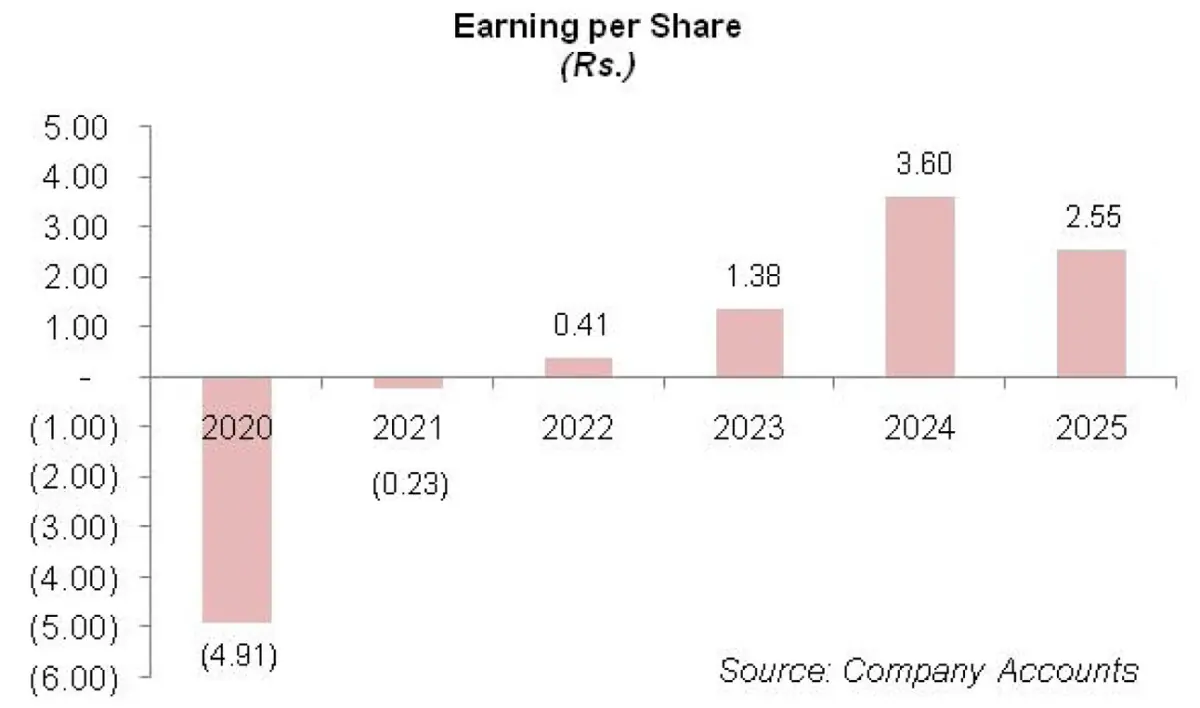

The company posted net loss of Rs.6.735 million in 2021, down 81.34 percent year-on-year. This translated into loss per share of Rs.0.23 in 2021 versus loss per share of Rs.4.91 recorded in 2020.

MWMP’s topline rebounded by 272.22 percent to clock in at Rs.458.22 million in 2022.

Production volume surged by 139.44 percent to clock in at 1111 tons in 2022. This translated into capacity utilization of 26 percent in 2022. Demand was highly concentrated in chemical, lube oil and food sectors. This was the second year of the company’s operation after its restructuring.

MWMP was in the process of constantly expanding its product range to attain greater market competitiveness. Cost of sales mounted by 244.85 percent in 2022 mainly on the back of increased production, higher raw material expense and utility expense incurred during the year.

MWMP recorded gross profit of Rs.33.78 million. Lesser payroll expense as well as a downtick recorded in fee & subscription charges resulted in 9.76 percent drop in administrative expense in 2022.

Conversely, selling & distribution expense escalated by 249.58 percent in 2022 due to mounting freight charges. Net other income ticked up by 2.46 percent in 2022 as the company received waiver of rent expense from M/S MM Flour Mills (Private) Limited for the period ranging from January 2020 to November 2021.

