The debate over early start of crushing has dominated discussions of sugar supply-demand availability this season. The industry is of the view that early start of crushing is responsible for opportunity loss of 0.3 million tons of incremental sugar production, blamed on loss of sucrose recovery. On the other hand, Cane Commissioner Punjab has rubbished these claims, insisting that recovery is above par.

The administration’s position adopts a public policy perspective, which goes as follows. Delayed crushing means delay in harvest of sugarcane, which leads to loss of optimal wheat sowing season. Not only this means lower wheat availability resulting in loss of domestic self-sufficiency, it also means that farmers are stuck with growing sugarcane year after year, irrespective of economic returns.

While notification of crushing season clearly leads to overt government intervention in private markets, it is also very necessary as public policy must adopt a holistic perspective and strike a balance between profit motive of sugar mill owners, and farmer’s agency to freely choose crop preferences. Or so argues the government.

Even if the sugar industry’s grievance over lower recovery levels is taken on face value, the concerns over loss of wheat sowing means policymakers face no easy choices. If markets were completely free, one might argue that those farmers who wish to retain agency to plant wheat should switch away from sugarcane altogether. But that would neither work in favour of sugar mills nor government, as the former will face raw material shortage, while the latter will face a ballooning refined sugar import bill to meet shortfall.

On the other hand, notification of mandatory crushing means sugar mills alone have to bear the brunt of a lopsided policy. And that appears to be true even if industry’s position over lower recovery is completely disregarded, as insisted by cane commissioner. Here is how.

