Maqbool Textile Mills Limited (PSX: MQTM) was incorporated in Pakistan as a public limited company in 1989. The principal activity of the company is the manufacturing and sale of yarn, cotton seed and cotton lint.

Pattern of Shareholding

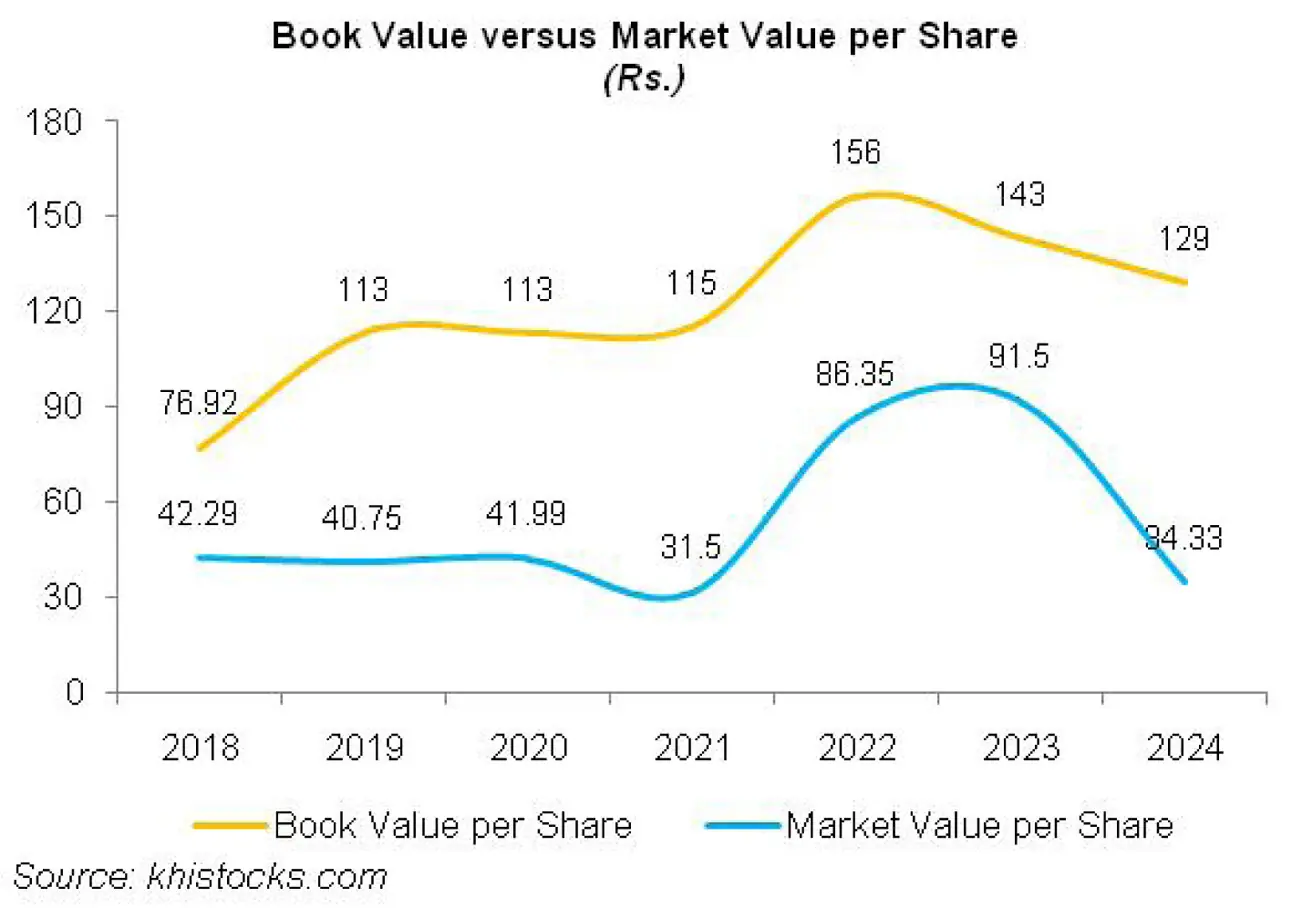

As of June 30, 2024, MQTM has a total of 18.432 million shares outstanding which are held by 574 shareholders.

Directors, CEO, their spouse and minor children have the majority stake of 55.31 percent in the company followed by local general public holding 34.82 percent shares. The remaining shares are held by other categories of shareholders.

