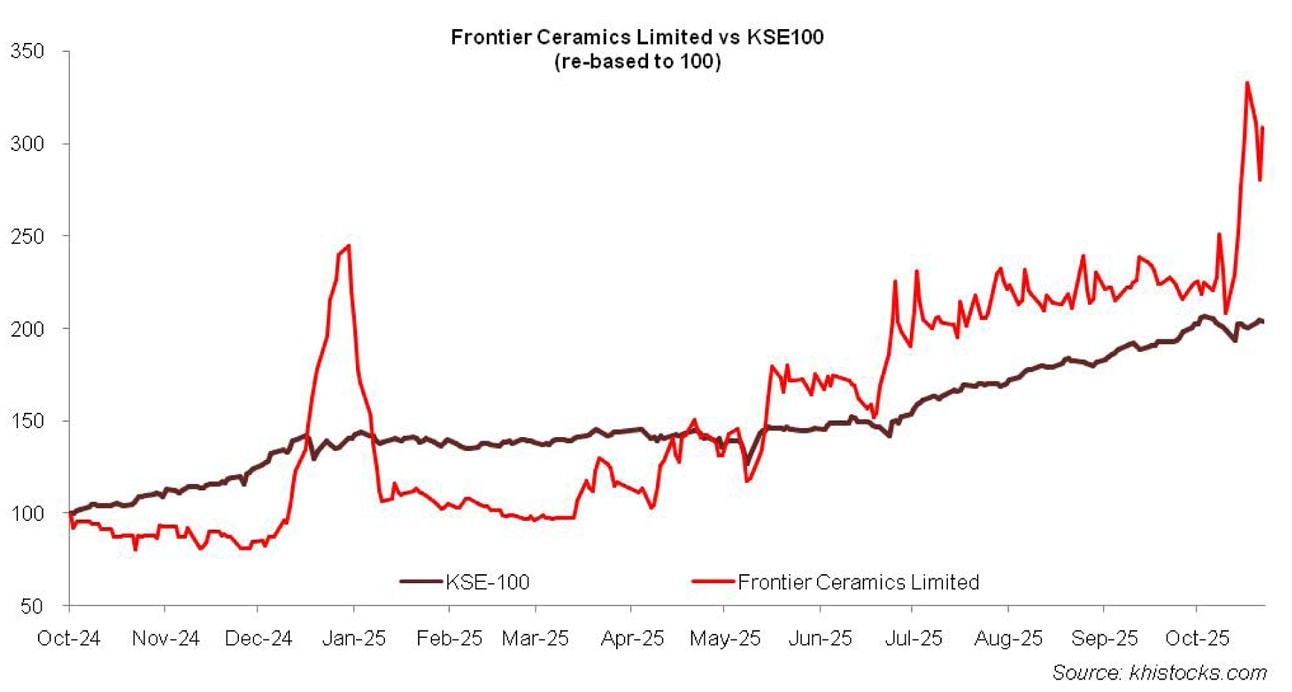

Frontier Ceramics Limited (PSX: FRCL) was incorporated in Pakistan as a public limited company in 1982. The company is engaged in the manufacturing and sale of wall and floor ceramic tiles, sanitary wares and other related products.

Pattern of ShareholdingAs of June 30, 2025, FRCL has 37.874 million shares outstanding which are held by 980 shareholders. Directors, their spouse and minor children have the majority stake of around 96 percent in FRCL followed by local general public holding 3.15 percent shares of the company. The remaining shares are held by other categories of shareholders.

