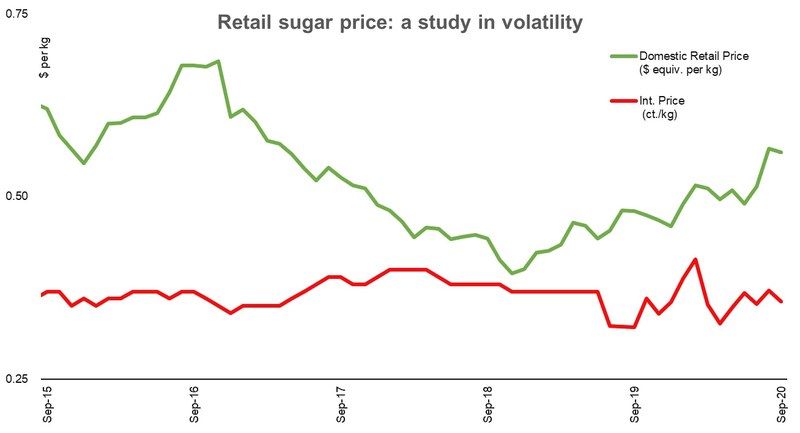

For better part of the last decade, international sugar prices as tracked by ISO White Sugar Index have been range bound between 32 – 42 cents per kg. During the same period, domestic retail prices have kissed the peak of Rs 95 per kg as well as witnessing precipitous declines to Rs 50 per kg multiple times. Although the domestic market is largely insulated from imports, prices have been equally mercurial in dollar terms: falling as low as 40 cents and rising as high as 70 cents per kg.

Domestic retail prices trade at a significant premium to ISO White Sugar Index – as they should. International prices are spot rates that do not reflect value chain costs such as handling and shipment, insurance, other incidental logistical expenses, importer, wholesaler’s and retailer’s margin, or sales tax on domestic consumption. Over the past 5 years, this premium has ranged between 1.06 – 1.96 over ISO index. Price volatility, thus, is a structural challenge inherent to domestic sugar market that hurts domestic consumers the most, possibly even more than the lack of competitiveness of domestic producers.

The consequences of this price volatility have been at full display since March 2020, when the federal government first indicated its intention to import sugar on account of low domestic production during the last crushing season. Pronouncements of various exemptions and quotas aimed to send price signals to the market have failed at both: to arrest the upward spiral in domestic sugar prices, or to pique private sector buyers’ interest in importing sugar, who have remained on the side lines due to unfriendly levels of price risk.

In this respect, federal government’s latest attempt to incentivize private sector import has left the domestic sugar producers up in arms. After the private sector sugar import quota remained unutilized, FBR announced exemption of imported sugar from income tax, sales tax, and VAT levies on August 24th for a period of two months. Recall that this step comes after the prohibitive custom duty on import of sugar of 40 percent was also waived earlier this year, to no avail – failing to translate into import. Will the latest exemptions have the desired effect?

Possibly. Regular readers will recall that the Customs valuation table values imported white crystalline sugar at $725 per ton under SRO 812(I)/2016, which has still not been revoked or suppressed; even though international price has been rangebound between $320 - $420 per ton over the past decade. Fortunately, the latest exemption from all tariffs and duties renders the $725 per ton valuation irrelevant, albeit temporarily. Logically, this should translate into utilization of imported sugar quota, especially since the shortfall in domestic availability has become nearly certain.

The million-dollar question, however, is whether this will help bring down sugar prices. Not by a lot. Recall that last month TCP’s tender to import sugar fell through when suppliers placed bids of $470 per ton -quoting a landed cost that was almost $100 higher than prevailing ISO White Sugar Index at the time. At that price, 20 percent additional margin (for wholesalers/retailers) would bring final price equivalent to prevailing retail price of Rs 95 per kg, keeping domestic producers margins intact. Why then is the domestic miller’s lobby unhappy?

That is not too hard to figure out. PSMA has demanded that the government remove sales tax of 17 percent imposed on domestically produced sugar to ensure a level playing field. That would knock off Rs 10 per kg from retail price, as domestic produced sugar is still valued at Rs 60 per kg for sales tax purposes. But doing that would erode margin on import, ensuring that the private sector traders refuse to participate in import – bringing everybody back to square one.

Tax exemptions on import may very well be the last trick in the bag of federal government, even though these exhibit unfair trading practices (temporarily!). If calculations by BR Research are correct, domestic stock of 1.8 million tons available as at July end (based on SBP pledge finance data) is barely sufficient to last through November. That means import quota of 0.3 million tons is just enough to last until the next crushing season begins in December. And while imports may not bring down retail sugar prices substantially, they will keep price of domestically produced sugar in check during the crucial next 10 weeks.

That is, if traders participate in import. Tick tock.

Comments

Comments are closed for this article.