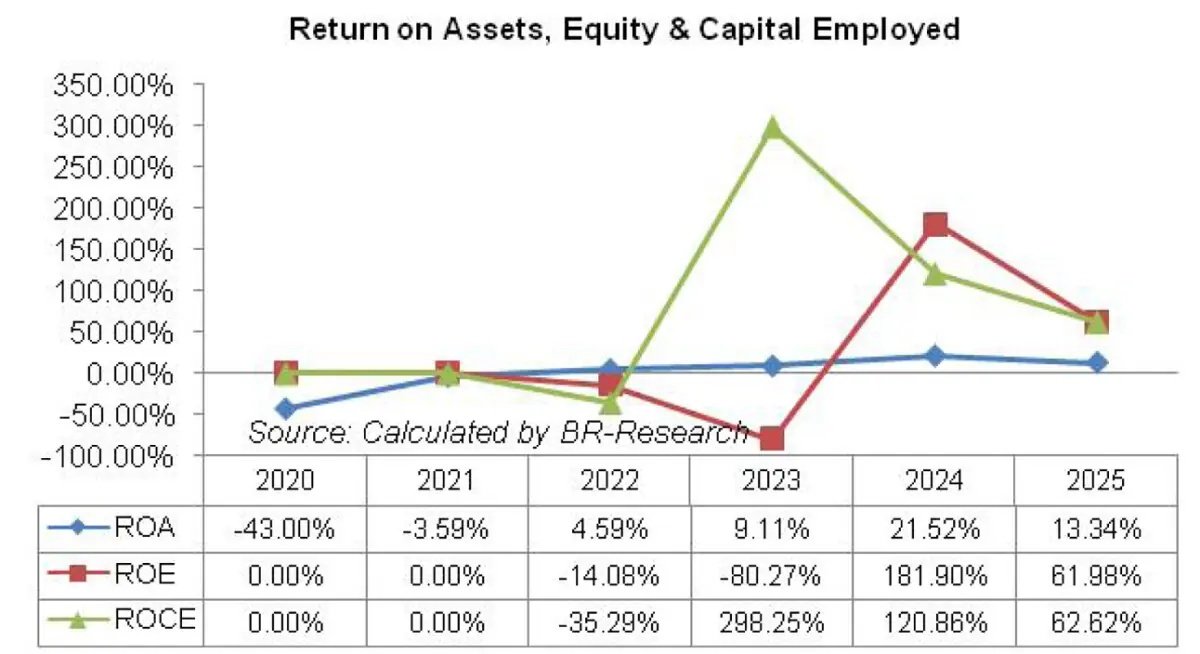

The company recorded operating profit of Rs.24.935 million in 2022 with OP margin of 5.44 percent. Finance cost soared by 369.15 percent in 2022 due to higher discount rate and increased outstanding liabilities. MWMP registered net profit of Rs.11.66 million in 2022. This translated into EPS of Rs.0.410 and NP margin of 2.55 percent in 2022.

In 2023, MWMP registered 35.26 percent improvement in its topline which clocked in at Rs.619.811 million.

The company increased its capacity from 4275 tons in 2022 to 5775 tons in 2023. Production volume was recorded at 1180 tons, up 6.21 percent year-on-year. While the company expanded into 250 liters drums in blow molding packaging, it didn’t launch the product during the year due to persistently difficult macroeconomic conditions. Demand was mainly driven by food and chemical sectors in 2023.

Cost of sales surged by 21.88 percent in 2023 due to higher raw material charges, utility expense, rent expense as well as travelling expense incurred during the year. Gross profit improved by 203.52 percent in 2023 which translated into a stronger GP margin of 16.54 percent.

Administrative expense climbed up by 63 percent in 2023 mainly on the back of higher payroll expense. Distribution expense escalated by 19.75 percent in 2023 due to a spike in freight charges as well as advertisement charges incurred during the year.

Net other expense of Rs.3.634 million recorded in 2023 was due to higher provisioning done for WWF and WPPF and no waiver of rent expense received unlike the previous year. Operating profit strengthened by 191 percent in 2023 with OP margin jumping up to 11.71 percent.

Finance cost multiplied by 227.98 percent in 2023 due to higher discount rate and increased short-term borrowings. Net profit picked up by 240 percent to clock in at Rs.39.66 million in 2023. This translated into EPS of Rs.1.38 and NP margin of 6.40 percent in 2023.

MWMP’s topline further enlarged by 78.85 percent to clock in at Rs.1108.56 million in 2024. Production volume surged by 55.42 percent to clock in at 1834 tons in 2024. This translated into capacity utilization of 31.76 percent in 2024. The company’s new product – 250 liters drums which it withheld in the previous year – was launched in 2024 and received great market response.

Cost of sales hiked by 64.39 percent in 2024 due to increased production, higher inflation and utility expense.

