Another ‘mini budget’ is expected to be announced by the federal government this week, and stock brokers are going gaga over the possibility that the government would give various concessions to the market in terms of the capital gains tax regime and advance income tax on brokers. This, along with a couple of other sector-specific (mini) budgetary measures is predicted to “create positive sentiments”, which in turn will lift the market from its recent abyss. Is this prediction offered in hope or in expectation? There is only one way to find out: wait.

In the meanwhile, let’s take a step back and take a look at CY19 strategy reports recently released by various leading stock brokers. The predictions for December 2019 vary between 15 to 29 percent growth over CY18’s close depending on whose prediction one might want to buy.

But before one buys into those predictions, consider that brokers’ year-end predictions are hardly ever met at year end. Instead, the average year-end brokers’ outlook is usually met by way of almost-hitting the ‘during the year intra-day high’, before or after which the benchmark index also drops substantially below previous year’s close, and below what brokers had predicted on average.

Even in CY16 when brokerage reports sounded extremely optimistic on Pakistan, and market performance in fact exceeded that optimism - hitting the then high of 47,979 points - the benchmark index had hit a low that was 22 percent lower than average brokerage outlook for that year. And those were the good times with brokers’ CY16 reports citing inter alia “stable external sector”, “historic low inflation”, “FX reserves at all time high”, “possible reclassification to MSCI EM index”, “healthy politics”, “GDP growth crossing 5 percent”, and “high public sector development spending” (PSDP).

Compare that to what their CY19 reports are saying: “no reason to drop guard for now” with key sources of market volatility going to be cases against opposition leaders, coalition politics, and the IMF dilly-dally (brokerage: BMA). This is of course in addition to the factors of higher inflation, slow GDP growth, low PSDP, and increasing yields on the 10-year PIB.

According to calculations by AKD Securities, the current spread between equities’ earnings yield (14.9%) and sovereign yield (13.3%) is “too narrow to indicate bullish momentum, hinting at likely lacklustre market performance in the initial days to come. Echoing similar sentiments, brokerage Topline reminded that periods of high interest rates have historically kept the market at forward P/E below 7.5x. At current prices, that multiple is around 8x.

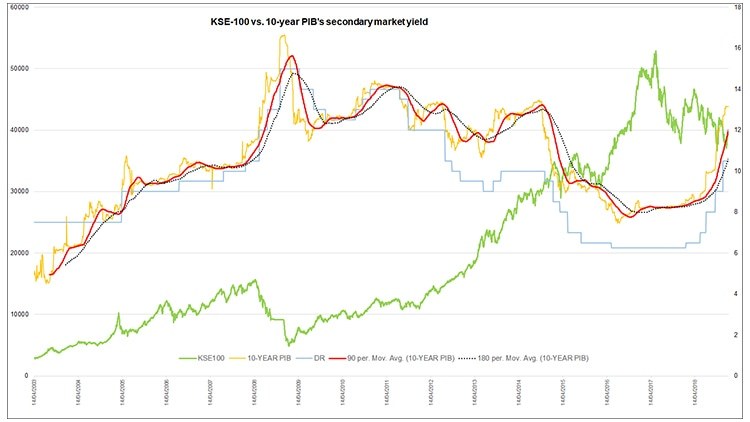

These views should not come as a surprise to BR Research readers. As early as late CY17, trends in secondary market PIB yields (10-year paper) had signaled a rise in interest rates, and BR Research’s then articles had cautioned how the rise in yields spells bane for equities and why investors “shouldn’t be surprised if the benchmark index slips to 36,000 points”. (Read KSE100: Drama on two-way street November 3, 2017; PSX’s year of fear November 30, 2017; RIP equities December 20, 2017)

This begs the question what’s the outlook on interest rates, the IMF programme and PIB yields. The consensus view among equities market players seems to be that the policy rate has peaked. But price action by bank treasurers is saying something else. Last week at the T-Bill auction the market had participated less than half of the maturing amount of Rs600 billion. The government took it all. But the key from that auction is that no one even participated in six- and twelve-months papers.

In other words, we are close to peak and not really peaked as yet, although there are expectations that the cycle may eventually start reverting by CY19 or the start of CY20. There is also a consensus that Pakistan will have to go to the IMF no matter how much the government might want to play it cool.

If the government does not go to the IMF, then it will give birth to a fresh bout of macroeconomic uncertainties, which the market will not like at all - unless those promised dollars from the UAE, China and Saudi Arabia do actually materialise. So far there is a huge gap between promises and actual dollar inflow.

In the event of any delay in the IMF programme, then according to AKD Securities’ assessment, the market could fall to as low as 33,800 points. That number is close to what BR Research wrote on October 15, 2018 when the article titled A game of nerves flagged that the PIB yields could “yield further wrath on equities to the extent that the benchmark index could even slide to 32,000-33,000 points”. If Pakistan does not go to the IMF, secondary market 10-year PIB yields are expected to rise from 13.15 at present to at least 13.6 – 13.75 percent. If Pakistan eventually goes to the IMF, then whether or not IMF insists on further increasing interest rates beyond 11 percent, it will surely insist on increasing the duration of debt. This means that in the ensuing PIB auctions the market will surely test the government’s appetite, and accordingly the secondary market bond yields may rise to 14.5 -14.7 percent.

In comparison if expected earnings yield of equities is only 15 percent then why would the smart money (high net worth individuals, pension or investment funds, and foreign players) invest in equities at current levels? Accordingly, the KSE-100 could substantially drop before it reaches the average outlook levels predicted in brokerage strategy reports.

Some chartist, however, point to the strong support of 38,900 levels calculated on the basis of 200-exponential moving average (EMA) on weekly charts, arguing that the market “should respect this level as the last time this level broke was in 2008.” Then again, as brokerage JS Global wrote in its CY19 strategy, “make no mistake that we are economically worse off now than during the previous two IMF entry points (2008 and 2013) and our external funding plague will continue to infect our monetary and fiscal policies in 2019”.

In other words, don’t be surprised if the market does not respect the 200-EMA (weekly charts) line and falls below 38,900 points to find new bottoms, just as it did not respect the 200-EMA back in 2008. In anticipation of market-specific capital gain tax (CGT) and advance income tax (AIT) concessions in the upcoming mini-budget, punters may jack up KSE-100 towards 41,800 points – an immediate term spike eyed by AKD’s chartist Qasim Anwar. But in the grand scheme of things the future doesn’t seem rosy. And heaven forbid – just heaven forbid - if budgetary announcements on CGT and AIT fall short of market expectations!

Comments

Comments are closed for this article.