Towellers Limited (PSX: TOWL) was incorporated in Pakistan as a private limited company in 1973 and was converted into a public limited company in 1994. The company is engaged in the manufacturing and export of garments, towels and textile make ups.

Pattern of Shareholding

As of June 30, 2025, TOWL has a total of 17 million shares outstanding which are held by 1421 shareholders. Around 84.11 percent of the company’s shares are held by its Directors, CEO and sponsors followed by local general public holding 8.17 percent shares of TOWL.

Insurance companies account for 3.86 percent shares of TOWL while public sector companies hold 2.103 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-25)

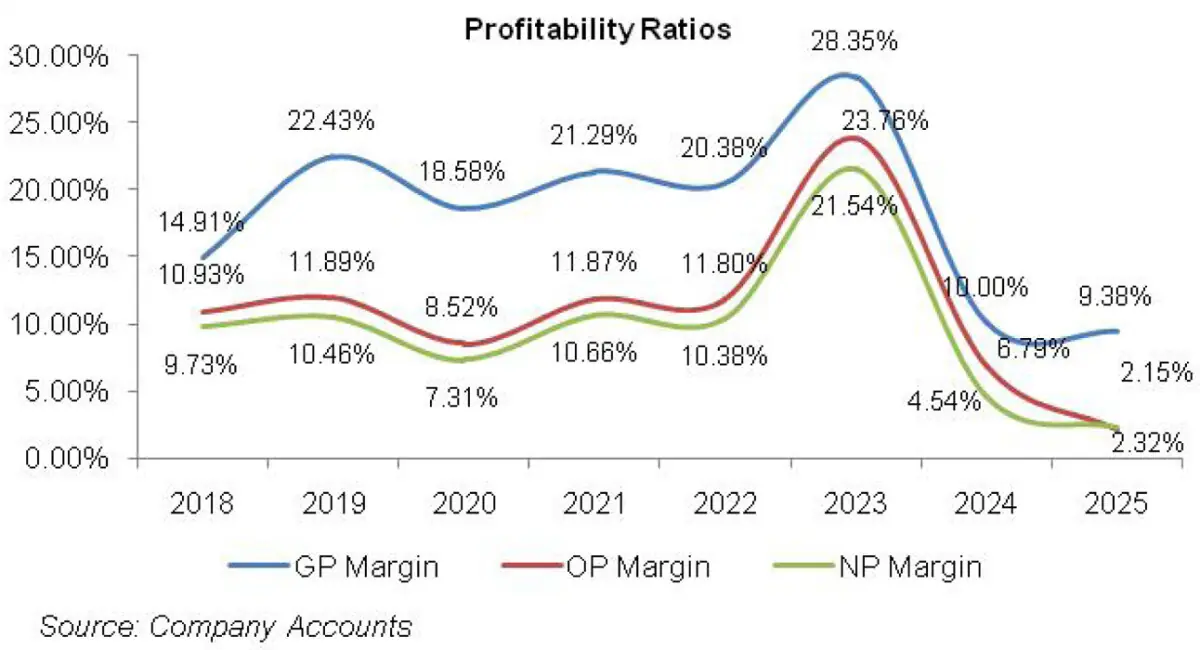

Except for a slide in 2020, TOWL’s topline posted year-on-year growth over the period under consideration. Conversely, its bottomline shrank in 2020, 2024 and 2025. The margins posted sound growth in 2019 followed by a plunge in 2020. In 2021, the margins greatly recovered followed by a marginal downtick in 2022.

In 2023, TOWL’s margins registered whopping growth to reach their optimum level followed by a drastic fall in the subsequent years to reach their lowest level in 2025 (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, TOWL’s topline boasted a staggering growth of 47.68 percent year-on-year to clock in at Rs.3848.284 million. Since TOWL is an export oriented business with local sales constituting less than 1 percent of its net sales, Pak Rupee depreciation and government rebates for exporters proved to be bliss for the company and greatly improved its gross margin.

During 2019, cost of sales grew by 34.64 percent year-on-year on account of high indigenous inflation which drove up the prices of raw materials as well as fabric dyeing and stitching charges.