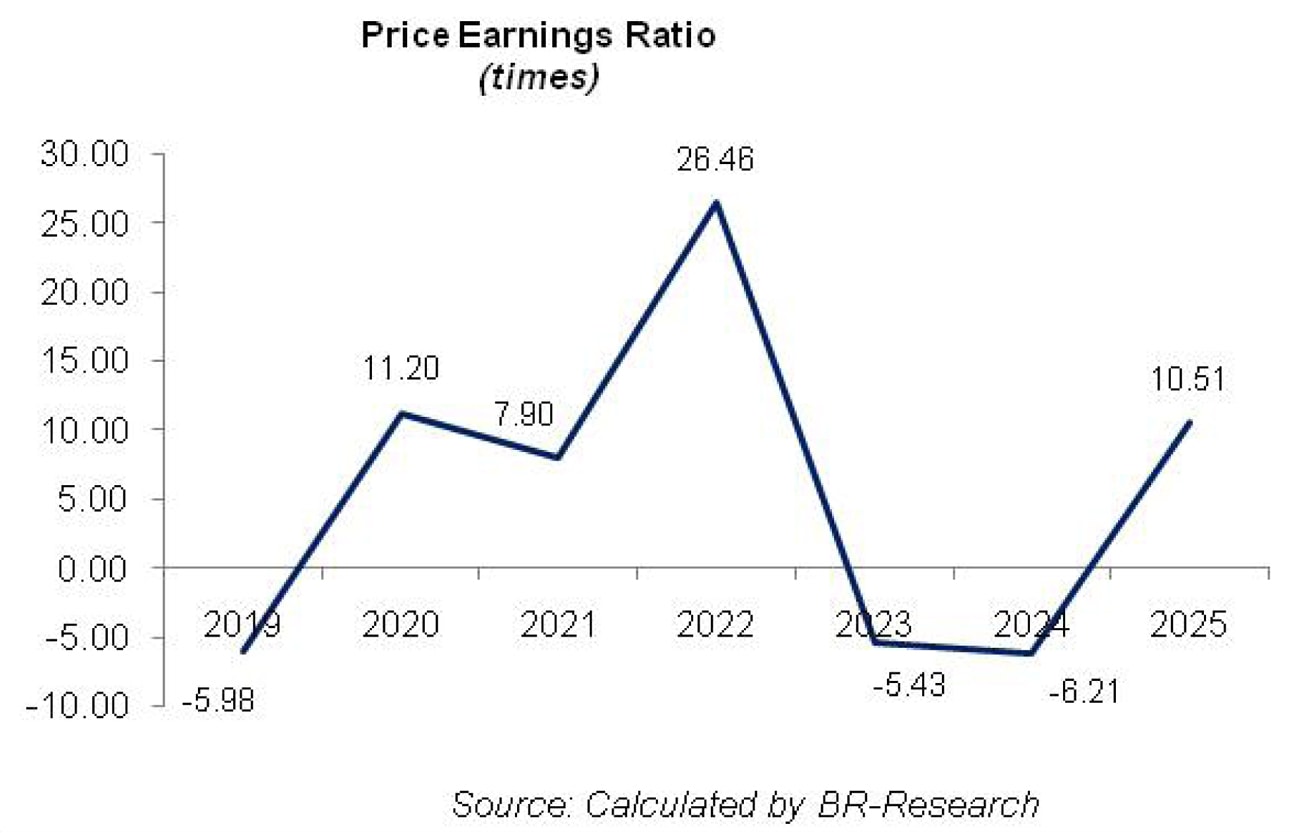

Historical Performance (2019-25)