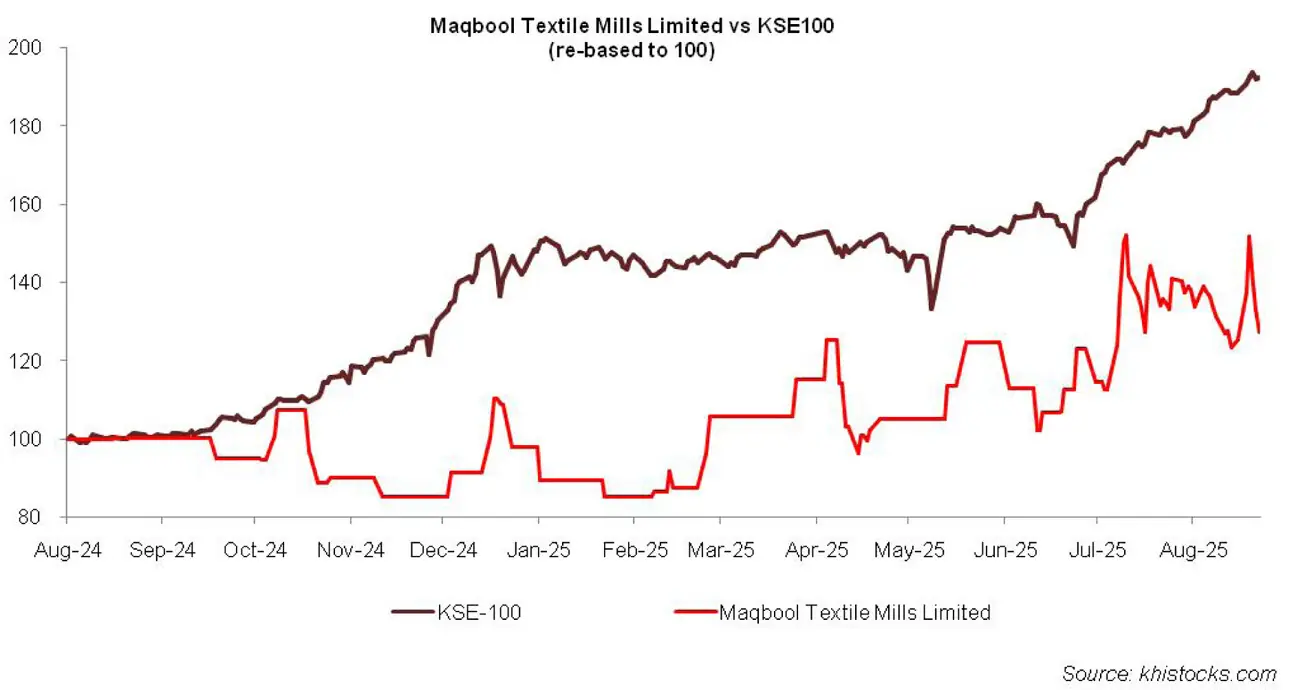

Historical Performance (2019-24)

