Legacy energy liabilities must be separated from current consumption tariffs if Pakistan wants affordable power, industrial competitiveness, and a real market.

Pakistan’s energy problem is no longer just about supply. It is about the accumulated cost of years of bad policy, weak governance, distorted pricing, and delayed reform. That overhang now sits like a dead weight on the entire system.

The state keeps trying to recover yesterday’s mistakes through today’s tariffs (without any concrete reform or restructuring of the system) and then acts surprised when industry cannot compete, households cannot pay, demand collapses, and reform goes nowhere.

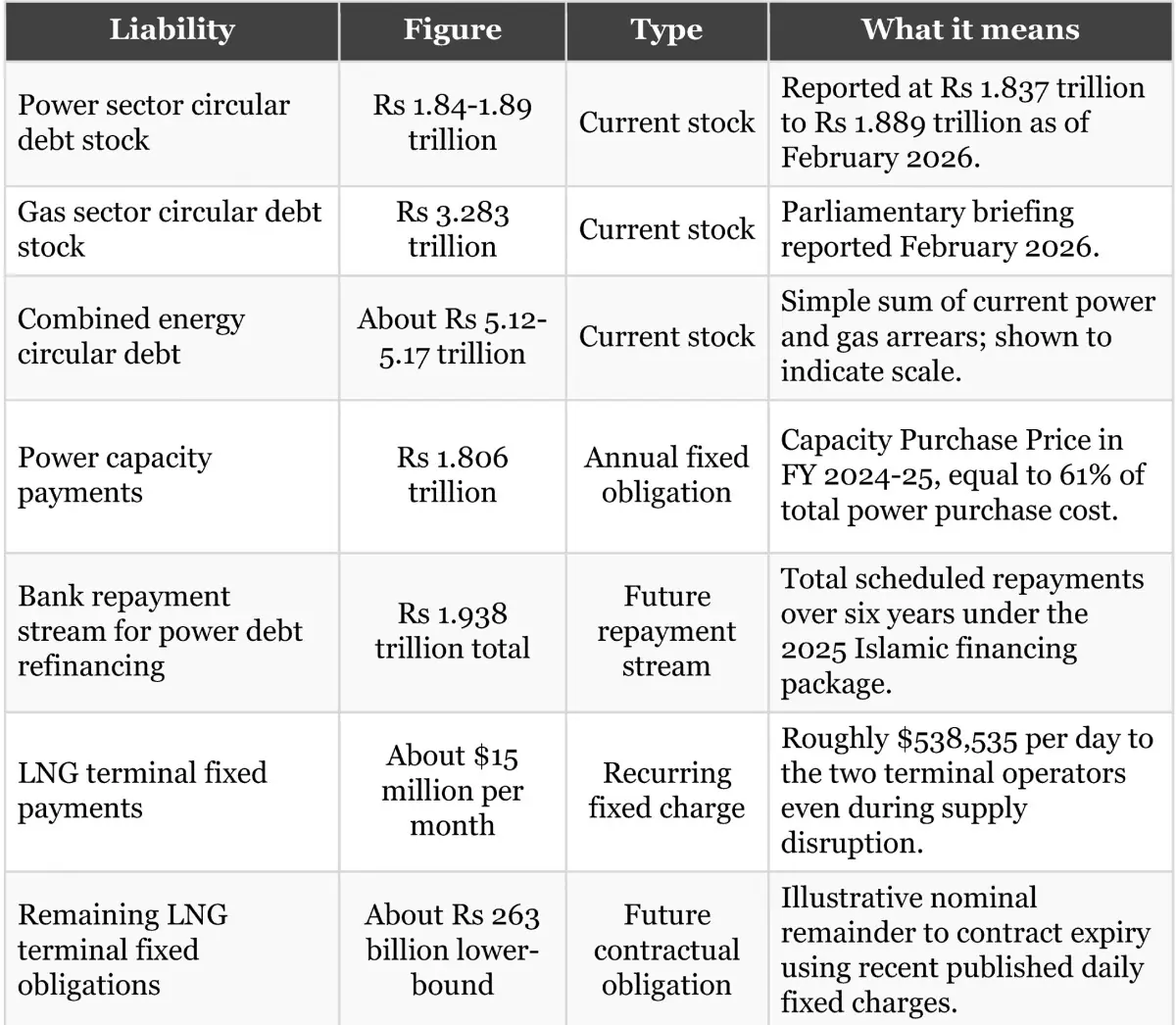

The numbers are ugly enough on their own. The stock of circular debt in the power and gas sectors together is already above five trillion rupees on current estimates. On top of that sit annual capacity payments, LNG terminal fixed charges, and repayment streams created to refinance old arrears. These costs are real. But loading them onto current consumption is the policy equivalent of making today’s economy pay rent on yesterday’s incompetence.

Scale of the energy overhang

Note: the table separates current debt stock from future fixed obligations and repayment streams. These figures show scale; they are not all additive one-for-one, and some future flows reflect refinancing of liabilities already in the stock.

Surprisingly there is no serious analysis or plan to stop this haemorrhaging of the energy sector. Instead, the strategy seems to be to pass on the losses to the consumers. There seems too little realization on how inefficient this strategy is in terms of possibilities of demand substitution options and the adverse growth and investment options.

Instead of separating legacy liabilities from the price of serving current load, the system bundles past inefficiency, fixed contractual burdens, theft, non-recovery, and political pricing into the tariff facing current users. The result is a tariff structure that has become unaffordable for much of the population and commercially destructive for productive sectors, especially industry and exports.

