Service Industries Limited (PSX: SRVI) was incorporated in Pakistan as a private limited company in 1957 and later turned into a public limited company. The company is engaged in the purchase, manufacturing and sale of footwear, tyres and tubes as well as technical rubber products.

A huge portion of SRVI’s sales revenue comes from export markets particularly European market. The company has also started expanding in the US, Australia and Middle East.

Pattern of shareholding

As of December 31, 2024, SRVI has a total of 46.987 million shares outstanding which are held by 1710 shareholders. 40.37 percent of the company’s shares are held by its Directors, CEO, their spouse and minor children followed by local general public holding 31.56 percent shares of SRVI.

NIT and ICP account for 12.03 percent shares of the company while associated companies, undertakings and related parties have a stake of 9.66 percent in SRVI. Modarbas and Mutual funds account for 2.74 percent shares while pension funds hold 1.30 percent shares of SRVI. Around 1.07 percent of the company’s shares are held by joint stock companies. The remaining shares are held by other categories of shareholders.

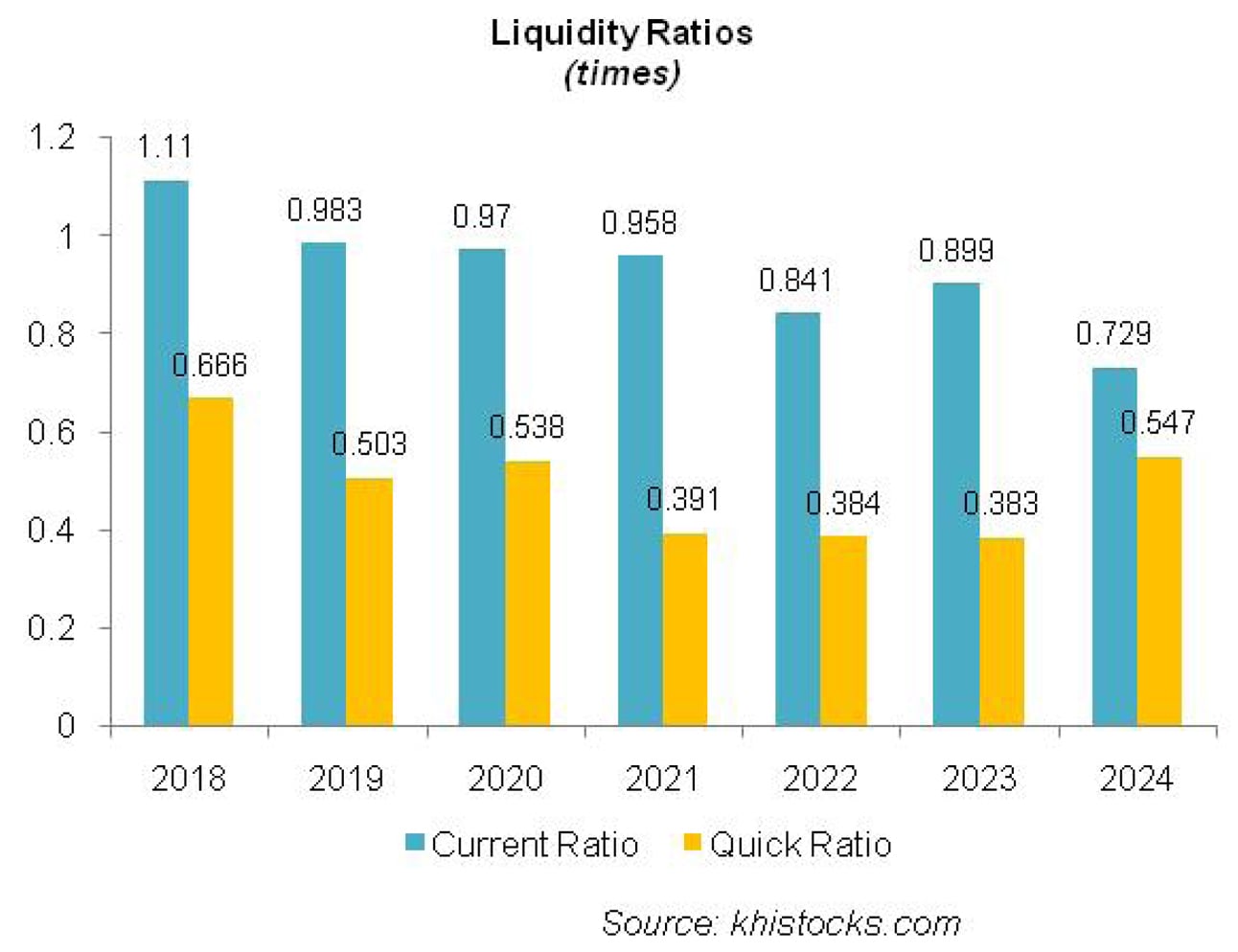

Historical Performance (2019-24)

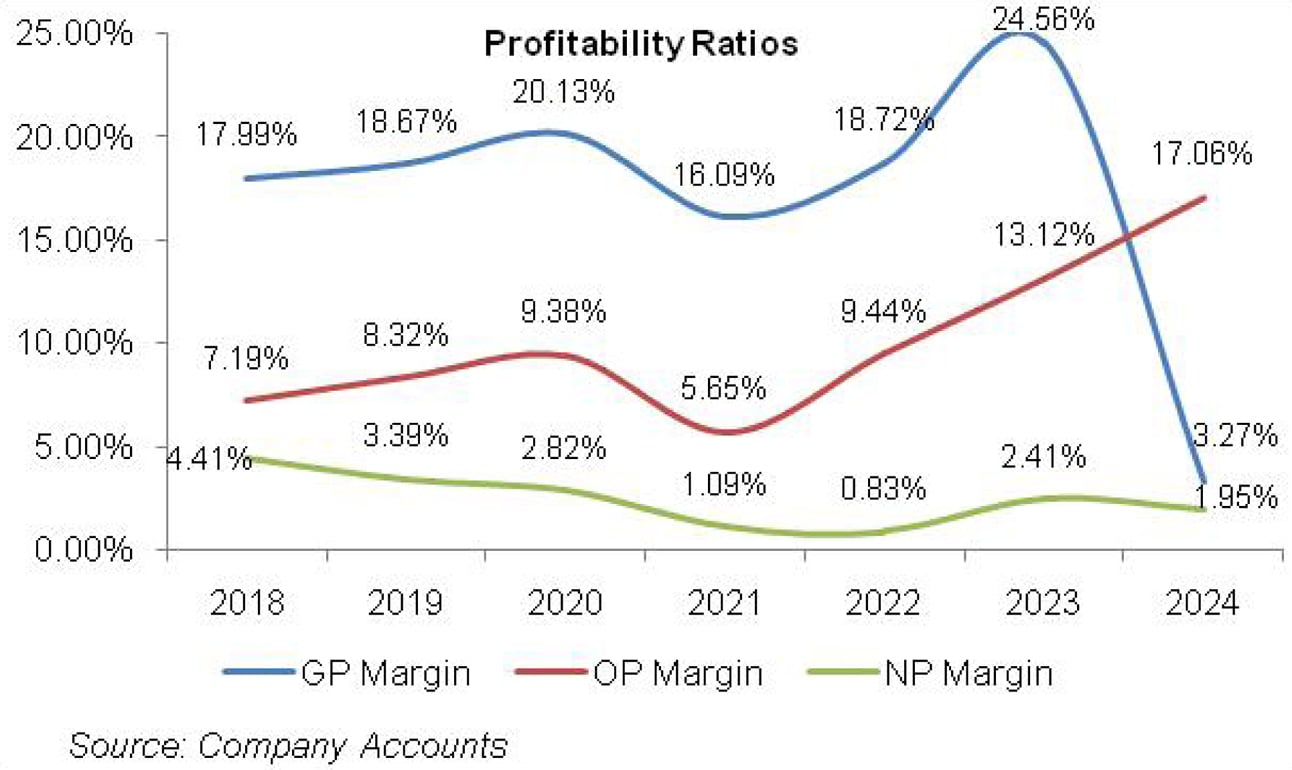

SRVI’s topline slid twice during the period under consideration i.e. in 2020 and 2024. Conversely, its bottomline which had been constantly ticking down until 2022 recorded a staggering rebound in 2023. This was followed by a drastic decline in bottomline in 2024. SRVI’s gross and operating margins which had been ascending until 2020 significantly plunged in 2021.

