The single largest polyester staple fibre (PSF) producer in Pakistan, Ibrahim Fibres Limited (PSX: IBFL) is a leading player in synthetic textiles. With over Rs 21.1 billion in market capitalisation, the firm stands out as the only synthetic textile manufacturer in the KSE100 list of companies.

The principal business of the company is the manufacture and sale of PSF and polyester yarn. It has two power generation plants with capacity of 73MW, solely for the purpose of catering to its energy requirements. Moreover, the company has control of Allied Bank, which often makes a healthy contribution to the company's financials.

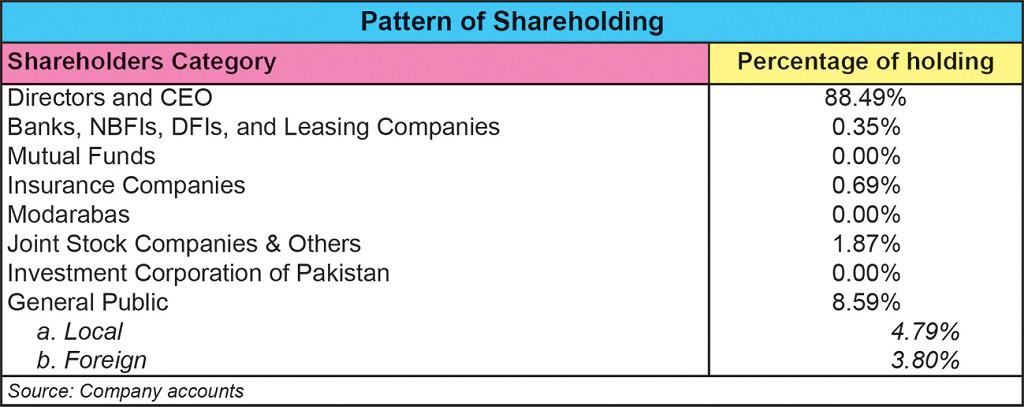

Stock and Pattern of shareholding

IBFL stock largely seems to be in the hands of the owners, with around 90 percent of the shares staying within the company. There appears to be no company or associate with any significant shareholding. Even the public amounts to less than nine percent, which would explain why IBFL makes rare appearances on the PSX and volumes, are so low.

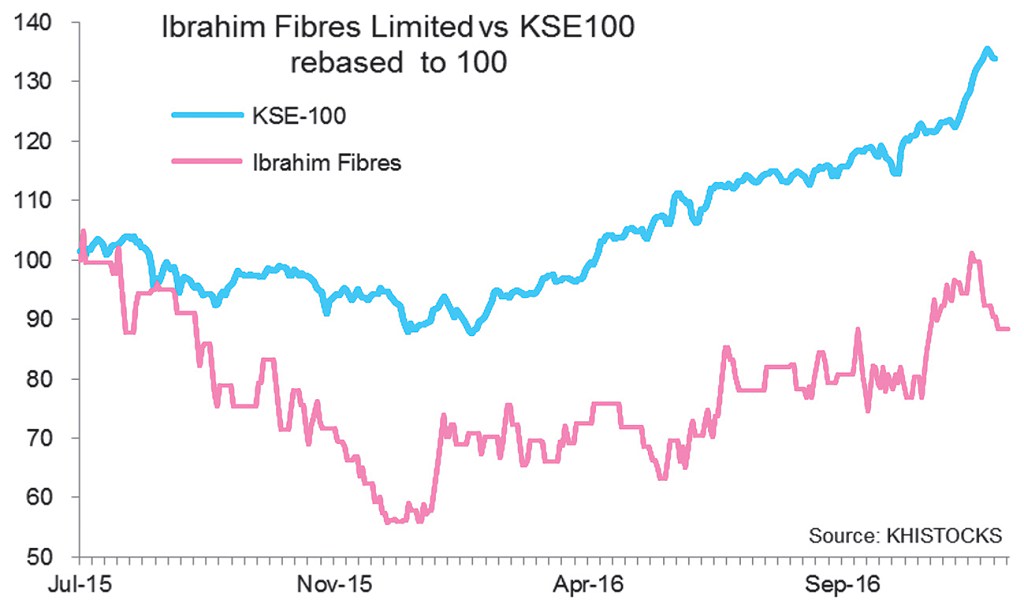

IBFL remained largely lacklustre throughout the past fiscal year, but the new fiscal has brought with it a slight uptrend. Nevertheless, the stock remains below the KSE100 index.