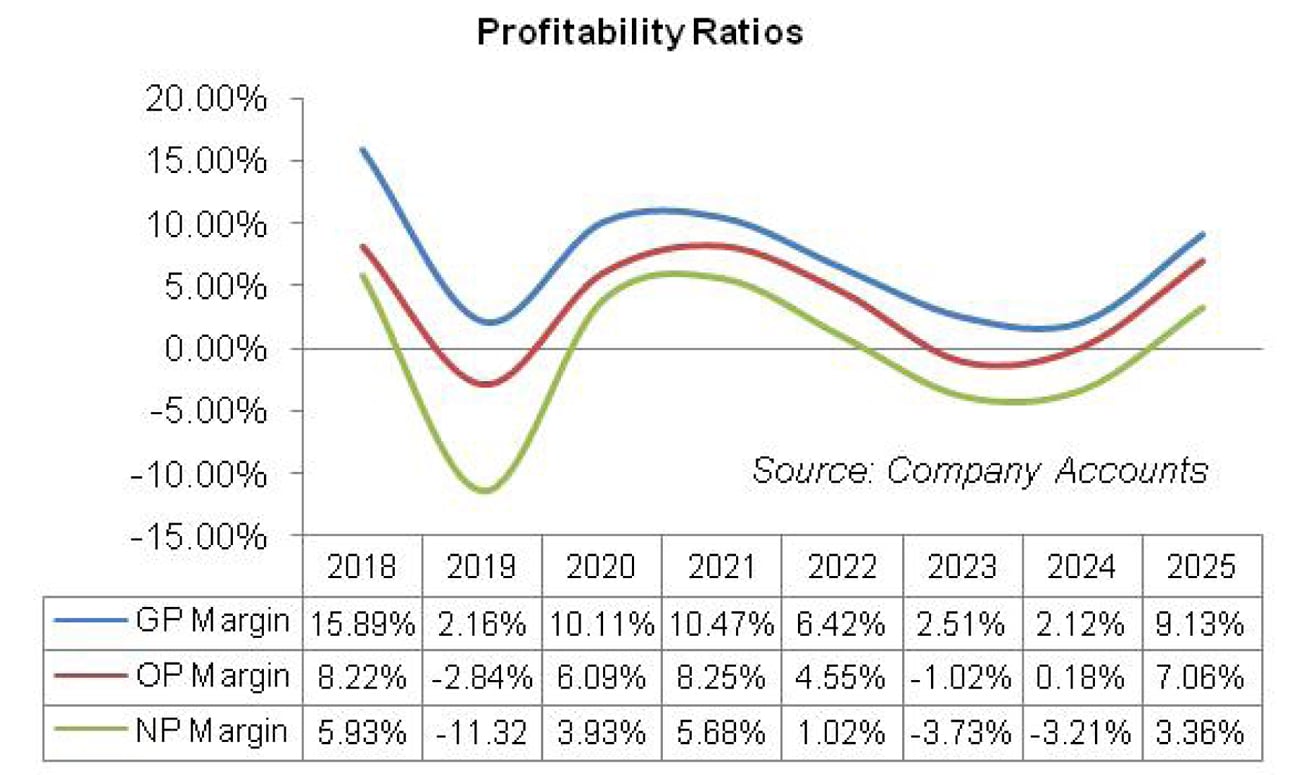

FRCL’s topline strengthened over the period under consideration except for a year-on-year dip recorded in 2024. Conversely, its bottomline posted net loss in 2019, 2023 and 2024. FRCL’s margins drastically fell in 2019 and then improved for the next two years. This was followed by a plunge in 2022 and 2023.

In 2024, GP margin continued to slide while OP and NP margin registered slight improvement. FRCL’s margins posted significant rebound in 2025 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, year-on-year topline growth of 17.57 percent was posted by FRCL. This pushed its topline up to Rs.781.83 million. The growth was led by higher volumes. However, cost of sales grew by 36.75 percent year-on-year in 2019 on the back of heavy consumption of LPG to cater to the issue of gas load shedding. Increase in gas tariff and Pak Rupee depreciation also played their due role in pushing up cost of sales and squeeze the gross profit by 84 percent year-on-year in 2019.

GP margin radically plummeted to 2.16 percent in 2019 versus GP margin of 15.89 percent recorded in 2020. To top it off, operating expense also grew on account of higher payroll expense and depreciation.

FRCL enhanced its workforce from 203 employees in 2018 to 242 employees in 2019. This resulted in FRCL recording operating loss of Rs. 22.18 million in 2019 as against operating profit of Rs.54.65 million posted in 2018. Other expense dropped by 92 percent in 2019 as FRCL didn’t make any provisioning for WWF and WPPF during the year.

Moreover, there were no inventory write offs during the year as against the previous year. Other income didn’t provide any respite either and plunged by 90.40 percent year-on-year in 2019 due to high-base effect as the company wrote back liabilities of Rs.19.47 million in 2018.

Finance cost gave another major blow to the bottomline by expanding by over 240 percent year-on-year in 2019. Not only the higher discount rate did the trick, the company’s short-term and long-term borrowings also grew during the year,. FRCL posted net loss of Rs. 88.47 million in 2019 as against net profit of Rs.39.43 million recorded in 2018. Loss per share clocked in at Rs.2.34 in 2019 versus EPS of Rs.1.04 registered in 2018.

The next two years were characterized by staggering topline and bottomline growth and improved margins. Sales growth was led by both improved volumes and upward revision in the sales prices. In 2020, before the outbreak of COVID-19, the company performed exceptionally well and recorded net sales growth of 42.64 percent for the year despite sluggish business in the 2HFY20. 2021 saw an uproar in construction activity post COVID-19 and resulted in the highest topline growth of 153.67 percent.

Cost of sales was kept in check in both the years which resulted in phenomenal growth of gross profit to the tune of 566.40 percent and 162.81 percent respectively in 2020 and 2021. This led FRCL record GP margin of 10.11 percent and 10.47 percent in 2020 and 2021 respectively. Operating expenses were higher in both the years on the back of improved sales volume coupled with inflationary pressure.

FRCL expanded its workforce to 546 employees in 2020 and 764 in 2021. This led to higher payroll expense. Higher freight charges and depreciation also led to elevated operating expense in both the years. Other expense also posted hefty growth of 116.83 percent and 336.59 percent respectively in 2020 and 2021 owing to higher provisioning for WWF and WPPF coupled with higher legal & professional charges.

FRCL recorded operating profit of Rs.67.89 million in 2020 as against operating loss of Rs.22.18 million in 2019. This translated into OP margin of 6.10 percent in 2020. Operating profit further strengthened by 243.81 percent in 2021 with OP margin registering its optimum level of 8.25 percent. Other income built up by 43.24 percent and 33.06 percent respectively in 2020 and 2021. Finance cost also buttressed the bottomline in both the years.