In the subsequent two years, GP and OP margins considerably recovered. In 2024, gross margin registered a steep fall while operating margin attained its optimum level. SRVI’s net profit margin followed a descending trend since 2019 and bottomed out in 2022. This was followed by a significant rise in 2023 and then a dip in 2024. The detailed performance review of the period under consideration is given below.

In 2019, SRVI’s topline grew by 8.62 percent year-on-year to clock in at Rs.26,156.20 million. This came on the back of local sales which grew by 20 percent during the year. Conversely, export sales shrank by 13 percent during 2019. Across the product categories, sales of tyres posted a momentous growth both in local and export markets and continued to be the mightiest source of revenue for SRVI to clock in at Rs.15,960 million in 2019 (61 percent of total revenue). 2019 was the year when the company began agricultural tyre production which received an overwhelming response from the market.

Sales revenue from technical rubber products also inched up during the year, however, only in local market, while no sales of this product category was made in the export market. Technical rubber products contributed only Rs.231.18 million to the topline of SRVI which was less than 1 percent of the total sales revenue of 2019.

Sales of footwear weakened in 2019 mainly on the back of lower export sales while local footwear sales also posted a marginal growth. Overall, the footwear category contributed Rs.9,964 million to the topline in 2019 which was roughly 38 percent of SRVI’s total sales revenue of 2019.

Despite high cost of sales on account of high inflation, gross profit grew by 12.73 percent year-on-year in 2019 with GP margin climbing up to 18.67 percent from GP margin of 18 percent recorded in 2018. Operating expense grew by 7.83 percent year-on-year in 2019 mainly on account of market induced rise in salaries, higher freight and insurance charges, tremendous growth in advertising and publicity budget as well as sample charges.

Other expense grew by 39 percent year-on-year in 2019 mainly on the back of higher provisioning against expected credit losses. However, other expense was counterbalanced by other income which posted a stunning 57.29 percent year-on-year growth on account of robust exchange gain.