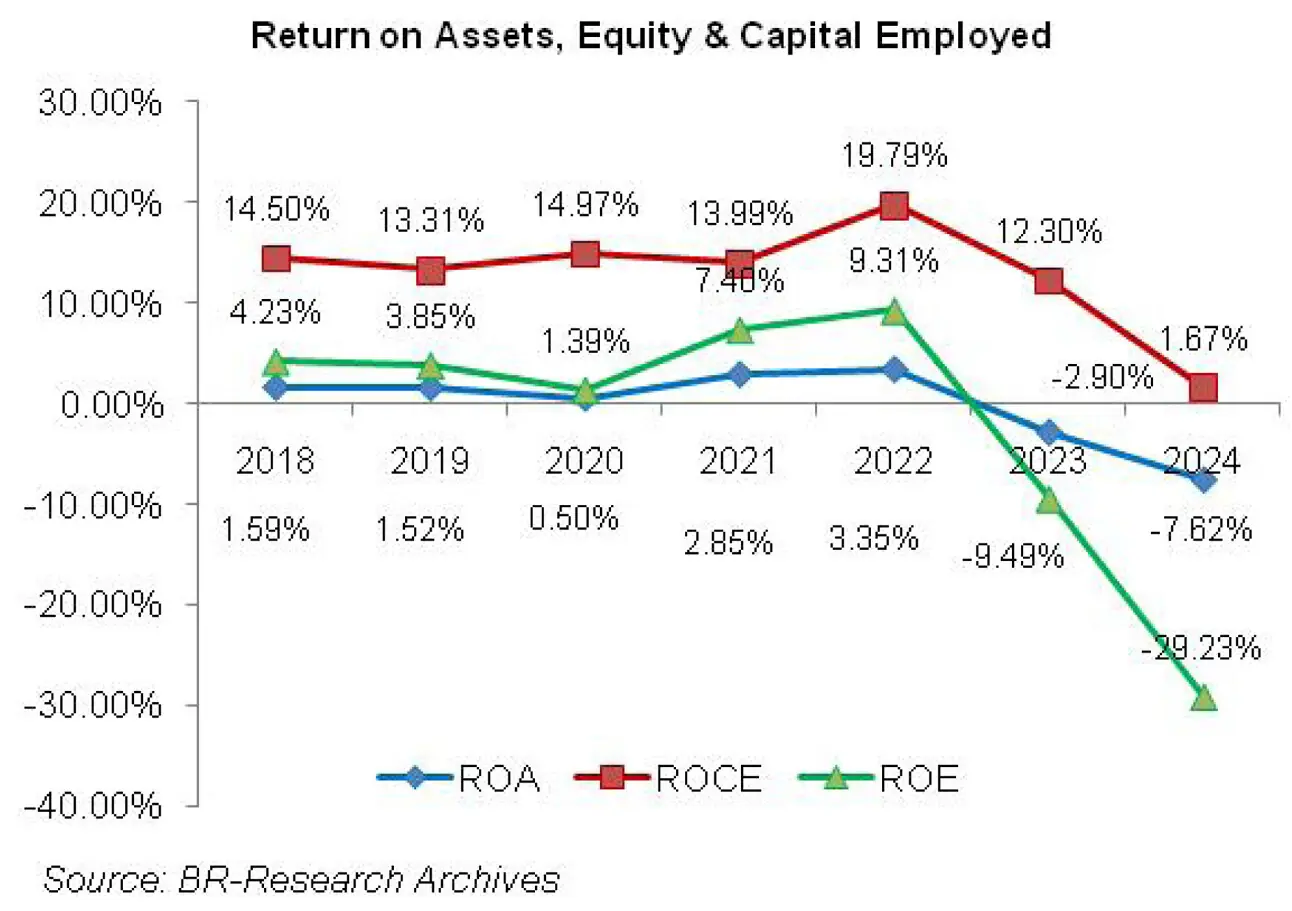

During the period under consideration, MQTM’s topline and bottomline posted a plunge twice i.e. in 2020 and 2023 with the latter year being more grievous where the company posted net loss. In 2024, MQTM’s net loss massively increased.

