Sapphire Fibres Limited: performance and outlook

Sapphire Fibres Limited (SFL) experienced fluctuating profitability despite generally rising sales, influenced by currency dynamics, global demand, and strategic diversification into power generation, amidst ongoing cost and market challenges.

- SFL's fluctuating sales, margins, and net profit trends.

- Impact of currency and global demand on export performance.

- Strategic diversification into power and company amalgamations.

- Challenges from rising costs and geopolitical uncertainties.

Sapphire Fibres Limited (PSX: SFL) was incorporated in Pakistan as a public limited company in 1979. The principal activity of the company is the manufacturing and sale of yarn, fabric and garments.

Pattern of Shareholding

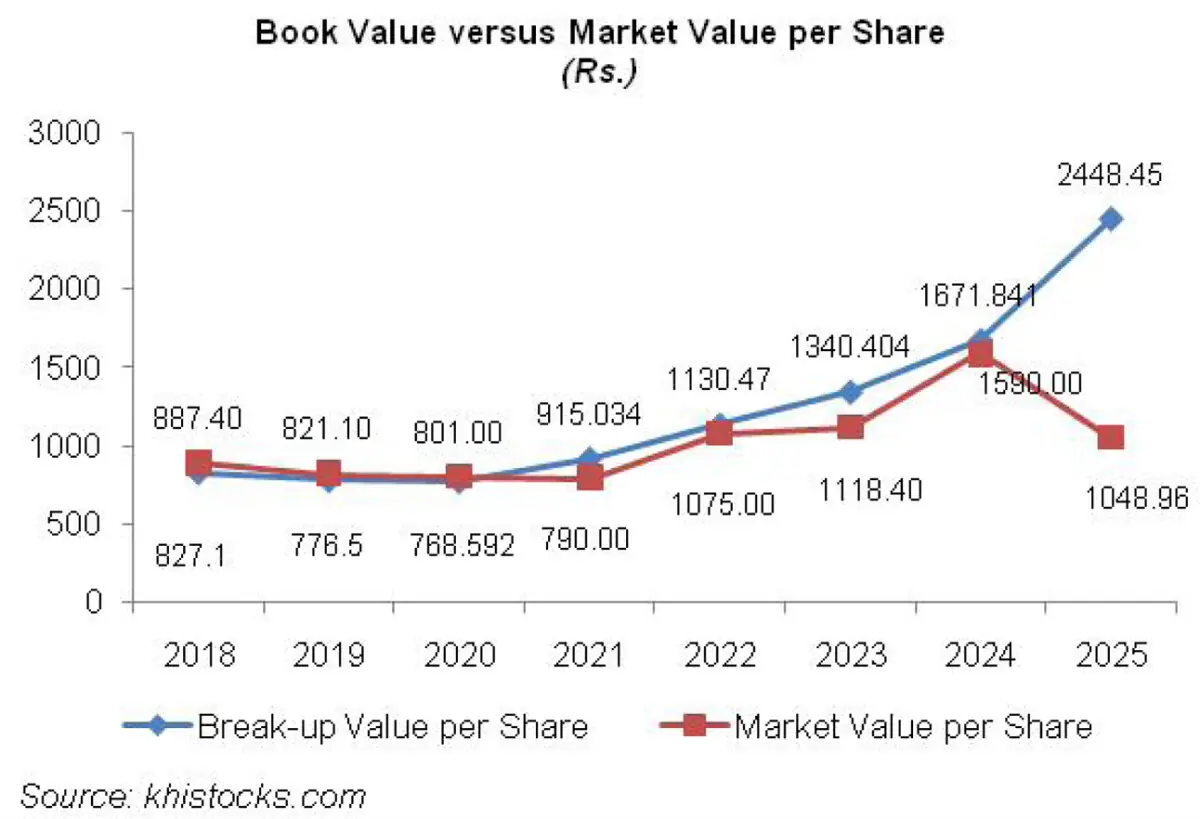

As of June 30, 2025, SFL has a total of 20.672 million shares outstanding which are held by 736 shareholders. Associated companies, undertaking and related parties have the majority stake of 89.61 percent in the company followed by local general public holding 5.55 percent shares.

NIT & ICP account for 3.04 percent shares while Directors, CEO, their spouse and minor children hold 1.38 percent shares.

The remaining shares are held by other categories of shareholders.