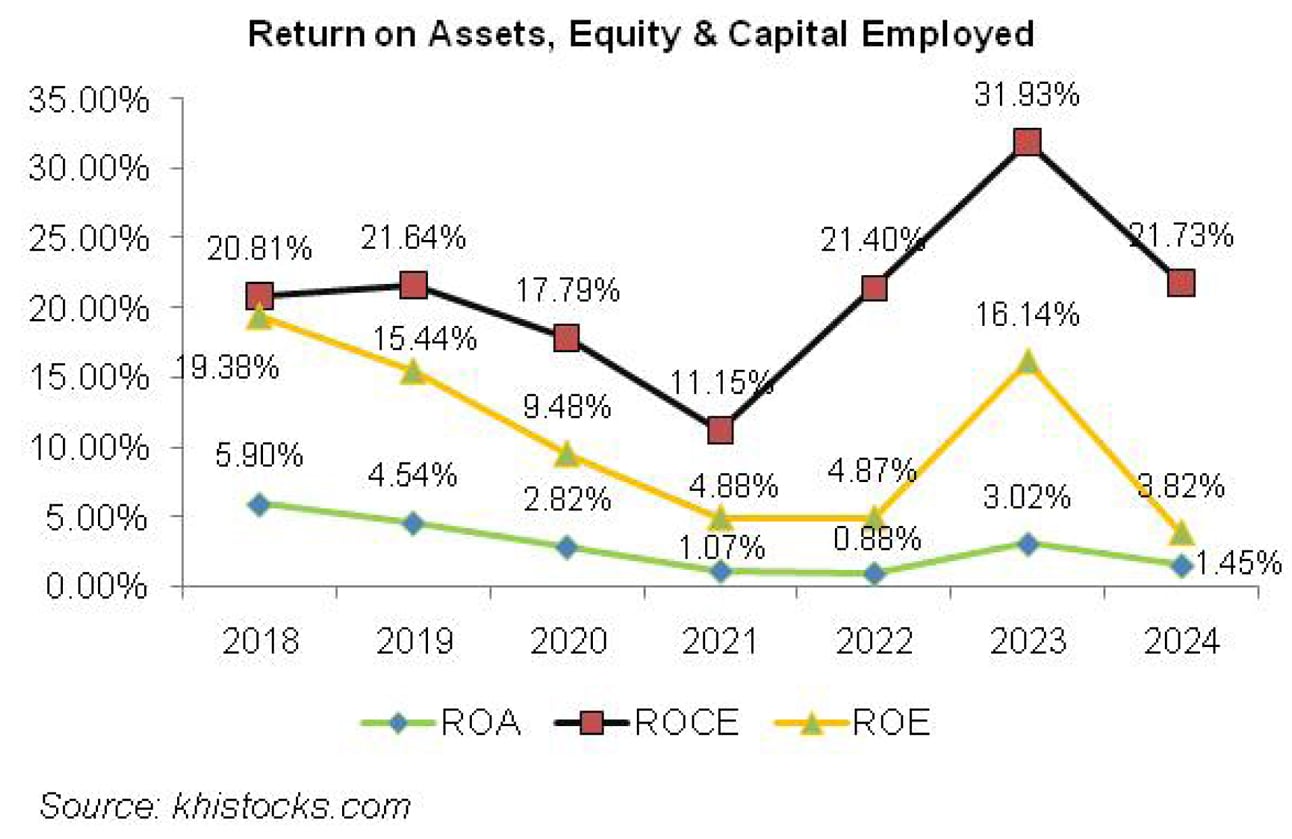

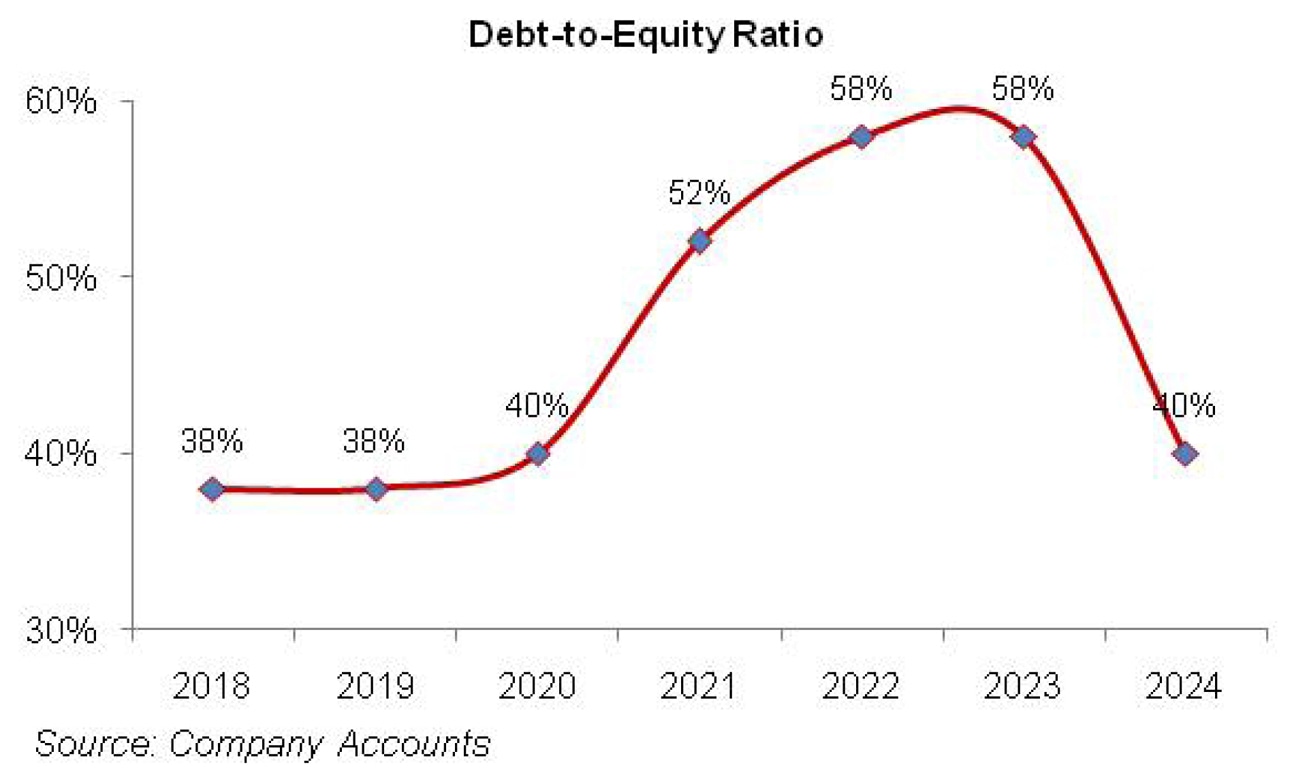

Operating profit grew by 25.78 percent year-on-year in 2019 with OP margin rising from 7.19 percent in 2018 to 8.32 percent in 2019. Finance cost drastically grew by 90.78 percent year-on-year in 2019 on the back of high discount rate. Debt-to-equity ratio stayed at 38 percent for the third consecutive year in 2019.

The growth in finance cost pushed the net profit down by 16.48 percent year-on-year in 2019 to clock in at Rs.886.36 million with NP margin of 3.40 percent down from NP margin of 4.41 percent posted in 2018. EPS also descended from Rs.56.47 in 2018 to Rs.37.73 in 2019.

In 2020, SRVI’s net revenue slumped by 6.55 percent year-on-year to clock in at Rs.24,442.49 million. The company had to suspend its operations owing to the lockdown imposed due to outbreak of COVID-19 and hence the capacity remained underutilized.

The major hit to the topline came from export sales which were almost halved in 2020 to clock in at Rs.3001.45 million due to restrictions on the movement of people and goods on account of COVID-19. Local sales grew marginally by 8 percent year-on-year to clock in at Rs.21,394 million in 2020. A sneak into the categories shows that footwear sales posted major slump of 40 percent year-on-year due to massive drop in export sales.