However, TOWL’s gross profit improved by 122.10 percent year-on-year with GP margin tremendously growing from 14.91 percent in 2018 to 22.43 percent in 2019.

Distribution expense rose by 31.33 percent year-on-year in 2019 on account of higher export freight charges, export surcharge, clearing and forwarding as well as travelling charges.

Administrative expense also grew by 9.44 percent year-on-year in 2019 mainly on account of higher payroll expense as the company increased its human resource count from 794 employees in 2018 to 1012 in 2019 in order to meet additional demand. Other expense rose by 59.41 percent year-on-year in 2019 due to higher provisioning for WPPF.

On the contrary, other income plunged by 96.40 percent year-on-year in 2019 due to high-base effect as the company received waiver of loan and markup in 2018 which wasn’t there in 2019.

Operating profit grew by 60.65 percent in 2019 with OP margin picking up from 10.93 percent in 2018 to 11.89 percent in 2019. Finance cost inched up by 24.64 percent year-on-year in 2019, however, it mainly comprised of interest charges on WPPF and bank charges as TOWL didn’t have any external borrowings in 2019.

Net profit grew by 58.78 percent year-on-year in 2019 to clock in at Rs.402.68 million with NP margin standing at 10.46 percent up from NP margin of 9.73 percent recorded in 2018. EPS also rose from Rs.14.92 in 2018 to Rs.23.69 in 2019.

TOWL’s topline posted year-on-year drop of 1.98 percent in 2020 to clock in at Rs. 3772.25 million. This was because the company faced delays and cancellation of export orders due to restrictions on the movement of people and goods on account of COVID-19. Furthermore, TOWL also suffered production losses and idle capacity due to lockdown which increased its fixed cost.

The topline drop would have been more profound had the local currency not depreciated. Weaker Pak Rupee diluted the effect of a massive drop in volumes and kept the net sales afloat to a great extent. Cost of sales grew by 2.89 percent year-on-year in 2020 which reduced the gross profit by 18.79 percent year-on-year. GP margin slid down to 18.58 percent in 2020.

As sales volume nosedived, so did the distribution expense because of lower freight, clearing and forwarding and travelling charges coupled with lesser export development surcharge. Administrative expense mounted by 17.67 percent year-on-year in 2020 primarily due to higher payroll expense due to rising inflation. Lesser provisioning for WPPF drove other expense down by 27.21 percent year-on-year in 2020; however, other income staggeringly grew by 298.56 percent due to remarkable profit recognized on saving account.

Operating profit tapered off by 29.78 percent year-on-year in 2020 with OP margin dropping to 8.52 percent. Finance cost contracted by 1.46 percent year-on-year in 2020 due to lesser bank charges. Net income plummeted by 31.49 percent year-on-year in 2020 with NP margin inching down to 7.31 percent. EPS also fell to Rs. 16.23 in 2020.

The company came back even stronger in 2021 with 38.40 percent year-on-year surge in its topline which clocked in at Rs.5220.747 million. As the signs of COVID-19 began to ease down, the retail markets of the US and Europe resumed and TOWL received huge sales orders. Local sales also grew by over 6 times in 2021. Due to the installation of solar power plant as well as new knitting and dyeing machines, the company was able to keep a check on its cost of sales which grew by 33.79 percent year-on-year in 2021.

Gross profit improved by 58.59 percent year-on-year in 2021 with GP margin climbing up to 21.29 percent. Distribution and administrative expense mounted by 25.63 percent and 20.10 percent respectively in 2021 due to increase in operational capacity and better sales volumes.

The number of employees also grew from 1014 in 2020 to 1195 in 2021. Higher provisioning for WPPF pushed other expense up by 82.79 percent year-on-year in 2021 while other income shrank by 26 percent during the year due to lesser profit on saving account as discount rate greatly reduced during the year.

Operating profit posted a robust 92.86 percent year-on-year rise in 2021 with OP margin bouncing back to 11.87 percent – the level seen in 2019. Finance cost dropped by 14.78 percent year-on-year in 2021 due to lower interest charges on WPPF. Net profit grew by 101.69 percent year-on-year in 2021 to clock in at Rs.556.456 million with NP margin clocking in at 10.66 percent. EPS jumped up to Rs.32.73 in 2021.