Performance Trajectory (2019-25)

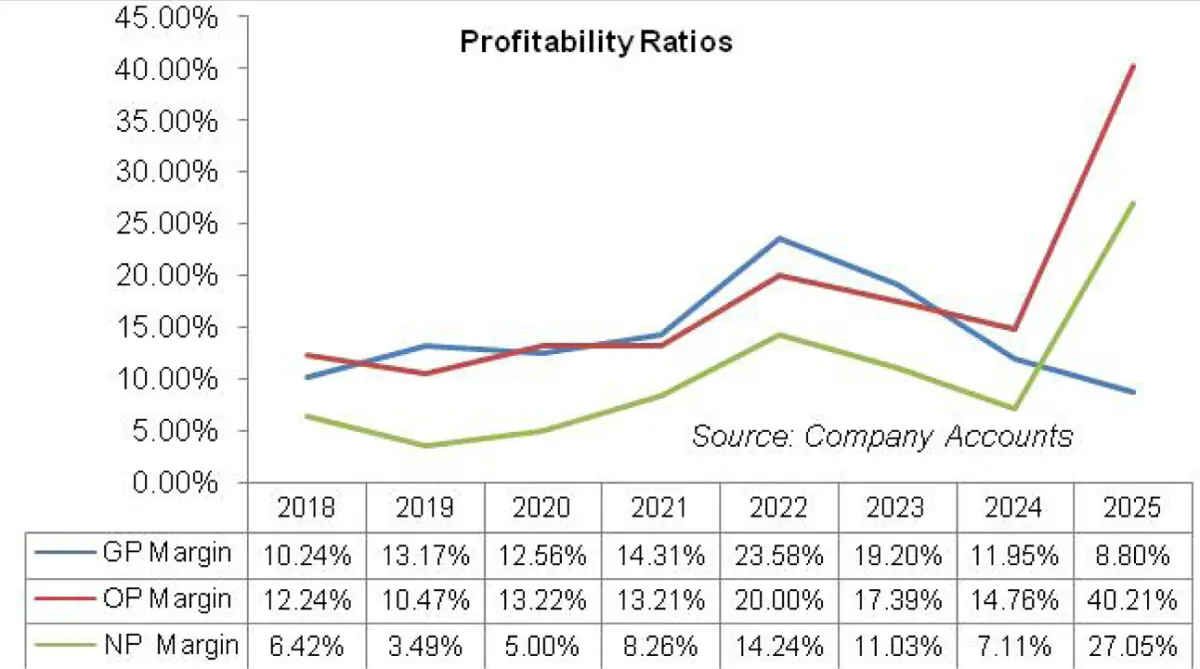

SFL’s topline followed an upward trajectory over the period under consideration. Conversely, its bottomline witnessed a dip thrice during the period i.e. in 2019, 2023 and 2024. SFL’s margins portray an asymmetrical pattern whereby its gross margin improved in 2019 while its operating and net margins considerably declined.

In 2020, gross margin plunged while operating and net margins strengthened. In 2021 and 2022, SFL’s margins boasted incredible growth to hit an unprecedented level in 2022.

The margins registered a decline in 2023 and 2024. In 2025, gross margin continued to plunge while operating and net margins attained their optimum level. The detailed performance review of the period under consideration is given below.

In 2019, SFL’s topline grew by 22 percent year-on-year to clock in at Rs.21,750.25 million. As of June 30, 2019, around 81 percent of the company’s net revenue comprised of export sales.

The growth in export sales during the year was mainly the consequence of Pak Rupee depreciation. Elevated cost of sales due to high energy cost and soaring inflation took its toll on SFL’s international market share resulting in no volume backed growth in revenue.

Declining value of local currency resulted in a higher GP margin of 13.17 percent in 2019 versus GP margin of 10.24 percent recorded in 2018. Distribution expense multiplied by 22.12 percent in 2019 primarily due to higher freight & forwarding charges incurred during the year.

Administrative expense inched up by 3.18 percent in 2019 on account of higher payroll expense. SFL enhanced its workforce from 3833 employees in 2018 to 3975 employees in 2019. Other income dwindled by 62.65 percent year-on-year in 2019 due to suppression of dividend income particularly from related parties.

Other expense also contracted by 51.42 percent in 2019 due to lower profit related provisioning and a dip in provisioning on doubtful tax refunds.

SFL posted 4.44 percent higher operating profit in 2019, however, OP margin fell from 12.24 percent in 2018 to 10.47 percent in 2019. Finance cost escalated by 72.26 percent in 2019 on account of higher discount rate and increased working capital related borrowings obtained during the year.