Prior Performance:

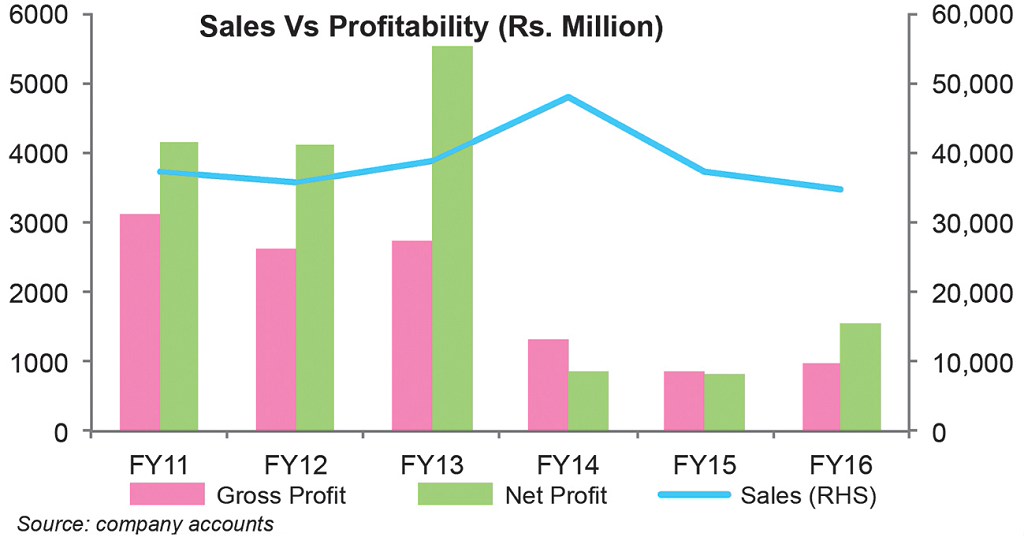

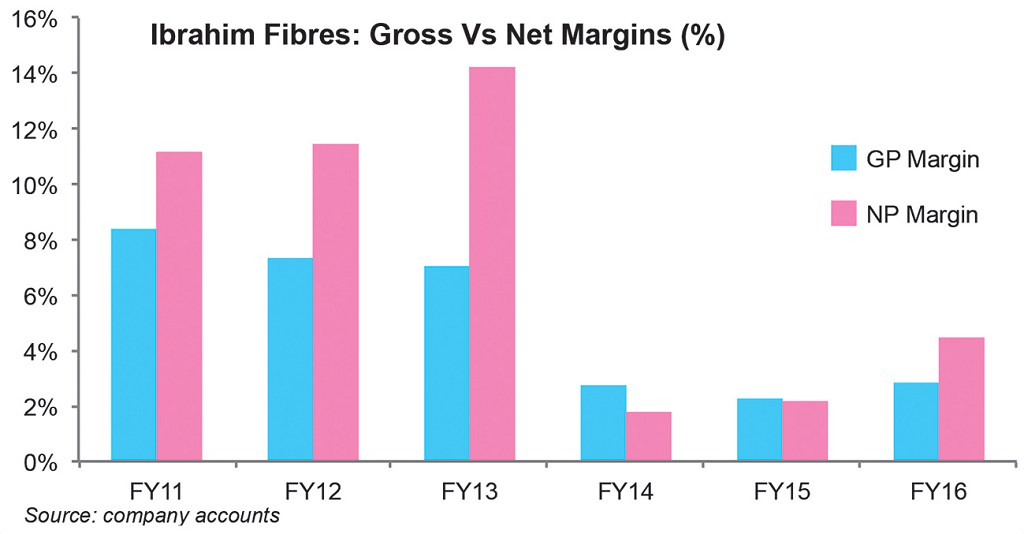

Ibrahim Fibres has fallen on hard times and has more or less stayed there; for the past three fiscal years, the company has seen a declining trend in sales, while profits are a fraction of what they were in the years before that. In fact, were it not for Allied Bank, Ibrahim Fibres would have been reporting net losses for all three years (FY14-16).

Things clearly went wrong for the company in FY14 - ironically, the year that it achieved its highest-ever sales. As per the Director's Report of that year, FY14 witnessed a depression in demand and prices of PSF. This happened after the National Tariff Commission decided to withdraw an anti-dumping duty on imports of PSF from China. The decision was taken at the start of the fiscal year and the subsequent years have seen heavy PSF dumping by Chinese companies in local market at exceptionally low prices. As per one of the Director's Reports, local PSF manufacturers had been forced to adjust PSF sales price downwards in order to remain competitive.

To make matters worse, Ibrahim Fibres does not have an export market; the company's exports amount to a negligible 0.03 percent of sales (as of FY16). With heavy PSF dumping and nowhere to go, the company has been taking a beating in its only market.