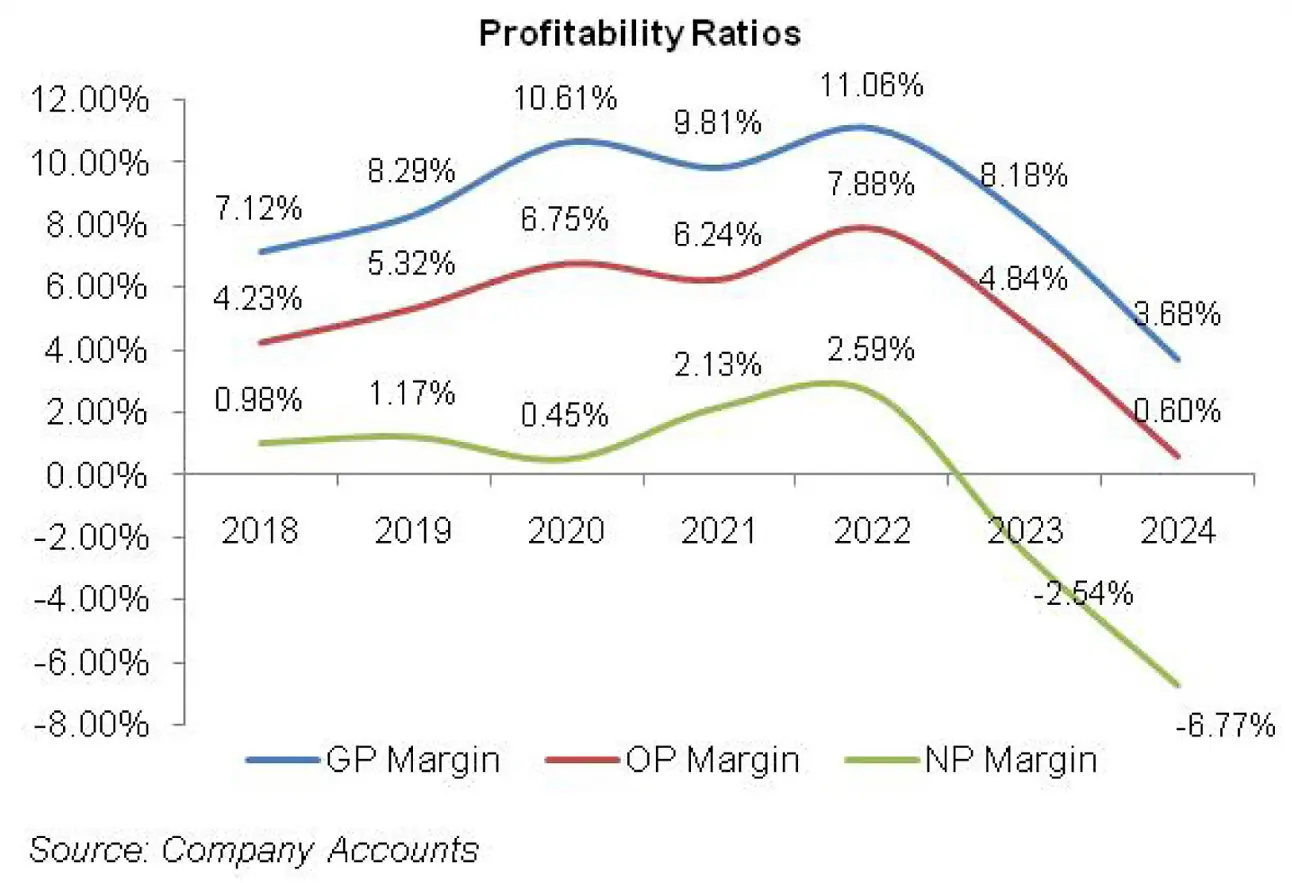

The company’s margins oscillated over the period to attain their optimum level in 2022 only to slide back in the subsequent years (see the graph of profitability ratios). The detailed performance review of each of the years under consideration is given below.

In 2019, MQTM’s topline grew by 11.36 percent year-on-year to clock in at Rs.6,234.76 million. During the year, the company enhanced its capacity from 70,440 spindles in 2018 to 81,192 spindles in 2019.

Improved sales volume coupled with upward price revision and operational efficiency achieved by the installation of modern machinery during the year culminated into 29.74 percent year-on-year rise in MQTM’s gross profit in 2019 with GP margin rising up to 8.29 percent from 7.12 percent in 2018.

Distribution expense slid by 11.90 percent year-on-year in 2019 due to lower export expenses as MQTM’s export sales took a hit in 2019 on account of global slowdown.

The company also incurred lesser export development surcharge during the year. Conversely, administrative expense hiked by 20.66 percent year-on-year in 2019 as the company hired more employees to operationalize its newly installed capacity.

This took the human resource count from 1522 in 2018 to 1561 in 2019. Other expense mounted by 1118.60 percent in 2019 due to loss incurred on the sale of fixed assets as well as higher profit related provision booked during the year.

Other expense was conveniently offset by 44.18 percent rise in other income as the company recorded exchange gain on its export sales.

Operating profit escalated by 40.11 percent year-on-year in 2019 with OP margin climbing up to 5.32 percent versus OP margin of 4.23 percent recorded in the previous year.

Finance cost surged by 34.83 percent year-on-year in 2019 on account of higher discount rate as well as increased borrowings which included running finance to meet working capital requirements and long-term financing to fund its expansion projects.

MQTM’s bottomline grew by 33.14 percent year-on-year in 2019 to clock in at Rs.72.84 million with EPS of Rs.4.34 versus EPS of Rs.3.26 posted in 2018. NP margin also inched up from 0.98 percent in 2018 to 1.17 percent in 2019.

2020 was a challenging year for the local as well as global economies as COVID-19 resulted in lockdown which severely restricted the economic activity. MQTM’s topline also succumbed to external vulnerabilities and plummeted by 6.30 percent year-on-year to clock in at Rs. 5,841.69 million in 2020.