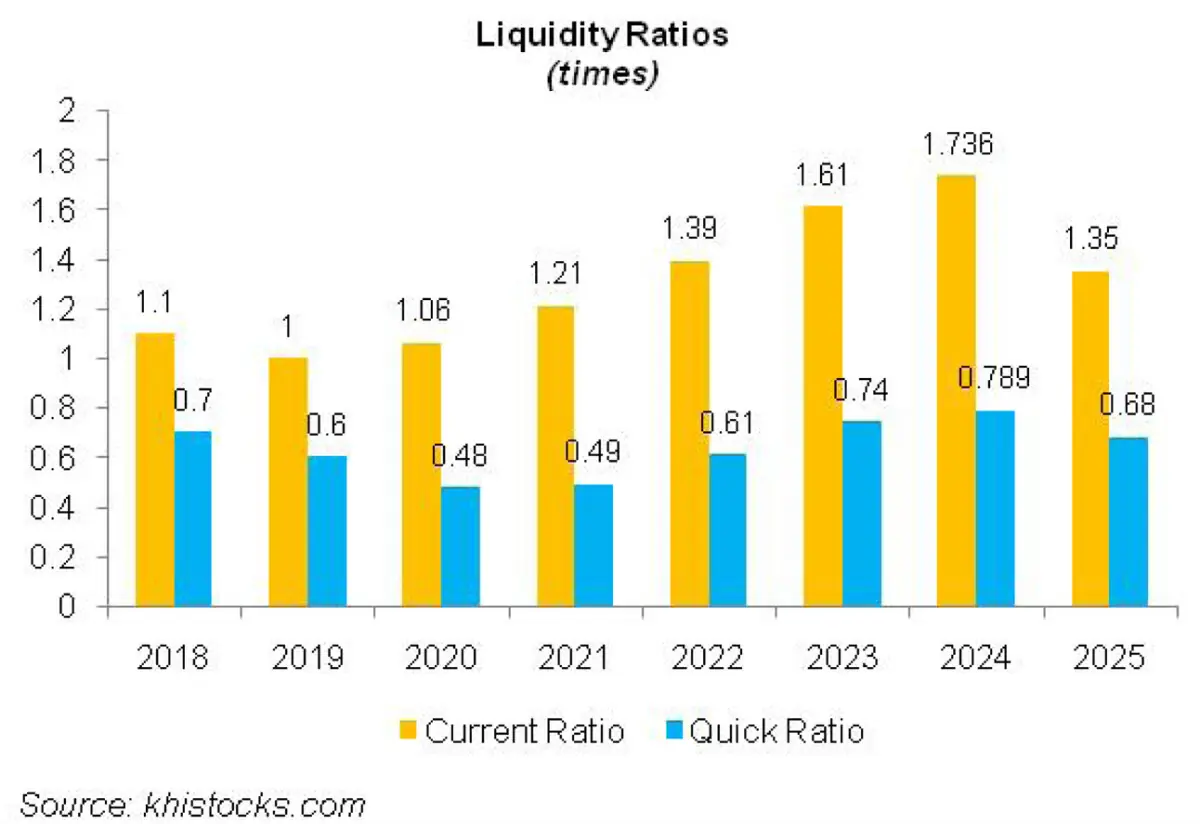

SFL’s gearing ratio climbed up from 46 percent in 2018 to 51 percent in 2019. Net profit shrank by 33.70 percent in 2019 to clock in at Rs.759.197 million with EPS of Rs.36.72 versus EPS of Rs.58.16 recorded in 2018. NP margin slid from 6.42 percent in 2018 to 3.49 percent in 2019.

In 2020, SFL’s net revenues grew by 3.41 percent year-on-year to clock in at Rs. 22,491.62 million. Due to outbreak of COVID-19, businesses, locally and internationally, greatly suffered.

Lockdown imposed during the year didn’t allow the company’s fixed cost to be absorbed effectively, resulting in 1.42 percent slide in gross profit in 2020. GP margin also inched down to 12.56 percent in 2020.

Distribution expense multiplied by 17.39 percent in 2020 due to higher freight & forwarding charges and sales promotion expense incurred during the year. 6.11 percent higher administrative expense incurred during the year was the consequence of increased payroll expense as the company further expanded its workforce to 4192 employees in 2020. 172.52 percent year-on-year rise in other income proved to be a blessing for SFL in 2020. This came on the back of robust dividend income received from related parties in 2020.