In 2020, when discount rate was high for most part of the year, the company considerably squeezed its long-term borrowings resulting in 13.60 percent lower finance cost. In 2021, finance cost further shrank by 12.40 percent due to monetary easing. In 2020,

FRCL posted net profit of Rs.43.85 million with EPS of Rs. 1.16. In 2021, net profit mounted by 266.50 percent to clock in at Rs. 160.71 million with EPS of Rs.4.24. FRCL posted NP margin of 3.93 percent and 5.68 percent respectively in 2020 and 2021.

The merry time enjoyed by FRCL for the two consecutive years seems to end in 2022 as the company once again faced a drastic bottomline fall and constricted margins despite topline growth of 32.85 percent. Net sales clocked in at Rs.3758.16 million in 2022. During the year, both public and private construction activities were arrested owing to low purchasing power of consumers and a meteoric rise in the prices of construction materials.

FRCL altered its sales portfolio to focus more on the high margin products which resulted in growth of net sales. Cost of sales continued to surge as the company shifted its plant operations on RLNG which is much more expensive than the natural gas. This coupled with Pak Rupee depreciation and elevated prices of other basic raw materials took a toll on FRCL’s gross profit which eroded by 18.52 percent in 2022.

GP margin also dipped to 6.42 percent in 2022. Operating expense succumbed to inflationary pressure. During the year, the company hired 22 additional workers to take the tally to 786 employees. The company made lower provisioning for WWF and WPPF during the year, resulting in 29.47 percent lower other expense. Operating profit slumped by 26.68 percent in 2022 with OP margin slipping to 4.55 percent as against OP margin of 8.25 percent recorded in the previous year.

Finance cost grew by 20.79 percent in 2022 on the back of higher discount rate and also because the company secured fresh long-term financing of Rs.73.26 million during the year for the purchase of generator. Net profit dwindled by 76 percent year-on-year in 2022 to clock in at Rs.38.51 million with EPS of Rs.1.02 and NP margin of 1 percent.

The bottomline slide and margins contraction which began in 2022 persisted in the 2023 as economic and political malfunctioning continued. The topline grew by 9.51 percent year-on-year in 2023 to clock in at Rs.4114.50 million. This was the result of alterations in product portfolio and sales channel mix. These changes enabled FRCL to sustain its volumes at last year’s level.

Cost of sales spiked by 14 percent in 2023 due to global commodity super cycle owing to Russia-Ukraine crisis. This was further exacerbated by Pak Rupee depreciation, high indigenous inflation, hike in energy tariff, jagged supply of gas as well as import restrictions which led to supply chain impediments. This marred gross profit which plunged by 57.18 percent year-on-year in 2023 with GP margin sliding to 2.51 percent.

Distribution and administrative expenses escalated by 33.58 percent and 29.13 percent respectively in 2022 on account of higher payroll expense, depreciation expense as well as provision booked for ECL. Number of employees increased to 813 employees in 2023. Other expense gave a major hit to the bottomline as it grew by 459.58 percent in 2023 to reach Rs. 70.35 million. This was on account of hefty exchange loss incurred during the year.

FRCL made operating loss of Rs.41.99 million in 2023. Other income magnified by 344 percent in 2023 on account of higher markup income. Finance cost continued to enlarge on the back of high discount rate. This resulted in net loss of Rs.153.47 million in 2023 with loss per share of Rs.4.05.

In 2024, FRCL’s topline posted year-on-year decline of 16.91 percent to clock in at Rs.3419.35 million. This was due to slowdown in construction activities which led to demand destruction in the tiles & ceramics industry. On the supply front, limitations on the opening of Letter of Credit led to interrupted supply chain, impeding the company to operate at its optimum capacity during the year.

Gross profit declined by 29.76 percent in 2024 on the back of low capacity utilization, elevated rates of gas & electricity, heightened wage rate and soaring prices of raw materials. GP margin also inched down to 2.12 percent in 2024 – the lowest level recorded during the period under consideration.

Distribution expense ticked up by 2.69 percent in 2024 due to higher freight charges and increased salaries paid within the distribution chain.

Conversely, administrative expense tumbled by 21.64 percent in 2024 as the company booked no provision against doubtful debts in 2024 and also because of reduced payroll expense as the company squeezed its workforce from 813 employees in 2023 to 765 employees in 2024. Other expense shrank by 94.41 percent in 2024 primarily due to no exchange loss incurred during the year.

