The first quarter (1QFY21) post Corona-quarter (4QFY20) was an encouraging one in terms of exports. Anyone looking for the pre-Covid levels to return immediately should think twice. Pakistan may well have fought the pandemic rather well, but the world is still battling with the one wave or the other. Global economy is nowhere near any semblance of normalcy. In that context, the export rebound is rather encouraging.

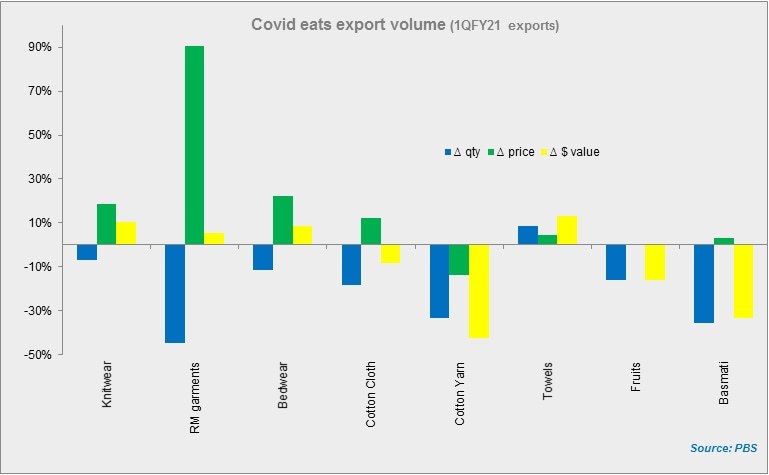

Textile exports during 1QFY21 at $3.47 billion are very much at par with the past six quarters before the pandemic (minus 4QFY20). This is rather encouraging despite the ongoing pandemic that continues to engulf Pakistan’s key textile export destinations in Europe and the USA. The variables in the textile export equation have switched roles, as the quantity growth story has now been replaced with growth in unit prices.

The most telling tale within the textile group is that of the readymade garment exports, which have apparently moved a ladder or two ahead, in terms of price segments. Bulk of Pakistan’s readymade garment exports has historically been in the “men’s or boys’ suits, jackets, trousers….” under HS Code 6203. The particular HS code has historically constituted for more than 80-85 percent of the readymade garment exports of Pakistan in the last five years.

Detailed HS code export data comes with a considerable lag, but looking at the 1QFY21 data, one can say that Pakistan may have moved towards the higher pricing end of 6203 HS code. Pakistan ranked 5th in 6203 exports in 2019 as per International Trade Centre data. The likes of China, Bangladesh, Vietnam, and Pakistan have had comparable unit prices within a 10 percent range. Others in the top 10 are the likes of Germany, Netherlands, Italy, where average unit price is at least double the Asian bloc, and quadruple in other cases.

Now, the export quantity has dwindled during the pandemic without an iota of doubt. That initially sounded like a dampener to Pakistan’s hope of textile exports, as Pakistan was heavily relying on the volume growth, in a highly price competitive market. But the last quarter (1QFY21) saw the average unit price in the readymade garment category rise 90 percent year-on-year, and higher by 50 percent over last eight quarters’ averages. This alone has kept the value in green despite a 45 percent year-on-year drop in the segment volume.

Pakistan’s average HS code 6203-unit price has hovered around $4.5 in the last two years – in line with major regional players. It has now jumped to nearly $7 per piece. It is hard to fathom Pakistan made a swift change from one HS code to another during the pandemic. What seems more plausible is that Pakistan has captured the higher end of the market, where demand may not have fallen at that great a pace.

Also, the producers in the higher end segment of the particular HS code are the ones most deeply impacted by the coronavirus, and industrial production has not returned to full throttle, unlike Pakistan’s. With Christmas approaching, Pakistan’s readymade exporters could get lucky, even as the pandemic shows no signs of going away, especially in the developed world.

Comments

Comments are closed for this article.