This is self-defeating policy. When tariffs rise beyond what consumers can bear, recoveries worsen, demand falls, captive generation expands, rooftop solar accelerates, and more users try to defect from the grid. The remaining paying consumers are then asked to carry an even larger burden. That is how a pricing system enters a death spiral while pretending to be fiscally responsible.

Industry bears the brunt first. Manufacturers cannot absorb tariffs inflated by legacy costs that have little to do with the marginal cost of power today. When electricity prices are pushed up to finance stranded payments and circular debt, Pakistani industry loses competitiveness against regional peers. Exports weaken, investment slows, factories reduce utilization, and the tax base shrinks. In trying to collect more from current users, the state ends up shrinking the very economic activity needed to sustain the system.

The social consequences are just as damaging. For the bulk of the population, especially lower- and middle-income households, electricity, and gas are no longer just utility issues. They are now central inflation issues. High tariffs cascade through transport, food, services, and domestic budgets. When the state uses utility bills as a hidden tax instrument to recover years of energy-sector failure, it does so in one of the most regressive ways possible.

Worse, this approach is now blocking the development of an energy market. You cannot build workable energy markets if every new transaction is forced to carry the baggage of the old system. You cannot create credible privatization if investors know that the wires business is stuffed with non-commercial obligations, political interference, and tariffs inflated by liabilities they did not create. And you certainly cannot expect competitive supply, open access, wheeling, or bilateral contracting to emerge if the price signal itself is contaminated by legacy costs.

That is why the first principle of reform should be straightforward: legacy debt and current energy pricing must be separated.

This does not mean the liabilities disappear. It means they are put where they belong: into a financing and fiscal strategy instead of the marginal tariff.

Circular debt stocks should be refinanced over longer horizons through explicit instruments. Legacy contractual obligations should be renegotiated, reprofiled, bought down, or budgeted transparently where possible.

Revenue from privatization, petroleum levies, carbon-related taxes, and targeted budgetary transfers can all be part of the solution. Above all, deregulation and other structural measures to revive growth should be undertaken to foster a strong demand for energy to finance the legacy debt.

The second principle is equally important: stop adding to the pile. Pakistan cannot refinance old liabilities while continuing to recreate them every year. That requires discipline in dispatch, pricing, recovery, and governance. Cheaper power must be dispatched first.

Transmission must be strengthened urgently so that low-cost electricity from where it is generated can actually reach where it is needed. Recoveries must improve. Losses must be reduced. Fuel allocation must stop favouring expensive options merely because the system is rigid or politically convenient.

Transmission deserves special emphasis because it is one of the main reasons cheaper sources are not dispatched properly. Wind, local coal, imported coal, hydel, and other lower-cost sources are often available, yet they remain underutilized because the system cannot move power efficiently across regions. The result is absurd: Pakistan pays for expensive generation while cheaper capacity sits stranded. Strengthening transmission is therefore not a technical side issue. It is central to cost reduction, tariff reform, and the viability of future markets.

Third, the distribution business must be made commercial. No tariff rationalization will work if distribution companies continue to leak value through theft, non-recovery, poor maintenance, weak governance, and political interference. Privatization, or at least private management under hard performance contracts, needs to move from slogan to execution. Investors will not come into a system where inefficiency is protected and losses are socialized indefinitely.

Fourth, current reforms toward market opening should continue, but with honesty. Recent changes in the CTBCM (Competitive Trading Bilateral Contract Market) framework allowing hybrid consumption are a welcome step in the right direction. They signal movement toward a more flexible and realistic market structure. But nobody should confuse that with a fully workable market. A functioning energy market will still require open access that is genuinely non-discriminatory, transparent wheeling charges, credible balancing arrangements, enforceable contracts, strong system operation and, above all, a wires business that is not crippled by legacy debt and administrative distortion.

In other words, Pakistan must stop trying to build a market on top of a landfill. If the inherited burden remains embedded in the tariff, then every market reform will stall. Consumers will resist. Industry will bypass. Investors will hesitate. Regulators will resort to ad hoc fixes. And the system will continue to oscillate between crisis management and reform theatre.

There is a more sensible path. Separate the past from the present. Put legacy debt into a transparent recovery vehicle. Finance it over time through a mix of budgeted support, dedicated charges, restructuring, and asset monetization. Clean up dispatch. Fix transmission. Commercialize distribution. Let current tariffs increasingly reflect the real cost of current service rather than the weight of historic failure. That is the only way to make electricity affordable enough for industry, sustainable enough for households, and credible enough for privatization and competition.

Pakistan does not need to deny the scale of its energy liabilities. It needs to stop charging the future for them in the most destructive way possible. A country cannot tax current consumption indefinitely to finance accumulated inefficiency and still hope for growth, competitiveness, or reform. If Pakistan wants a serious energy transition, a real market, and a functioning power sector, it must move legacy costs off the backs of current users. Until then, every tariff hike will do what the others have done: punish the productive, protect the broken, and delay the inevitable.

Copyright Business Recorder, 2026

PUBLIC SECTOR EXPERIENCE: He has served as Member Energy of the Planning Commission of Pakistan & has also been an advisor at: Ministry of Finance Ministry of Petroleum Ministry of Water & Power

PRIVATE SECTOR EXPERIENCE: He has held senior management positions with various energy sector entities and has worked with the World Bank, USAID and DFID since 1988. Mr. Shahid Sattar joined All Pakistan Textile Mills Association in 2017 and holds the office of Executive Director and Secretary General of APTMA.

He has many international publications and has been regularly writing articles in Pakistani newspapers on the industry and economic issues which can be viewed in Articles & Blogs Section of this website.

Comments