The inter-ministerial Cotton Crop Assessment Committee (CCAC) under federal cabinet has released its second assessment of domestic cotton production for FY21 kharif season crop. Observers relying solely on governmental sources might conclude that realism is finally setting in on officialdom, as the original target of 10.9 million bales has been revised down to 7.7 million bales in the second round. Such optimism would be severely misplaced.

It is not that the official estimate of 7.7 million bales is misrepresentative of what is going on with the crop. Afterall, even at this level, the output would be at its lowest in 33 years. The problem, however, is that non-official sources estimate that the output may be lower by an additional 25 percent.

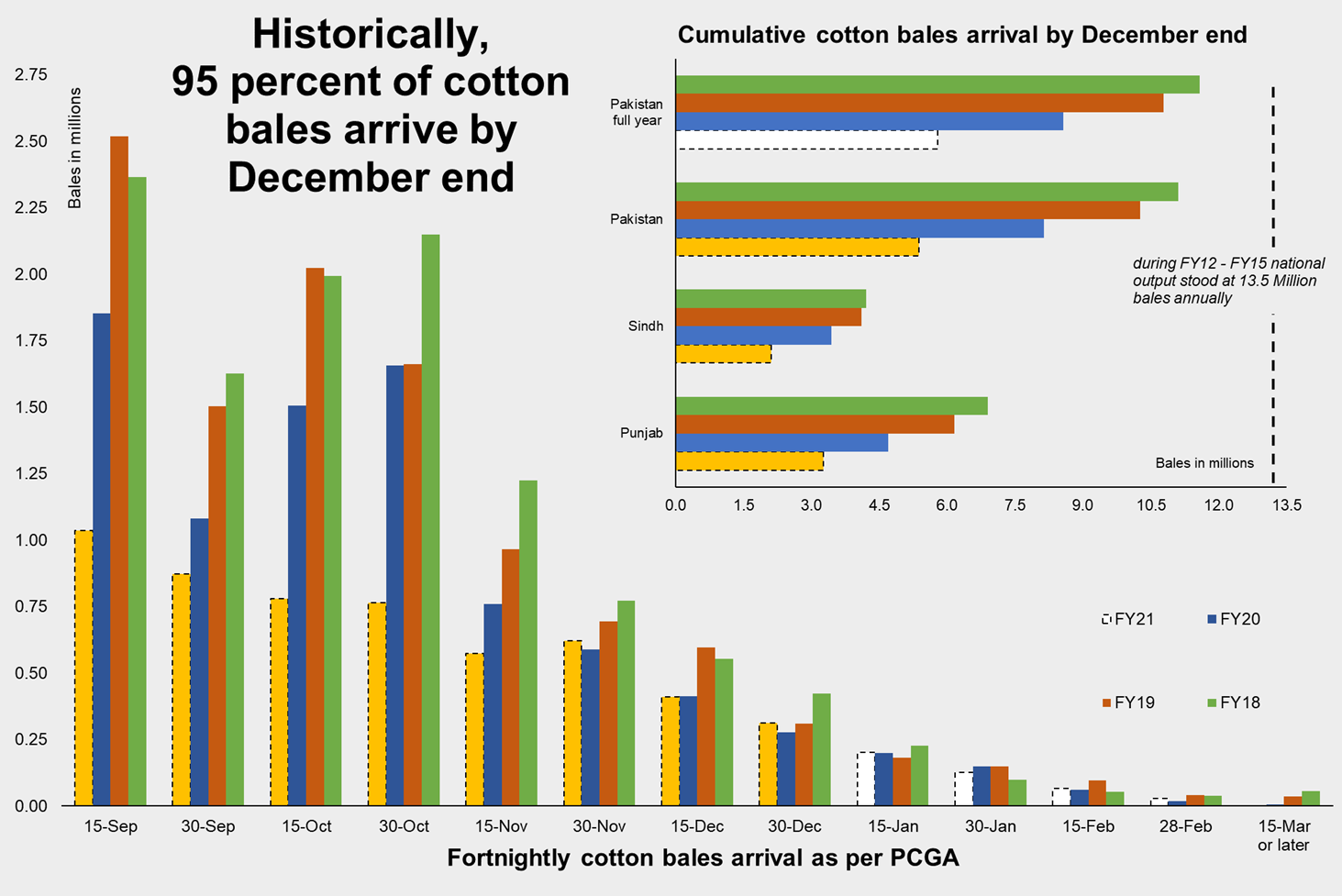

The fortnightly cotton crop arrival estimates – as issued by Pakistan Cotton Ginners Association (PCGA), and “collected with joint cooperation of All Pakistan Textile Mills Association (APTMA) and Karachi Cotton Association (KCA)” put cotton arrivals at 5.4 million bales by end of December 2020. That means crop arrivals are already short by over one-third compared to the same period last year (Aug – Dec). In contrast, the official estimate suggests that the crop will only be lower by 16 percent.

Why does the official estimate matter so much? After all, the government is in the business of routinely over- (or where necessary, under-) estimating facts, figures, and their impact. Private sector buyers make their decisions based on market intelligence, which drove price of domestic cotton up early into the harvest season based on forecast of severe shortfall. Most spinning mills appear to be already done with their buying spree as the sold to fresh stocks ratio (with ginneries) is also declining on a fortnightly basis, further corroborated by a slowdown in volume of monthly imports, as reported by PBS. In making commercial decisions, the market clearly does not wait for, or rely on official data.

But it matters. For two reasons, mostly normative in nature. First, based on whose figure you believe – the difference in output severely over or under-estimates the health of the cotton crop in this country. Consider: based on area sown of 2.2 million hectares, crop yield comes out at two very disparate figures of 445kg per ha or 590kg per ha, based on PCGA and CCAC figures, respectively.