Sales of tyres grew by 12.7 percent year-on-year and it contributed around 74 percent to the topline. The export sales of technical rubber products were discontinued in 2019, while local sales in this category almost doubled in 2020, yet failed to produce any significant impact on the topline as its share in the overall revenue hovered around 1.9 percent in 2020. Reduced operational activity resulted in year-on-year drop of 8.23 percent in cost of sales.

This drove the GP margin up to 20.13 percent in 2020. Operating expense also slid by 8.57 percent year-on-year in 2020 due to curtailed expenditure on freight and insurance, advertising and publicity as well as a significant drop in samples expense. Other expense grew by 30 percent year-on-year in 2020 on the back of additional allowance booked for expected credit losses as well as higher provisioning done for WWF and WPPF.

Other income dwindled by 56.96 percent year-on-year in 2020 due to massive drop in exchange gain on the back of lesser export sales. Operating profit grew by 5.40 percent year-on-year in 2020 with OP margin rising up to 9.38 percent. Finance cost dropped by 3.47 percent year-on-year in 2020 due to monetary easing to spur business activity amidst COVID-19.

The dip in finance cost was registered even after an increase in the long-term and short-term borrowings of the company during the year. The debt-to-equity ratio of SRVI surged to 40 percent in 2020. The bottomline dropped by 22.15 percent year-on-year in 2020 to clock in at Rs.690.02 million with NP margin of 2.82 percent. EPS also dropped to Rs.14.69 in 2020.

