More than a decade after the 2003-04 deregulation of Pakistan's telecom sector, Pakistan Telecommunication Company Limited (PSX: PTC) - a long-time state monopoly that is now run by private management - continues to be the largest telecom carrier in Pakistan. PTC, as PTCL Group, operates in different telephony segments, having telecom licenses for fixed local loop (FLL - landlines), wireless local loop (WLL) telephony, mobile telephony (Ufone), long distance & international (LDI) telephony, broadband services, and mobile financial services or branchless banking.

PTC - which is chiefly made up of fixed-line behemoth PTCL Company and its cellular arm, Ufone - was partially privatised in 2007, when PTC's 26 percent management stake was acquired by Emirates Telecommunication Corporation (Etisalat) for a sum of $2.6 billion. About $800 million of that amount still remains outstanding on account of a dispute over transfer of real estate in PTCL Company's name.

Since 2007, when the forces of fixed-mobile substitution favoured mobile over landlines, PTC has been consciously shifting its strategic focus towards data services. Today, PTC enjoys multiple revenue streams, thanks to the data and voice operations of PTCL Company and Ufone. Besides retail services that it itself markets in segments of FLL, WLL and broadband, the PTCL Company is a carriers' carrier, in that it also provides core infrastructure services to other telecom operators, internet service providers, call centres, and payphone operators.

Recent financial performance

The PTC management in 2013 changed the company's financial/accounting year to start in January instead of July. For meaningful comparison, the financial performance of the three full calendar years since has been taken into account here.

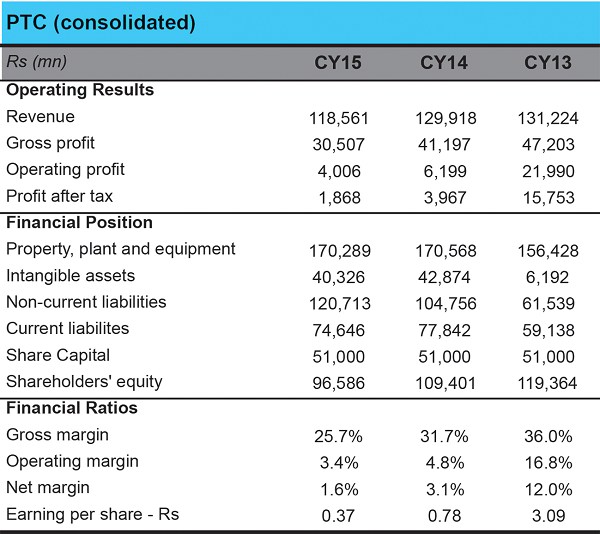

PTC's profitability has seen a visible decline over the past three calendar years. Group profits in CY15 were just 12 percent of what they were back in CY13. The decline between CY13 and CY15 is mainly on account of a trend of declining revenues and a greater depletion of those revenues on core costs and operating expenditures. In the most recent full calendar year, CY15, PTC's top line declined by 9 percent, operating profit declined by 35 percent, and net profit fell by 53 percent.

To break it down, weaknesses resulting from both PTCL Company and Ufone have contributed to the lacklustre financial performance in recent years. PTCL Company's CY15 revenues dropped by 7 percent year-on-year, mainly on account of lower revenues from its LDI operations, which have seen an industry-wide squeeze in the post-ICH days. Ufone revenues slumped by over 10 percent in CY15, plausibly due to lost revenues on account of Sims re-verification drive of 2014 and declining voice tariffs.

The PTCL Company performed well in CY15 relative to previous year, growing its operating and net profits solidly. But its CY15 net profitability (Rs 8.8 billion) was 70 percent of what it was back in CY13.

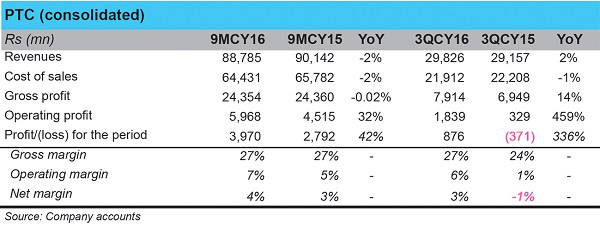

Ufone, on the other hand, suffered a net loss of over Rs 6.5 billion in CY15, marking a consecutive loss-making year, compared to Rs 3 billion in profits that it had scored in CY13. In the nine months ended September 30, 2016, one sees a sharp difference in PTC's operating performance. As the illustration shows, PTC (the Group) was able to boost its bottom line massively in 9MCY16, with a corresponding amelioration in profit margins.

Breaking it down, one notices that there is a slight reversal of fate among the constituent units. It is Ufone that grew its revenues and curtailed its losses in 9MCY16, and it was PTCL Company that saw declines in its top line and bottom line during that period. In 3QCY16, however, one sees all round positivity, where despite a slight fall in revenues, PTCL Company expanded its bottom line - thanks to cost control measures - and Ufone also cut its losses, which was made possible on the back of a double-digit growth in its revenues.

Future outlook

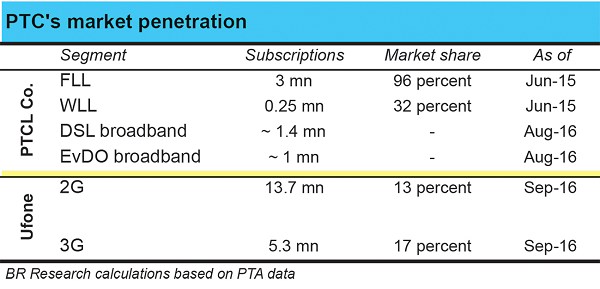

If it weren't for slowdown in LDI revenues, PTC as a group would have posted better financials in recent years. With the LDI segment likely to be a source of little to no revenue growth - thanks to low call termination tariffs and substitution happening on account of OTT apps such as WhatsApp and Skype - PTCL Company might continue to increasingly depend on its retail broadband operations and wholesale infrastructure for revenue growth. In recent periods, the lack of growth in PTCL's fixed broadband (DSL) and wireless broadband subscriptions, however, is not conducive to that objective.

That Ufone has returned to posting revenue growth is a sign that the mobile broadband market is in a better shape in terms of magnetisation. As of 9MCY16, Ufone was still in a state of net loss - as per our calculations, it scored a net loss in excess of Rs 1 billion. But this year, Ufone's extent of losses has been significantly curbed due to a rejuvenated top line. Ufone is expected to gain more breathing space and lend a hand to group financials if the main player, PTCL Company, continues to struggle to grow its top line in near future.

Comments

Comments are closed for this article.