This was due to reduced demand and suspension of production activities during the lockdown period.

As the demand of CVC yarn drastically dropped in 2020, the company changed its production and sales mix which required addition on new machinery. During 2020, the total number of spindles increased to 82,224. This helped company to somehow dilute the impact of the global pandemic on its sales.

Cost of sales declined by 8.68 percent in 2020, resulting in 19.92 percent improvement in gross profit with GP margin mounting to 10.61 percent.

Distribution cost dropped by 14.90 percent year-on-year in 2020 due to lower sales commission as well as freight and export expenses as export sales further eroded due to restriction on the movement of goods and people across borders.

Administrative expense enlarged by 11.12 percent in 2020 due to higher payroll expense despite the fact that the number of employees dipped to 1519 in 2020.

Lower profit related provisioning and high-base provided due to the sale of fixed assets in the previous year drove other expense down by 49 percent in 2020. Absence of exchange gain and warehouse rental income resulted in 98.17 percent reduction in other income in 2020.

Operating profit inched up by 18.77 percent in 2020 with OP margin rising up to 6.75 percent.

Finance cost spiraled by 52.57 percent in 2020 due to higher discount rate for most part of the year as well as increased borrowings. During the year, MQTM obtained Rs.86 million under TERF scheme of SBP for the addition of new machinery.

As a consequence, the company’s bottomline diminished by 63.76 percent year-on-year to clock in at Rs.26.39 million with EPS of Rs.1.57 and NP margin of 0.45 percent.

2021 proved to be quite cheering for MQTM as its topline expanded by 25.85 percent year-on-year to clock in at Rs.7351.74 million. This was mainly on account of robust demand from international market despite COVID-19 related challenges.

As many economies of the world were still in the lockdown state, Pakistani textile industry witnessed huge demand influx from different geographical markets. Surge in the cost of raw materials resulted in the company’s GP margin slipping to 9.81 percent despite 16.28 percent fatter gross profit recorded in 2021.

Distribution expense posted an uptick of 5.16 percent in 2021 mainly on account of higher freight and forwarding charges incurred during the year.

Administrative expense swelled by 24.79 percent in 2021 as a result of enlarged payroll expense as MQTM’s workforce witnessed massive expansion to clock in at 1669 employees. As the company disposed off its fixed assets at a gain, its other income multiplied by 614.84 percent in 2021, however, it was nullified by 18.79 percent escalation in other expense due to higher profit related provisioning.

Operating profit picked up by 16.35 percent in 2021 but OP margin declined to clock in at 6.24 percent. Finance cost gave some breather as it shrank by 28.96 percent in 2021 on account of monetary easing as well as settlement of a considerable portion of short-term loans during the year.

MQTM’s net profit mounted by 492 percent in 2021 to clock in at Rs.156.27 million with EPS of Rs.9.08 and a healthier NP margin of 2.13 percent.

MQTM’s topline continued its growth trajectory in 2022 and registered 41.21 percent year-on-year rise to clock in at Rs.10,381.07 million. This was on account of improved sales volume as well as better pricing and sales mix.

Effective capacity utilization and operational efficiency achieved by the installation of state-of-the-art machinery and equipments resulted in cost reduction. As a consequence, gross profit grew by 59.32 percent in 2022 with GP margin reaching its optimum level of 11.10 percent.

Distribution expense posted a massive 35.87 percent escalation in 2022 due to higher sales commission and export expenses incurred during the year.

Administrative expense also spiraled by 45.22 percent in 2022 as MQTM’s workforce reached an unprecedented level of 1715 employees which amplified the payroll expense.

Tremendous exchange gain recognized during the year drove other income up by 580.38 percent in 2022. This easily counterbalanced the effect of 10.70 percent higher other expense incurred on the back of increased provisioning.

Operating profit turned out to be 78.30 percent bigger in 2022 with OP margin climbing up to 7.88 percent – the highest among all the years under consideration. Finance cost surged by 68.23 percent in 2022 on account of monetary tightening as well as significantly higher short-term loans obtained during the year.

The effect of super tax imposed during the year resulted in 103.12 percent higher tax charged during the year. MQTM’s net profit registered 71.82 percent enhancement in 2022 to clock in at Rs.268.51 million with EPS of Rs.14.57 and NP margin of 2.60 percent.