Other expense grew by 40.82 percent in 2020 on the back of increased provisioning for WWF and WPPF and also because of re-measurement loss recorded on foreign currency commitments.

SFL’s operating profit strengthened by 30.56 percent year-on-year in 2020 with OP margin climbing up to 13.21 percent. Finance cost surged by 15.92 percent in 2020 due to higher discount rate. SFL’s gearing ratio moved down to 48 percent in 2020.

Net profit rose by 48.23 percent year-on-year in 2020 to clock in at Rs.1125.32 million with EPS of Rs.55.61 and NP margin of 5 percent.

SFL recorded 22.41 percent higher net sales to the tune of Rs.27,531.20 million in 2021. This was on account of splendid rebound in both local and export sales after COVID-19.

Increased volume, upward price revision and operational efficiencies gained during the year translated into 39.54 percent higher gross profit in 2021 with GP margin flying up to 14.31 percent. Distribution expense hiked by 24.84 percent in 2021 due to higher sales commission, freight & forwarding charges and sales promotion expense incurred during the year.

During the year, the company hired additional human resources which took up its workforce to 4752 employees, resulting in higher payroll expense. This coupled with bigger legal & professional charges as well as fee & subscription charges incurred during the year drove up the administrative expense by 12 percent in 2021.

Other income slid by 13.73 percent in 2021 due to lower dividend income which overshadowed the impact of superior gain recorded on disposal of fixed assets in 2021.

Higher profit related provisioning was partially offset by the absence of provision for doubtful tax refunds and re-measurement loss on foreign currency commitments. This resulted in 5 percent uptick in other expense in 2021.

SFL’s operating profit enhanced by 22.26 percent in 2021 with its OP margin staying afloat at 13.2 percent. Finance cost was squeezed by 34.21 percent in 2021 on the back of monetary easing.

Gearing ratio also inched down to 47 percent in 2021. SFL registered a staggering 102.04 percent year-on-year rise in its net profit in 2021 which clocked in at Rs.2273.56 million with EPS of Rs.109.98 and NP margin of 8.26 percent.

In 2022, SFL recorded further 58.5 percent rebound in its net sales which clocked in at Rs.43,637.52 million. While local sales remained lackluster, export sales registered 71.7 percent rise in 2022, grabbing 87.9 percent share in the total sales mix of SFL, compared to 81 percent share recorded in the previous year.

Pak Rupee depreciation played a tremendous role in driving up the export sales and boosting the company’s margins during the year. The company recorded 161 percent year-on-year rise in its gross profit in 2022 with GP margin attaining its peak of 23.58 percent. Distribution expense multiplied by a massive 91.74 percent in 2022 due to drastic hike in export commission as well as freight & forwarding charges.

Administrative expense also surged by 25.66 percent in 2022 due to high payroll expense due to workforce enhancement. SFL’s workforce comprised of 4844 employees in 2022. Other income strengthened by 15 percent in 2022 due to higher dividend earned from unrelated companies.

Other expense surged by 311.78 percent in 2022 due to escalation in the provisioning done for WWF, WPPF and doubtful tax refunds. Operating profit improved by 139.95 percent in 2022 with OP margin climbing up to 20 percent. 73.7 percent year-on-year spike in finance cost in 2022 was the consequence of monetary tightening.

Gearing ratio marched down to 43 percent in 2022 on account of increased equity. SFL posted 173.38 percent growth in its net profit in 2022 which clocked in at Rs.6215.45 million with EPS of Rs.300.67 and NP margin of 14.24 percent.

The magnitude of topline growth which surged to 58.5 percent in 2022 dwindled to a paltry 6.44 percent in 2023. SFL’s net sales were recorded at Rs. 46,446.99 million in 2022. This was due to slowdown of global demand on account of recession in the major export destinations coupled with strict import controls in the local market.

Processing and garments division still managed to bag 52.9 percent increase in sales; however, it was offset by sales decline in spinning and denim divisions. High cost of sales due to Pak Rupee depreciation and hike in raw material and conversion cost resulted in 13.33 percent plunge in gross profit in 2023 with GP margin shrinking to 19.20 percent.

Distribution expense tumbled by 3.69 percent in 2023 due to lesser export commission and freight charges on the back of lackluster off-take. Administrative expense increased by 12.53 percent in 2023 due to higher payroll expense. This was despite the fact that the company streamlined its workforce to 4525 employees in 2023.

Other income grew by 36.96 percent in 2023 on account of higher dividend income from related parties, higher mark-up on loan to related parties as well as exchange gain and reversal of provision on doubtful tax refunds.