In 2021, SRVI’s topline boasted the highest ever growth of 33.89 percent year-on-year to clock in at Rs.32,724.92 million. Tyre division continued to be the main growth contributor. The revenue from tyre division grew by 37.5 percent year-on-year to clock in at Rs.24,747 million in 2021 with a share of 76 percent in the overall sales mix. Sale of footwear and technical rubber products grew by 21 percent and 59 percent respectively in 2021.

Footwear division had a contribution of 22 percent in the sales mix of SRVI. The remaining 2 percent was contributed by the technical rubber products. High inflation, energy and fuel prices as well as Pak Rupee depreciation pushed the cost of sales up by 40.66 percent year-on-year in 2021. Consequently, GP margin dropped to 16.1 percent in 2021. High ocean freight charges, increased salaries and benefits as well as higher advertising and promotion budget resulted in 33.94 percent year-on-year hike in operating expense.

Other expense dropped by 58 percent year-on-year in 2021 on account of lesser allowance booked for expected credit losses as well as lesser provisioning done for WWF and WPPF. Conversely, other income magnified by 110.20 percent year-on-year in 2021 primarily on the back of scrap sales and amortization of government grant. Operating profit shrank by 19.33 percent year-on-year in 2021 with OP margin drastically falling to 5.65 percent.

Despite monetary easing, finance cost grew by 21.19 percent year-on-year in 2021 due to considerable rise in borrowings during the year. SRVI’s debt-to-equity ratio further climbed up to 52 percent in 2021. The bottomline nosedived by 48.29 percent year-on-year in 2021 to clock in at Rs.356.83 million with NP margin of 1.1 percent. EPS also dropped to Rs.7.59 in 2021.

SRVI’s topline further grew by 30.17 percent year-on-year to clock in at Rs.42,599.48 million in 2022. The growth came on the back of tyre and footwear division which grew by 27 percent and 50 percent respectively during 2022 while sales of technical rubber products contracted during the year.

Cost of sales grew by 26.10 percent year-on-year; however, robust sales volume as well as upward price revision pushed the gross profit up by 51.40 percent year-on-year in 2022. GP margin regained its lost momentum and clocked it at 18.72 percent in 2022. Increase in export sales during the year resulted in high freight charges.

Besides, higher salaries and wages as well as advertisement and publicity expense culminated into 35.85 percent year-on-year increase in operating expense in 2022. Write off of assets as well as higher allowance for expected credit losses and WPPF as well as generous donations pushed other expense up by 168 percent in 2022.

However, it was counterbalanced by 280.10 percent rise in other income on account of sky-rocketed dividend income recognized during 2022. Operating profit surged by 117.38 percent year-on-year in 2022 with OP margin of 9.44 percent. Excessive monetary tightening and increased borrowings produced 133.97 percent growth in finance cost in 2022. Debt-to-equity ratio further climbed up to 58 percent in 2022. SRVI’s profit before tax in 2022 was by 70.98 percent year-on-year. However, higher provision for taxation shoved net profit down by 0.67 percent year-on-year to clock in at Rs.354.43 million in 2022. NP margin dropped to 0.83 percent while EPS clocked in at Rs.7.54 in 2022.

2023 brought lucky streak for SRVI with year-on-year topline growth of 30.86 percent. This drove the net sales up to Rs.55,744.03 million. This was backed by an increase in the prices and volumes of both tyre and footwear division. Tyre division’s sales posted a year-on-year growth of 25 percent in 2023 with its exports strengthening by 87 percent during the year on account of increased off-take and Pak Rupee depreciation.

The revenue of footwear division grew by 45 percent year-on-year in 2023 which was primarily driven by growth in retail business. 83 new outlets were opened during the year which took the tally to 232 as of December 31, 2023. Gross profit grew by 71.70 percent year-on-year with GP margin climbing up to its optimum high level of 24.56 percent in 2023.

