Crescent Cotton Mills Limited (PSX: CCM) was established in 1959. Initially it operated as a sugar and distillery unit, however later it set up a spinning unit. It was previously known as Crescent Sugar Mills and Distillery Limited; it changed its name to the current one in 2012. Today, the company manufactures and sells yarn and hosiery items in addition to trading and dealing with cloth.

Shareholding pattern

Around 15 percent of the company’s shares are held under the category of ‘other companies’ which includes corporate bodies, trust, etc. this is closely followed by the directors, CEO, their spouses and minor children, holding another near 15 percent of the shares. The CEO, Mr. Muhammad Arshad holds close to 4 percent shares. The local general public collectively holds 55 percent, whereas the remaining around 15 percent shares are distributed with the rest of the category.

Historical operational performance

Crescent Cotton Mills profit margins have been on a declining trend before improving to some extent in FY18. However, in FY19 again it hit its lowest net margin seen in almost a decade.

The company recorded its highest decline in revenue during FY15, at 23 percent. While the overall textile sector saw a slump during the period, the spinning segment specifically saw the biggest decline within the sector. This was due to substantially low demand relative to previous years- particularly China; reason being that the country had shifted its demand to more price competitive suppliers. The company’s cost of production had increased to claim almost 95 percent of the revenue due to dollar depreciation, and shortage of energy which forced companies to move towards costly alternatives. Thus, the year concluded with a loss of Rs 21 million.

The declining trend in revenue continued during FY16 as it fell by 9 percent. While exports saw a decline in demand since most of the exports were limited to China, revenue from domestic sales also reduced due to a fall in yarn prices. However, cotton prices continued to rise, contrary to expectations, due to a shortfall of cotton as well as a poor crop. The spinning and weaving segment witnessed the most decline, whereas value-added segments fared relatively better. Cost of production further climbed on to consume more than 95 percent of the revenue; however, a major decline in profits was somewhat put off by other income coming from gain on remeasurement of fair value of investment properties, with net margin remaining flat at less than negative 1 percent.

In FY17, the company saw some recovery as revenue increased by 15 percent. This was primarily supported by domestic yarn sales. In fact, more than 90 percent of the revenue was generated through domestic yarn sales. The textile sector of Pakistan over the years has failed to modernize whereas poor cotton crop also added to costs. This is reflected in the consistent rise in cost of production. With the local cotton crop failing to meet demand of local manufacturers, the latter also must resort to expensive imported cotton. Without other income (Rs 170 million) the company would have witnessed another year of losses.

During FY18, topline nearly doubled to exceed Rs6 billion. This was again largely made up of domestic yarn sales. While a few industry experts claimed that the rationale for improvement in topline for some companies post FY18 was due to currency devaluation, this theory does not seem to hold true for Crescent Cotton Mills; exports, although increased year on year, had a negligible contribution to the total topline figure. However, there was a corresponding increase in cost of production as well, which did not deter from its above 95 percent of revenue level for the fourth consecutive year, thus allowing a minimal positive net profit. Until last year, other income was also notably contributing to the bottomline which returned to its normal level in FY18, thereby reducing net margin in comparison.

Topline increased for the third time in a row at 21 percent in FY19. Despite this, the company was unable to post a positive bottomline figure. Focused mainly on sale of yarn which did not have much of a market in the global arena, the company continued to sell in the domestic market. Apart from the slump in the Chinese market during FY15 and FY16, demand during the last two years remained subdued due to the US-China trade war. Cost of production was again at 96 percent of revenue primarily due to raw material expense. Given the shortfall in cotton in addition to poor crop, the manufacturers have had to import. With other income reducing even further, the company saw its lowest net margin.

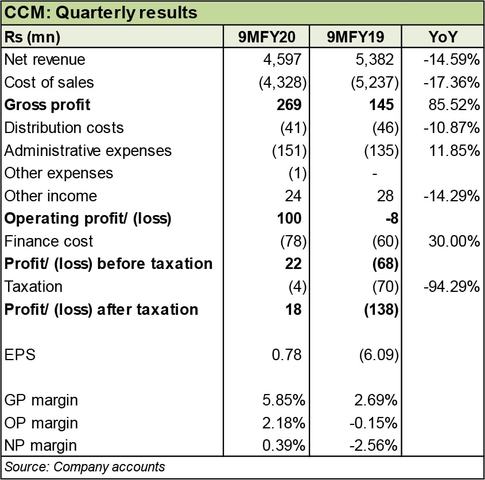

Quarterly results and outlook

Revenue fell during 9MFY20 by 14 percent year on year due to lower prices. A notable decrease was seen in the most recent quarter of 3QFY20. There was some improvement in cost of production as it reduced to 94 percent, although still high. This allowed some gain in profits. Since the company has been selling more in the domestic market, it could not take advantage of currency devaluation and hence favourable exports. However, the period ended with a profit of Rs 18 million.

While the event of the Covid-19 pandemic has spared one, it is imperative to consider the deterioration of the textile sector and the repercussions, irrespective of the pandemic, given that it employs a large part of labour and contributes the most to the GDP of the economy. Apart from lack of focus on value addition and improving technology, the country has also failed to diversify export markets.

Comments

Comments are closed.