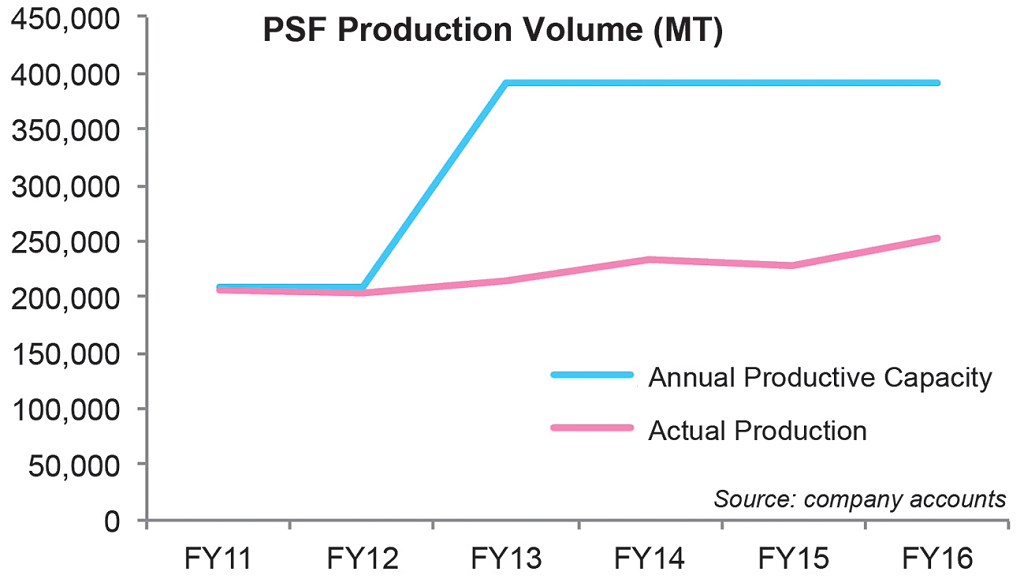

However, Ibrahim Fibres has managed to maintain volume growth in Pakistan. The NTC re-imposed an anti-dumping duty on PSF imports from October 2015 onwards. The graph indicates that the company's PSF volumes have been higher in FY16. The company has also ampede up production in the recent year.

Another issue, then, has been lower feedstock prices. PSF is made from the raw materials PTA (Purified Terephthalic Acid) and MEF (Mono-Ethylene Glycol). The prices of these feedstock materials were on a decline throughout FY14, then entirely plummeted vis-à-vis oil at the start of FY15. Thus, the recent reduction in revenues and gross margins was primarily caused by "declining PSF prices due to decrease in feedstock prices," claims the Director's Report. Why the PSF prices declined in greater proportion to the feedstock prices is anyone's guess.

Recent Performance:

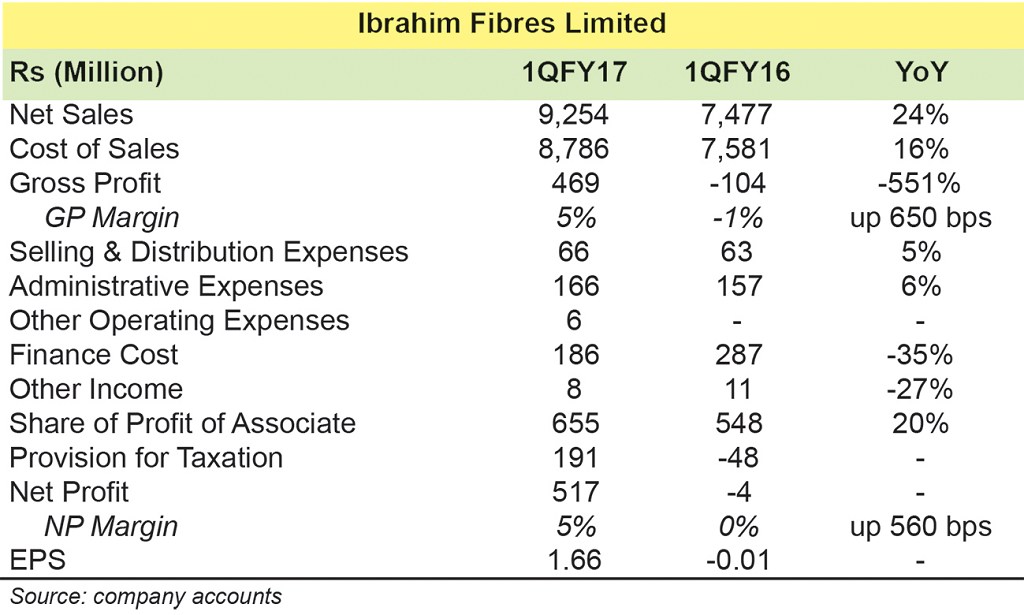

Ibrahim Fibres appears to be back in the game. For the first quarter ended FY17, the polyester maker's sales jumped by 24 percent year-on-year, while costs did not increase proportionately. This gave Ibrahim Fibres a gross profit of Rs 469 million as against a loss of Rs 104 million in the same period last year.

In addition, Allied Bank's performance seems to have been better as well; the share of profit of Ibrahim Fibre's associate company was up by 20 percent year-on-year.

As per the Director's Report, PSF production was up by a whopping 42 percent year-on-year. The company undertook numerous BMR measures and made investments into its polyester and textile plants. Moreover, as mentioned earlier, the duty on PSF imports has helped the company regain some momentum in recent times. It may also be the case that lower cotton production during the year meant that the demand for polyester was higher over the period.

Outlook:

Being such a huge producer of PSF and catering to Pakistan only, Ibrahim Fibres' wellbeing depends largely on the state of the textile industry. Some new measures such as restoration of zero-rating on exports and a steadier supply of energy have been witnessed, but the industry is far from out of the woods yet.

Comments

Comments are closed for this article.