Operating expense grew by 39.28 percent year-on-year in 2023 on the back of elevated payroll expense, freight & insurance charges as well as publicity & advertising expense incurred during the year. Other expense dipped by 12.25 percent in 2023 as lesser assets were written off during the year.

Other income plunged by 42 percent in 2023 due to thin dividend income which eclipsed the effect of higher exchange gain and lofty scrap sales recorded during the year. SRVI’s operating profit multiplied by 81.84 percent in 2023 with OP margin climbing up to 13.12 percent. Finance cost escalated by 63.26 percent in 2023 due to high discount rate. Debt-to-Equity ratio stayed at 58 percent in 2023. SRVI registered 278.68 percent growth in its net profit in 2023 which clocked in at Rs.1342.136 million with EPS of Rs.28.56 and NP margin of 2.4 percent.

In 2024, SRVI’s net sales radically dropped by 70.16 percent to clock in at Rs.16,636.19 million. This was the lowest topline recorded by the company over the period under review. During the year, the company entered into a scheme of arrangement for the de-merger of its tyre undertaking, retail undertaking and Speed (Private) Limited shares to its wholly owned subsidiaries. This was the reason for the massive decline in SRVI’s net sales during the year.

Cost of sales dipped by 61.73 percent in 2024. Gross profit declined by 96 percent in 2024 with GP margin falling down to 3.27 percent. The transfer of three of its businesses to its subsidiaries resulted in 85.53 percent slump in operating expense in 2024. This was due to a decline recorded in salaries expense, freight & insurance charges, advertising & publicity expense, fuel & power charges, depreciation and travelling expense.

Number of employees was reduced from 7902 employees in 2023 to 1905 employees in 2024. After the demerger, other income proved to be the main source of income for the company. In 2024, SRVI’s other income mounted by 431.19 percent to clock in at Rs.3,307.05 million out of which dividend income accounts for Rs.2788.316 million. SRVI also recorded interest income on loan to subsidiaries and rental income in 2024 which also contributed in driving up its other income.

Operating profit thinned down by 61.20 percent in 2024, however, OP margin reached its optimum level of 17 percent. Finance cost tumbled by 56.75 percent in 2024 due to decline in short-term and long-term borrowings outstanding at the end of the year. Debt-to-equity ratio fell from 58 percent in 2023 to 40 percent in 2024. SRVI recorded net profit of Rs.324.421 million in 2024, down 75.83 percent year-on-year. This translated into EPS of Rs.6.90 and NP margin of 1.95 percent in 2024.

Recent Performance (1QCY25)

After the restructuring of its operations in 2024, SRVI operates as a holding company which maintains a diversified portfolio in varied sectors through its subsidiaries. During the first quarter of the ongoing calendar year, SRVI’s net sales improved by 90.24 percent to clock in at Rs.2454.50 million. The growth primarily came on the back of higher local sales of tyres and footwear. Cost of sales mounted by 113 percent in 1QCY25. This resulted in 16.27 percent diminution recorded in gross profit in 1QCY25 with GP margin falling down to 7.75 percent from GP margin of 17.6 percent recorded in 1QCY24.

Operating expense tumbled by 5.50 percent in 1QCY25 due to lower salaries, advertisement & promotion, freight & insurance, fuel & power as well as travelling expense incurred during the period. Other income dipped by 25.63 percent in 1QCY25 seemingly due to lower interest income on account of monetary easing. SRVI recorded 28.84 percent thinner operating profit in 1QCY25 with OP margin clocking in at 17.59 percent versus OP margin of 47 percent recorded during the same period last year.

Monetary easing as well as lower working capital requirements resulted in 5.64 percent lower finance cost in 1QCY25. Net profit clocked in at Rs.64.875 million in 1QCY25, down 83.45 percent year-on-year. This translated into EPS of Rs.1.38 in 1QCY25 versus EPS of Rs.8.34 recorded in 1QCY24. NP margin also severely fell from 30.38 percent in 1QCY24 to 2.64 percent in 1QCY25.

Future Outlook

The company expects that the restructuring and realigning of its segments will result in improved focus and better performance of all the segments in the future.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.