2022 brought about the highest year-on-year growth of 96.10 percent in TOWL’s topline which was recorded at Rs.10,238.086 million. This was due to rise in sales orders coupled with the impact of Pak Rupee depreciation.

However, elevated level of inflation drove the cost of sales up by 98.36 percent year-on-year in 2022. This trimmed the GP margin down to 20.38 percent. Increase in sales volume coupled with higher ocean freight charges pushed the distribution expense by 158.52 percent year-on-year in 2022.

Administrative expense also ticked up by 16.71 percent year-on-year in 2022 due to higher payroll expense coupled with higher allowance for expected credit losses. Other expense grew by 124.78 percent year-on-year in 2022 due to higher provisioning for WPPF.

Other income also posted a handsome growth of 67.50 percent year-on-year in 2022 mainly due to higher profit on saving account. Operating profit multiplied by 95 percent year-on-year in 2022 with OP margin staying almost afloat at the last year level of 11.80 percent.

Finance cost grew by a massive 327 percent year-on-year in 2022 as the company obtained long-term financing under SBP finance scheme for renewable energy and short-term borrowings under export finance scheme. Net profit rose by 91 percent year-on-year in 2022 to clock in at Rs.1063.048 million with NP margin of 10.38 percent. EPS ascended to Rs.62.53 in 2022.

Global recession led to a reduction in export orders during 2023; however, unprecedented level of exchange gain guarded TOWL’s topline which posted 8.29 percent year-on-year rise to clock in at Rs. 11,086.916 million in 2023. Local sales did quite well in 2023, however, still stood at 1 percent of the net sales of TOWL in 2023 versus its share of 0.14 percent in TOWL’s net sales mix in 2022.

Lesser orders resulted in low capacity utilization and low production which trimmed down cost of sales by 2.54 percent year-on-year in 2023. This translated into 50.58 percent year-on-year growth in gross profit with GP margin rising to its highest level of 28.35 percent in 2023.

Distribution expense plunged by 41.76 percent in 2023 due to curtailed sales volume which pushed down export freight and export development surcharge. Administrative expense surged by 9.64 percent year-on-year due to high inflation which drove up payroll expense in 2023 while headcount was reduced from 1892 employees in 2022 to 1736 employees in 2023. Other expense grew by 114.18 percent year-on-year in 2023 on account of higher provisioning for WPPF.

Other expense was counterbalanced by a tremendous 696.87 percent year-on-year rise in other income in 2023 which was the result of hefty profit earned on saving accounts and mutual funds investment.

Operating profit grew by 118 percent year-on-year in 2023 with OP margin soaring to 23.76 percent. Finance cost escalated by 131.61 percent year-on-year in 2023 on the back of higher discount rate while borrowings greatly reduced during the year. Lesser borrowings are evident from TOWL’s gearing ratio dropping from 12.95 percent in 2022 to 0.14 percent in 2023.

Net profit surged by 124.67 percent in 2023 to clock in at Rs.2388.337 million with EPS of Rs.140.49 and NP margin of 21.54 percent.

In 2024, TOWL’s topline progressed by 11 percent year-on-year to clock in at Rs.12,314.921 million. During the year, stability was seen in the exchange parity. Stronger rupee as well as elevated input cost including gas and electricity prices resulted in a shrunken GP margin of 10 percent in 2024.

he company also had to revise its prices downward in 2024 due to intense competition and lackluster demand in the international market. Distribution expense surged by 15.81 percent due to higher export freight, export development surcharge as well as clearing & forwarding charges incurred during the year. Administrative expense inched up by 9.10 percent in 2024.

While payroll expense slid in 2024, factors that pushed up the administrative expense were elevated directors’ remuneration, depreciation expense as well as fee & subscription charges. Other expense dwindled by 40.56 percent in 2024 on the back of lower profit related provisioning.