Gross profit strengthened by 151.84 percent in 2024 with GP margin attaining its optimum level of 23.29 percent. Administrative expense surged by 89 percent in 2024 mainly due to higher payroll expense, fee & subscription charges as well as office expense.

MWMP expanded its workforce from 46 employees in 2023 to 57 employees in 2024. Higher freight charges and commission charges pushed up distribution expense by 28.14 percent in 2024.

Net other expense escalated by 1823.96 percent in 2024 primarily due to provisioning done for ECL and slow moving stores & spares besides booking impairment of assets in bond. Operating profit strengthened by 100.44 percent in 2024 with OP margin ticking up to 13.12 percent.

Finance cost grew by 21.57 percent in 2024 due to higher discount rate. Net profit rebounded by 160.94 percent to clock in at Rs.103.488 million in 2024. This translated into EPS of Rs.3.60 and NP margin of 9.34 percent in 2024.

In 2025, MWMP’s net sales didn’t demonstrate any significant improvement, registering only 0.67 percent growth to clock in at Rs.1116.036 million. This year, the company prioritized volume over pricing to enhance its market penetration. This was the reason why sales volume growth of 17 percent couldn’t produce any significant difference on the topline. Production volume grew by 13 percent to clock in at 2074 tons in 2025.

Capacity utilization was recorded at 35.91 percent in 2025. Cost of sales surged by 8.89 percent in 2025 which pushed down GP margin to 17 percent. Gross profit also shrank by 26.40 percent in 2025. 44.64 percent spike in administrative expense in 2025 was the result of higher payroll expense, travelling & conveyance charges, legal & professional charges as well as fee & subscription charges incurred during the year. Number of employees was increased to 69 in 2025.

Higher freight charges pushed up distribution expense by 12 percent in 2025. Net other expense fell by 91.11 percent in 2025 due to high-base effect as MWMP recorded provision for slow moving stores and spares, impairment of assets in bond and write off of raw materials in bond in the previous year.

The company recorded reversal of provision booked on ECL in 2025 versus provisioning done in the previous year. This also squeezed net other expense in 2025.

Operating profit ticked down by 12.93 percent in 2025 with OP margin falling down to 11.35 percent. Finance cost inched down by 10.74 percent in 2025. Majority of the company’s outstanding loan fell in the category of interest free loan obtained from Meskay & Femtee Trading Company (Private) Limited.

Net profit plunged by 29.26 percent to clock in at Rs.73.205 million in 2025. This culminated into EPS of Rs.2.55 and NP margin of 6.56 percent in 2025.

Recent Performance (1QFY26)

MWMP posted 91.48 percent stronger topline to the tune of Rs.451.72 million in 1QFY26. The main growth driver was higher demand from chemical sector due to its growing export potential.

Macroeconomic recovery also ensured steady demand from other sectors in 1QFY26. Gross profit picked up by 111.55 percent in 1QFY26 due to stable raw material prices, stronger Pak Rupee and robust demand. GP margin clocked in at 20 percent in 1QFY26 versus GP margin of 18.15 percent recorded in 1QFY25.

CAPEX worth Rs.6.98 million undertaken in 2025 to enhance operations coupled with increased capacity utilization was the reason for 88.56 percent higher administrative expense recorded in 1QFY26.

Higher sales volume also drove up distribution expense by 43.83 percent in 1QFY26. Operating profit improved by 133.82 percent in 1QFY26 with OP margin clocking in at 16 percent versus OP margin of 13.10 percent recorded in 1QFY25.

Finance cost tumbled by 11.40 percent in 1QFY26 due to monetary easing and lesser outstanding borrowings. MWMP recorded net profit of Rs.48.124 million in 1QFY26, up 154.68 percent year-on-year. EPS clocked in at Rs.1.67 in 1QFY26 versus EPS of Rs.0.66 recorded in 1QFY25. NP margin progressed from 8 percent in 1QFY25 to 10.65 percent in 1QFY26.

Future Outlook

In the remaining part of the ongoing fiscal year, the company will materialize its approved capital expenditure of Rs.250 million to enhance its production capacity, modernize its machinery and enhance product quality. This will not only enable the company to take optimum advantage of rising demand but will also allow it to reduce its cost, resulting in stronger bottomline and margins.

Positive bottomline over the years has enabled MWMP to squeeze its accumulated losses, which is a step towards improved financial sustainability and shareholder value. Aggressive market penetration carried out in the past will also bear fruit in the coming times.

Comments