Has the ‘powerful sugar milling lobby’ blinked under pressure from the federal government? Although wishful thinking would insist so, statistics from the central banks offer a mixed picture.

It has long been argued in this space that the sugar stocks in the country were to reach dead level by November end, given lowest production in a decade during MY20 season and historic domestic consumption trends (For the latest coverage, read ‘Time to short on sugar?’, published on November 24, 2020, by BR Research).

Some flashback. Back in peak summer consumption months, news of low stock position in the country – coupled with delays in import due to jarring indecisiveness displayed by MoC – played havoc with speculative markets beginning July to August. Retail price of sugar skyrocketed from near Rs 80 in June to almost a hundred in several cities across the country, as sugar dealers rushed to lift stocks from the mills against cash payments.

To put water on the speculative fire, MoIP and Punjab government sprang into action, imposing punitive measures and monetary fines in case the sugar mills delayed crushing once the season was notified by respective provincial governments. The arcane regulations of The Sugarcane Act were going to be enforced after a long time. Now, it is claimed that the ‘stick only’ strategy adopted by the administration has played a role in forcing millers’ hand – resulting in ‘timely’ start of crushing by mills and bringing retail prices down.

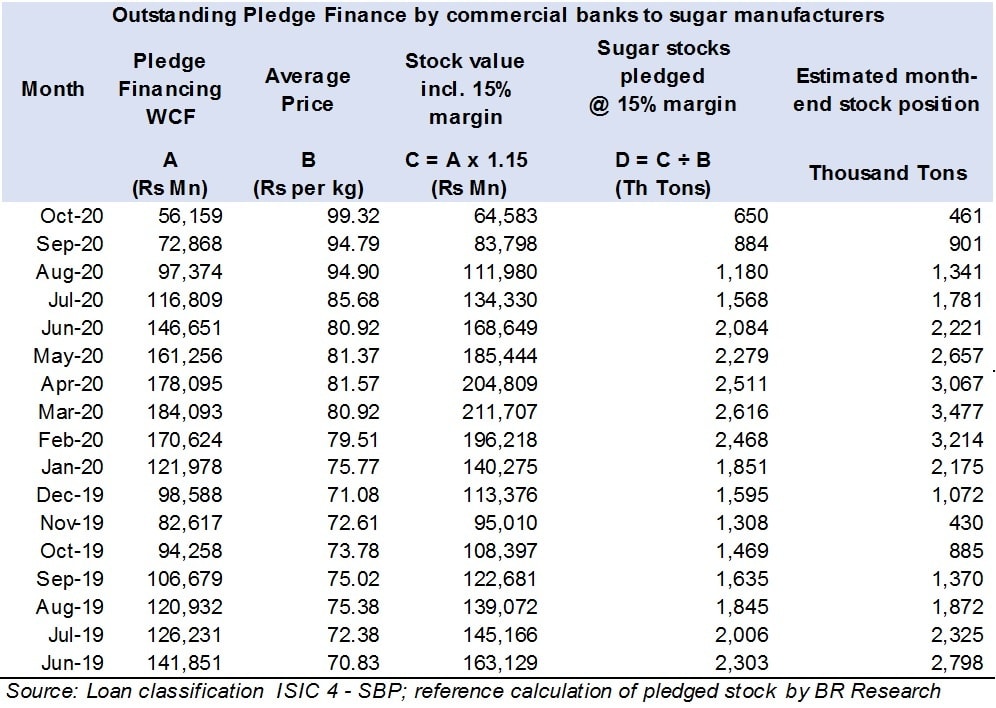

The verdict – is at best – mixed. Private sector credit statistics from the central bank show that sugar stocks pledged with commercial banks by end of October were no more than 5 weeks of domestic consumption at most (if not even lower)!

So, did sugar mills finally give into national interest and help put end to a looming crisis by starting to crush on time? Or did fear of takeover of mills by administration paid dividends? Both are possibilities but consider a third option.

If there is one thing sugar millers know better than any other industry in this country, its maximizing profits by averaging out selling price throughout the year by timing their inventory positions. By beginning of November, when most mills (should) had almost run out of stocks, the benefit of any speculative increase in market prices would have been accrued by sugar dealers and wholesalers sitting on those stocks – not the millers. The public, media, and administrative ire on the other hand, would have been directed on the milling industry.

Thus, mills effectively had the following choice set. A- Start crushing late as per tradition: by waiting for weakening of bargaining power of growers so they may sell cane at throw away prices by Dec-Jan. Or B-, Start crushing early so there is still time to ride (now nearly ending) wave of peak sugar prices - that is, while ex-factory prices are still over Rs 80 per kg – and reap the benefit of peak prices instead of letting the dealers/wholesalers to aggravate the speculation and benefit on industry’s expense.

Hard ball played by MoIP? Maybe. Sugar millers giving into national interest? Not, so much.

Comments

Comments are closed for this article.