If the private sector figure is to be believed, Pakistan’s average yield ranks 40th in 45 cotton growing countries that together produce 97 percent of global cotton output. And it also raises the question if given current levels of such poor productivity, whether domestic farmers should continue to grow cotton at all. Mind you, logic dictates that the decline in cotton acreage from peak 3.2 million ha to 2.2 million ha means that only the most productive growers would have stayed in the business – yet average productivity has nearly halved from peak of 815kg per ha, instead of improving.

Two, it shows how removed officialdom is from both reality and private sector stakeholders. The second assessment has been released after CCAC meeting on December 14th, 2020. Using trends based on past PCGA data – and private sector consultations – over 95 percent of seasonal cotton output is received at ginneries by end of December, historically. Consider also that CCAC estimates arrival of additional 2 million bales in coming weeks, even though PCGA’s fortnightly arrival report is readily available to them. What gives?

Unless of course, the officialdom believes that the stakeholders represented by PCGA are grossly under reporting their purchase and sales, possibly to hide profits – not unheard of in this land of pure. But then, consider this: the daily cotton report as released by Pakistan Central Cotton Committee (PCCC) – federal quarters for all-things-cotton under MNFS&R – lists CCAC’s assessment of 7.7 million bales and PCGA’s fortnightly figure of 5.3 million bales, side-by-side in the same breath and on the same page! If PCGA is misreporting, why does the official machinery watches on idly, as if oblivious?

Questions abound. By the time Economic Survey for FY21 is released in May 2021, official estimates will have been further revised down to match the reality of duties/taxes collected from cotton ginneries by revenue departments. Cotton ginning’s (standalone) contribution to GDP is probably less than fishery – another industry where the government does not even bother itself with collection of any volume/output data. Thus, whose interest is CCAC, PCCC, and MNFS&R really serving by insisting on estimates that are not simply wrong, but also undermine the credibility of these stakeholders?

The federal government need not disown CCAC’s assessment. However, the minister for NFS&R can take the first step in proving the seriousness of his intent & interest in agri- revival by justifying the accuracy (or lack thereof) of official figures. It may not offer any new insight to market players but may go a long way in building the minister’s credibility as a key stakeholder in cotton-related decision making.

Comments

Comments are closed for this article.