As per monthly CPI for Feb-20 released earlier this week, poultry prices have once again leapt forward by an enormous 38.2 percent (over Feb-19), throwing expectations off taming down inflation out of whack. While many will insist that the wild ride of poultry represents peak food volatility and should as such be discounted, it appears poultry has found a new price level, one that has been long in the waiting.

Why? The short answer is ‘perception’ of maize supply gap. Although formal sector poultry players may place maize component in overall cost of poultry production at as low as 20 percent, it may help to recall that most of poultry farming in the country is still semi-formal. Mid-sized players raising poultry follow bare minimum feed standards and are more inclined to increase maize component for cost minimization.

Since FY18-FY19 when rupee began its downward slide against dollar, semi-formal players began their increasing substitution of imported components such as soybean with cheaper – and largely locally produced and procured – inputs such as maize. Here it might also help to emphasize that while inputs such as soybean are a valuable source of protein, maize is a source for carb- rich diet, allowing growers to quickly fatten the broiler bird.

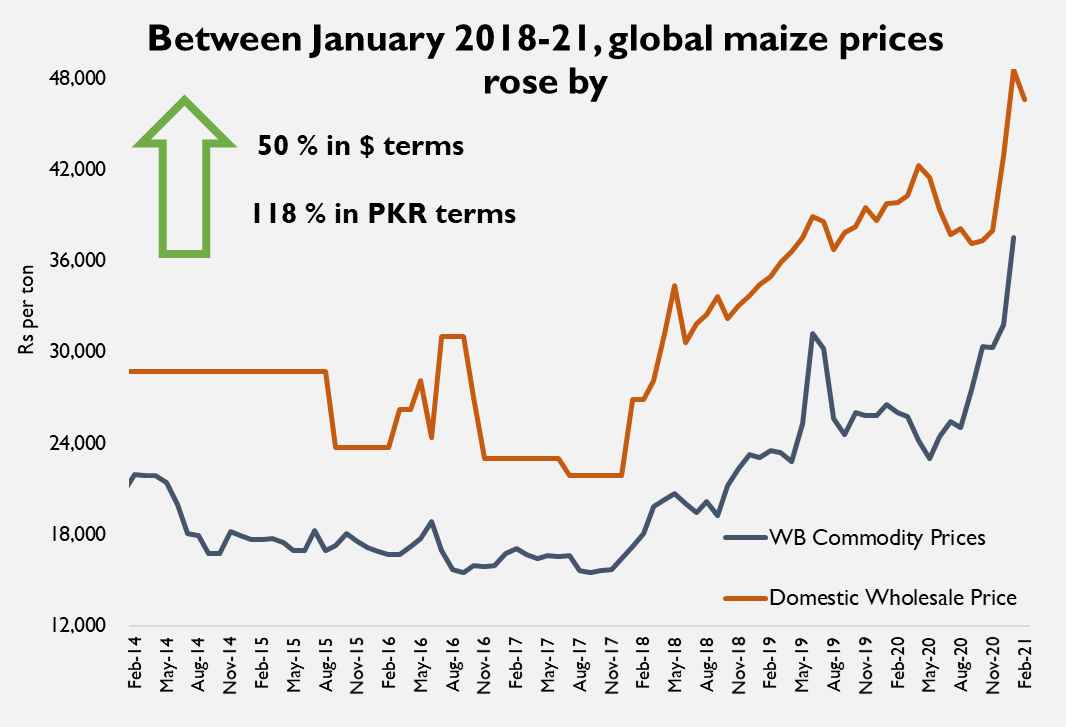

Enter global demand for maize with a twist. After bottoming out in CY17 when per ton maize price averaged at $160, international maize prices have been on a bull run since January 2018, rising by a 13 percent CAGR in the past three years. As of Jan-21, global maize prices are at a 7-year high with little signs of relenting.

Although international commodity market has seen much worse in the past – between CY11 to CY13, maize prices had averaged close to $300 per ton - the timing of bull run could not have been more unfortunate for domestic poultry industry. Over the past 18 months, currency depreciation appears to have made export prospects for maize particularly attractive, resulting in year-on-year export volume growing by 13 times in FY20, with a whopping 16 times rise in total Rupee value.

Meanwhile, the lockdown sideshow proved to be an effective distraction for market dynamics. Uncertainty ruled over commercial demand for poultry as the economy flirted with on-again, off-again strategy viz permanent return of public attendance to schools, offices, restaurants, and wedding banquets. Because poultry has a limited and very short lifecycle, every time people went back homes, commercial demand took a dip, sending prices of day-old-chicken on a rollercoaster ride.

Further twist was added by maize crop performance in recent past. Over the past decade, improving yield resulted in healthy surpluses for several seasons. Anticipating another surplus year, it appears that the commodity traders went all in on maize export during last year, dispatching highest ever volumes on the back of improved unit prices in FY20.

But it may help to take pause for a moment. If government supplied figures are anything to go by, even the highest ever export volume in FY20 was only about two percent of total domestic output. Thus, while the growth rate may have been significant, the absolute volume is not significant enough to cause a shortfall domestically, unless of course maize demand has risen dramatically in the last 24 months.

Then why are maize prices increasing? Because the liberal trade regime for the crop has ensured that prices in domestic market remain pegged to international market movement. Thus, the fact that maize farmers have been doing tremendously well in the past decade has much to do with international commodity price that has been consistently inching forward for over three years now.

Thus, before broiler becoming precious provokes a knee jerk reaction or leads to ban on maize export, caution is warranted. Growers have benefited from the bonhomie, leading to more acres being brought under maize cultivation and improved investment in inputs. Focus should be placed on improving crop productivity to ensure that output is sufficient to cater to both – demand from local poultry feed segment as well as that of opportunist traders bringing in foreign exchange through export.

Note: Domestic prices are extrapolated based on Lahore Monthly Wholesale Prices available in MNFS&R documents for up to June 2018. For the period between July 2018 – February 2021, WPI index values for maize have been used to extrapolate domestic price level; and is as such indicative.

Comments

Comments are closed for this article.