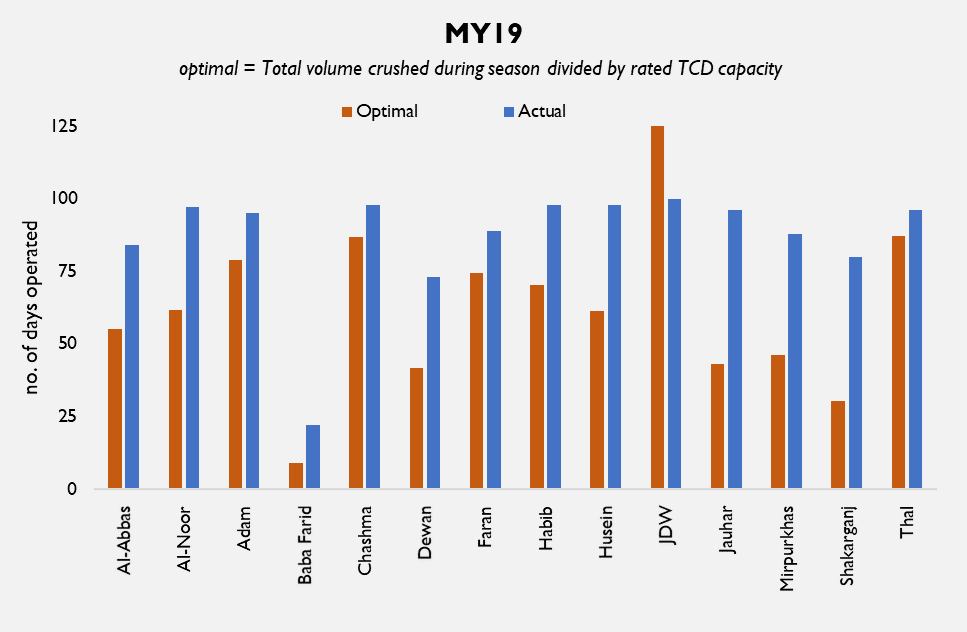

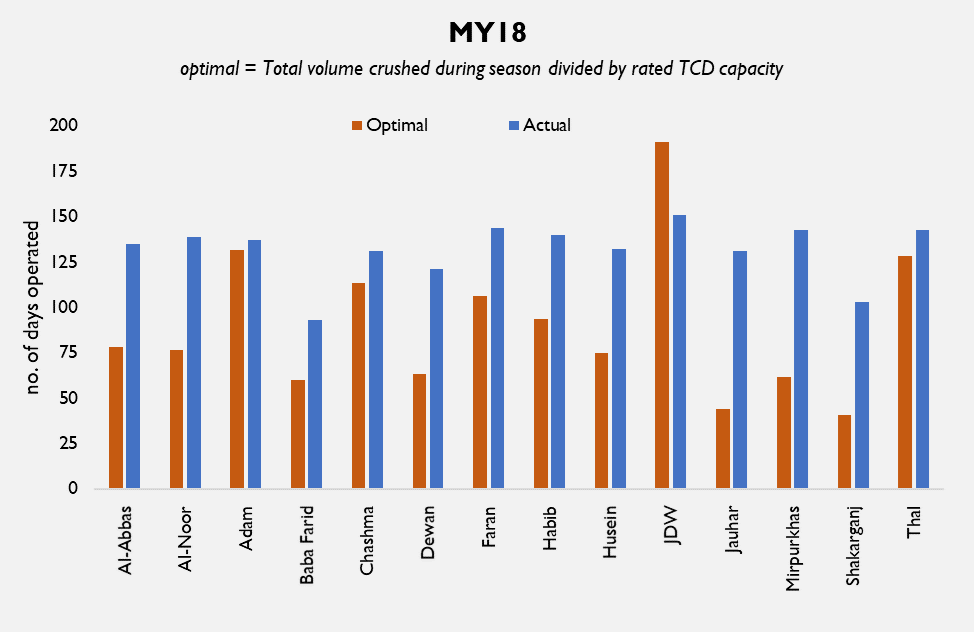

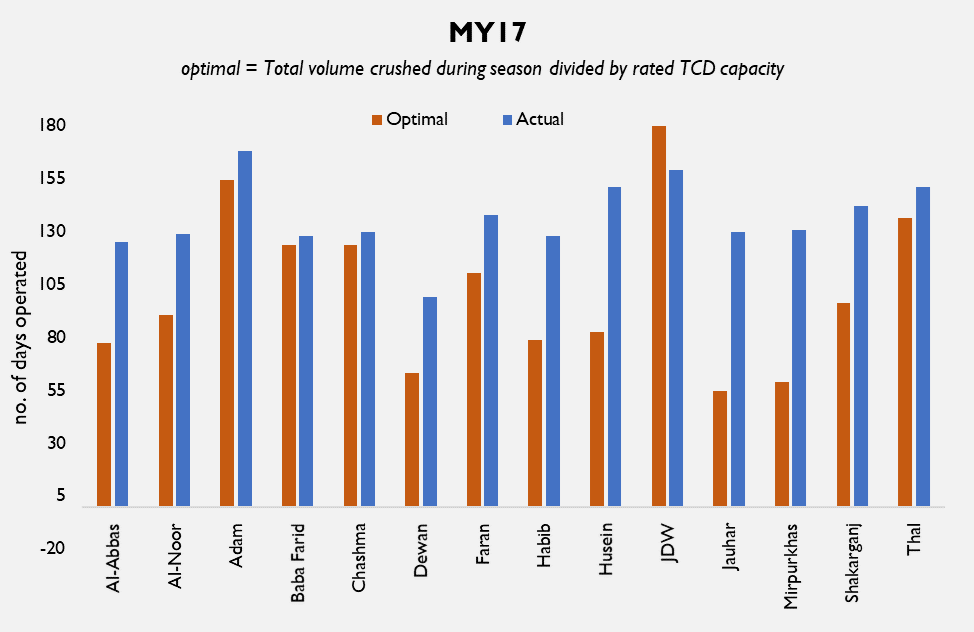

Once the crushing season begins, sugar mills operate 24/7. In order to minimize overheads related to plant operations, that means mills must crush (process) available (purchased) cane in as little time as possible, limited only by their plant capacity. Based on available information for selected listed sugar companies, BR Research conducted an in-depth analysis of the volume of sugarcane crushed and number of days operated over a 5-year period, and found interesting results.

Because supply of sugarcane is not readily available once the crushing begins, that means all except one sugar mill included in the sample operates for longer period than if they were to operate on optimal plant capacity per day. And excess number of days operated is not small by any stretch; most mills operate for an additional one month than necessary.

This is especially fascinating considering that the sample period included both two seasons of surplus crop (MY17 and MY18), and two seasons of shortfall (MY19 and MY20). To uninitiated readers, while 30 odd additional operating days may not sound a lot, it may be worth recalling that most mills operate for four to five months on average, where 25 to 30 incremental days of operation translates into 25 to 33 percent additional operating time than required – spent operating under capacity.

While it is hard to measure the full impact of this policy (in absence of industry wide information), it goes without saying that under utilization must translate into higher cost of production per unit. This would be further compounded, if you give industry’ claims concerning loss of recovery any credence.

Of course, a quick rebuke would be that mills are forced to underutilize capacity as they have increased capacity unlawfully. But in most cases, capacity enhancements in the industry are result of BMR and not plant expansions. Should the regulator also police measures taken by private business to improve plant efficiencies?

There may be no easy answers to these questions, but industry’s claims regarding mandatory crushing are worth a hearing. Meanwhile, the industry would also do well if it were to presents its narrative more cogently, instead of relying on hyperbole regarding ‘losses of billions’. Technical research is needed from both sides of the debate; but can anybody be bothered?

Comments

Comments are closed for this article.