Conversely, other income improved by 35 percent in 2024 on account of improved profitability on saving accounts and investments. Operating profit fell by 68.25 percent in 2024 with OP margin shrinking to 6.79 percent. Finance cost slid by 42.24 percent in 2024 due to lower interest expense incurred on short-term borrowings. Introduction of slabs for super tax also proved to detrimental for the company and resulted in 28.10 percent surge in the tax expense during 2024.

Net profit plummeted by 76.57 percent to clock in at Rs.559.501 million in 2024. This translated into EPS of Rs.32.91 and NP margin of 4.54 percent in 2024.

In 2025, TOWL posted a marginal year-on-year growth of 0.26 percent in its topline which clocked in at Rs.12,347.002 million. This was due to reduced prices, intense competition and stronger local currency which coupled with elevated energy tariff and inflationary pressure led to the lowest GP margin of 9.38 percent in 2025.

Increased fixed cost due to capacity enhancements of-late also pushed down TOWL’s gross margin in 2025 with its gross profit declining by 6 percent during the year. TOWL’s sales are greatly concentrated in the US and European markets. In 2025, these regions faced trade tensions, reciprocal tariff imposition and weaker consumer demand which greatly affected the sale of textile products. Distribution expense escalated by 44.41 percent in 2025 due to higher export freight charges, clearing & forwarding charges as well as travelling expense incurred during the year.

Administrative expense also mounted by 21.66 percent in 2025 due to higher payroll expense which was the result of inflationary pressure as well as workforce expansion from 2083 employees in 2024 to 2353 employees in 2025. Lower provisioning done for WWF, WPPF, lesser donations and no un-realized exchange loss on foreign currency transactions resulted in 63.68 percent decline in other expense in 2024.

Other income also deteriorated by 71.28 percent in 2025 particularly on the back of lesser income from short-term investments and saving accounts. TOWL posted 68.25 percent diminution in its operating profit in 2025 with OP margin clocking in at 2.15 percent.

Finance cost ticked down by 4.70 percent in 2025 due to monetary easing while borrowings escalated during the year resulting in a gearing ratio of 8.48 percent in 2025 versus 3.18 percent in the previous year. Net profit dwindled by 48.67 percent to clock in at Rs.286.709 million in 2025. This culminated into EPS of Rs.16.87 and NP margin of 2.32 percent in 2025.

Recent Performance (9MFY26)

During the nine-month period of the ongoing fiscal year, TOWL recorded 17.49 percent year-on-year decline in its net sales which clocked in at Rs.8067.30 million. This was on the back of lower demand in the key export markets of TOWL as well as pricing pressure due to higher energy cost, tariff barriers and tougher competition.

Despite lower sales, the company’s focus on high margin products alongside operational efficiency resulted in 3.46 percent uptick recorded in its gross profit in 9MFY26 with GP margin clocking in at 12.39 percent versus GP margin of 9.88 percent recorded in 9MFY25. Distribution expense tumbled by 7.65 percent in 9MFY26 due to thinner export sales.

Conversely, administrative expense spiked by 20.23 percent in 9MFY26 due to inflationary pressure which pushed up the payroll expense. Lower provisioning done for WWF and WPPF appears to be the cause of 65.23 percent decline in other expense in 9MFY26. Other income also deteriorated by 44.27 percent in 9MFY26 due to lower interest income on the back of monetary easing.

The company recorded 10.26 percent decline in its operating profit in 9MFY26 with OP margin clocking in at 3.64 percent versus OP margin of 3.34 percent recorded in 9MFY25. Despite monetary easing, finance cost surged by 35.86 percent in 9MFY26 due to increased borrowings.

TOWL’s net profit clocked in at Rs.120.96 million in 9MFY26, down 55.37 percent year-on-year. This translated into EPS of Rs.7.12 and NP margin of 1.50 percent in 9MFY26 versus EPS of 11.85 and NP margin of 2.77 percent registered in 9MFY25.

Future Outlook

TOWL’s heavy reliance on the US and European market exposes it to adverse shifts in demand patterns which will dictate its financial performance in the short-run. However, the company plans to expand its product portfolio and geographical outreach to garner greater export orders.

Increased emphasis on high margin products and keeping a check on its overheads and enhancing operational efficiency will buttress the financial performance of TOWL in the coming year.

Comments