Unfavorable socio-economic circumstances of the country took its toll on the net sales of MQTM which dropped by 5.24 percent year-on-year in 2023 to clock in at Rs.9,837.14 million.

Dwindling foreign exchange reserves resulted in import restrictions, making the company devoid of essential raw materials - cotton, polyester staple fiber and viscose staple fiber - resulting in reduced capacity utilization. Pak Rupee depreciation and withdrawal of subsidy on energy prices resulted in higher per unit cost.

Overall cost of sales slid by 2.17 percent in 2023 as fixed overheads couldn’t be completely absorbed, resulting in 29.91 percent shrinkage in the company’s gross profit with GP margin ticking down to 8.18 percent.

Distribution expense shrank by 38.84 percent year-on-year in 2023 on account of lower sales volume which lowered export expense, commission and freight charges.

Administrative expense enlarged by 14.36 percent in 2023 which was the effect of high inflation. Drastic decline in exchange gain during the year resulted in 35.11 percent thinner other income recorded during the year.

The company didn’t book any provision for WWF and WPPF in 2023, resulting in no other expense recorded in 2023.

As a consequence, operating profit eroded by 41.80 percent in 2023 with OP margin diving down to 4.84 percent. 102 percent spike in finance cost during the year proved to be the last nail in the coffin and translated into net loss of Rs.249.53 million in 2023 with loss per share of Rs.13.54.

In 2024, MQTM recorded 4.84 percent uptick in its net sales which clocked in at Rs.10,313.73 million. While local sales dipped during the year due to economic slowdown which resulted in demand destruction, export sales posted a staggering growth of 423.81 percent to clock in at Rs.1,974.355 million.

Cost of sales surged by 10 percent in 2024 due to withdrawal of subsidy on energy prices resulting in more than 100 percent spike in electricity cost. This coupled with higher commodity prices and Pak Rupee depreciation resulted in 52.84 percent decline in gross profit in 2024. GP margin fell to its lowest level of 3.68 percent in 2024.

Distribution expense escalated by 46.39 percent in 2024 due to higher export expense, commission as well as export development surcharge incurred during the year on the back of higher export sales.

Administrative expense dipped by 13.41 percent in 2024 due to thinner payroll expense as the company streamlined its workforce from 1703 employees in 2023 to 1041 employees in 2024. No profit related provisioning was booked during the year, resulting in no other expense.

Other income also dipped by 7.66 percent in 2024 due to lower exchange gain. MQTM posted 86.92 percent plunge in its operating profit in 2024 with OP margin falling to 0.60 percent. Finance cost escalated by 21.21 percent in 2024 due to monetary tightening as well as increased working capital borrowings. MQTM posted net loss of Rs.698.417 million with loss per share of Rs.37.89 in 2024.

Recent Performance (9MFY25)

During the nine-month period of FY25, MQTM’s net sales dwindled by 29.84 percent to clock in at Rs.5899.85 million. This was on account of a drastic decline in the demand of locally produced yarn as huge quantity of imported yarn was dumped into the local market.

The availability of surplus stock in the market resulted in a drop in prices which put further dent on the topline of MQTM in 9MFY245.

Lower capacity utilization resulted in high fixed cost per unit which coupled with exorbitant energy prices resulted in 85.44 percent slide in gross profit in 9MFY25. GP margin also deteriorated from 8.42 percent in 9MFY24 to 1.75 percent in 9MFY25.

Lower production and sales volume resulted in 71.75 percent and 33 percent drop in distribution expense and administrative expense respectively in 9MFY25. 346.36 percent growth in other income in 9MFY25 appears to be the result of exchange gain.

MQTM posted operating loss of Rs.78.90 million in 9MFY25 versus operating profit of Rs.377.32 million recorded in 9MFY24. Monetary easing coupled with a decline in short-term borrowings resulted in 15 percent lower finance cost in 9MFY25.

Net loss mounted by 149.39 percent to clock in at Rs.596.357 million in 9MFY25. This translated into loss per share of Rs.32.36 in 9MFY25 versus loss per share of Rs.12.97 posted in 9MFY24.

Future Outlook

The lingering impact of the global recession continues to cast substantial influence on the overall economy, including the country’s textile industry. Elevated power costs and unpredictable natural gas availability will persistently diminish profit margins.

However, the company is making continuous efforts to reduce its energy cost by installing solar power plant and low energy consuming motors. This coupled with monetary easing bode well for the financial performance of the company.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.