FRCL recorded operating profit of Rs.6.19 million in 2024 as against operating loss of Rs.41.99 million recorded in the previous year. Other income strengthened by 77.77 percent in 2024 due to higher markup income.

Finance cost grew by 29 percent in 2024 due to higher discount rate on account of markup incurred on provident fund. Conversely, gearing ratio nosedived to 24 percent in 2024 from 32 percent in 2023. FRCL recorded net loss of Rs.109.913 million in 2024, down 28.38 percent year-on-year. This translated into loss per share of Rs.2.90 in 2024.

In 2025, FRCL posted year-on-year growth of 28.40 percent in its topline which clocked in at Rs.4390.41 million. Construction sector which is the critical factor that generates the demand of FRCL’s products remained passive during the year owing to sustained period of high inflation, slow PSDP spending and cautious approach undertaken by the investors.

The company was able to drive growth in its net sales by focusing on high margin products and design oriented offerings. FRCL specifically focused on increasing the visibility and image of its brand “FORTE”.

The company also controlled its cost by optimizing its operational efficiency and tweaking its energy mix. This resulted in 19.21 percent spike in cost of sales in 2025 – much lower than the topline growth.

Gross profit strengthened by a whopping 452.28 percent in 2025 with GP margin jumping up to 9.13 percent. Distribution expense ticked down by 6.12 percent in 2025 due to lower communication and travelling expense as well as depreciation expense incurred during the year. Administrative expense ticked up by 3.41 percent in 2025 due to higher directors’ remuneration and allowance booked for ECL.

The company streamlined its workforce from 765 employees in 2024 to 732 employees in 2025. This led to a downtick in payroll expense during the year. Other expense surged by a massive 611 percent in 2025 owing to higher provisioning done for WWF and WPPF.

FRCL posted a phenomenal 4907.34 percent rise in its operating profit in 2025 with OP margin jumping up to 7 percent. Other income deteriorated by 84.63 percent in 2025 due to no rental income and a radical fall in mark-up income. Monetary easing as well as a considerable drop in outstanding long-term borrowings resulted in 79.68 percent slump in finance cost in 2025.

Gearing ratio plunged from 24 percent in 2024 to 6 percent in 2025. FRCL recorded net profit of Rs.147.495 million in 2025 as against net loss of Rs. 109.913 million recorded in the previous year. EPS clocked in at Rs.3.89 in 2025 versus loss per share of Rs.2.90 recorded in 2024.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, FRCL posted 13.59 percent year-on-year enhancement in its net sales which clocked in at Rs.1155.43 million. This was due to higher sales volume due to improvement in the macroeconomic activity. Majority of the demand was concentrated in the renovation and public sector projects with private sector demand lagging far behind.

Lately, the company has been focusing on high margin products. This coupled with cost optimization due to decline in inflation and commodity prices, stability of Pak Rupee and optimization of energy mix enabled FRCL to record 111.18 percent improvement in its gross profit in 1QFY26 with GP margin clocking in at 8.86 percent versus GP margin of 4.77 percent recorded in 1QFY25.

Enhancement of the company’s operations due to demand recovery resulted in 4.76 percent uptick in distribution expense and 11.40 percent uptick in administrative expense in 1QFY26. Other expense dipped by 4 percent during 1QFY26 probably due to lower/ no exchange loss.

Operating profit strengthened by 203.89 percent in 1QFY26 with OP margin clocking in at 6.80 percent versus OP margin of 2.54 percent recorded in 1QFY25. Other income boasted a tremendous year-on-year growth from Rs.0.55 million in 1QFY25 to 6.71 million in 1QFY26. This might be due to exchange gain recognized during the period. Finance cost hiked by 35.81 percent in 1QFY26 despite monetary easing. This is due to increase in short-term liabilities of the company.

FRCL recorded 704 percent enhancement in its net profit which clocked in at Rs.44.298 million in 1QFY26. This translated into EPS of Rs.1.17 in 1QFY26 versus EPS of Rs.0.15 recorded in 1QFY25. NP margin grew from 0.54 percent in 1QFY25 to 3.83 percent in 1QFY26.

Future Outlook

The market size of tiles has significantly contracted of-late due to diminished construction activity. This is on account of economic and political instability, heightened excise duty, property taxes, reduced purchasing power of consumers and shattered investor confidence.

While token improvement has been witnessed in the economic indicators, it will take quite some time to undo the damages done to the investor morale. Majority of the construction activity is concentrated in renovation and government projects with slow disbursements. Hence, for now, the company is focusing on attaining operational efficiency, brand visibility and tweaking its sales mix in favor of high margin products.

Comments

Comments are closed for this article.