Other expense plummeted by 35.29 percent in 2023 due to lesser profit related provisioning booked during the year. SFL recorded 7.42 percent lower operating profit in 2023 with its OP margin moving down to 17.39 percent.

Finance cost grew by 18.63 percent in 2023 due to higher discount rate. This was despite the fact that the company considerably squeezed its debt profile during the year which resulted in a gearing ratio of 34 percent in 2023.

Despite all the efforts to rationalize its outlays, SFL net profit tumbled by 17.61 percent in 2023 to clock in at Rs.5120.787 million with EPS of Rs.247.72 and NP margin of 11 percent.

SFL’s net sales inched up by an insignificant proportion of 2.10 percent to clock in at Rs.47,420.21 million in 2024. This was on account of weak demand in both local and export market on account of decline in the purchasing power of consumers. The company recorded 46 percent decline in the sales of knitting division.

However, it was offset by 21 percent growth recorded in the spinning division and 12 percent growth recorded in the denim division. In 2024, 60.37 percent of the company’s sales were from spinning division followed by 26.10 percent share of denim division and the remaining 13.53 percent sales coming from the knitting division.

Export sales constituted 81.35 percent of the net sales of SFL in 2024. Cost of sales hiked by 11.26 percent in 2024 due to profound inflationary pressure. This resulted in 36.47 percent lower gross profit recorded in 2024 with GP margin of 11.95 percent. Distribution expense ticked down by 9.55 percent in 2024 due to sluggish sales volume resulting in lower export sales commission.

SFL undertook lesser sales promotion activities during the year which also contributed in driving down the distribution expense in 2024.

High inflation continued to drive up administrative expense which posted 16.52 percent hike in 2024. This was mainly on account of higher payroll expense, utility expense, and vehicle running charges, entertainment charges, legal & professional charges and depreciation expense booked during the year.

Number of employees also increased to 4662 in 2024. SFL curtailed its profit related provisioning and registered 83.40 percent lower other expense in 2024. Other income greatly buttressed the financial performance of SFL in 2024. 91.63 percent higher other income recorded by SFL in 2024 mainly comprised of dividend income, markup income, exchange gain and reversal of provision booked for ECL and WWF.

Despite robust other income, SFL’s operating profit inched down by 13.39 percent in 2024 with its OP margin clocking in at 14.76 percent which although was lower than the OP margin of 17.39 percent recorded by the company in 2023, however, was higher than the GP margin for the current year.

Finance cost built up by 40.31 percent in 2024 due to higher discount rate. Lower outstanding borrowings at the end of the year resulted in a thinner gearing ratio of 18 percent in 2024.

SFL’s net profit slumped by 34.13 percent year-on-year in 2024 to clock in at Rs.3373.03 million with EPS of Rs.163.17. NP margin also moved down to 7.11 percent in 2024.

In 2025, SFL recorded 6.63 percent uptick in its net sales which clocked in at Rs.50,561 million. During the year, the company’s local sales grew tremendously while its export sales drastically fell.

Local sales which accounted for 18.52 percent of the total sales of SFL in 2024 grabbed 50.11 percent share of the total sales mix in 2025. Besides subdued volume, stability of local currency also played a role in driving down export revenue in 2025.

Cost of sales mounted by 10.43 percent in 2025 mainly on account of higher energy cost and lower domestic cotton output due to adverse weather condition, forcing the company to use imported cotton. This resulted in 21.45 percent downtick recorded in gross profit.

GP margin also fell to 8.80 percent in 2025. Distribution expense surged by 18.25 percent in 2025 due to elevated sales commission and freight charges. Inflationary pressure resulted in 37.20 percent higher administrative expense in 2025.

Other income boasted a staggering 401 percent growth in 2025 on account of robust dividend income worth Rs. 18.60 billion from related parties.

Other expense ticked up by 6.18 percent in 2025 due to greater provisioning done for doubtful tax refunds. SFL recorded 190.52 percent stronger operating profit in 2025 with OP margin clocking in at 40.21 percent.

Finance cost plummeted by 25.43 percent in 2025 due to monetary easing. This was despite the fact that the company’s short-term borrowings significantly escalated during the year in order to meet its working capital requirements. Gearing ratio was recorded at 23 percent in 2025 versus 18 percent in the previous year.

SFL’s net profit improved by 305.48 percent to clock in at Rs.13,676.837 million in 2025. This translated into EPS of Rs.661.62 and NP margin of 27 percent in 2025.

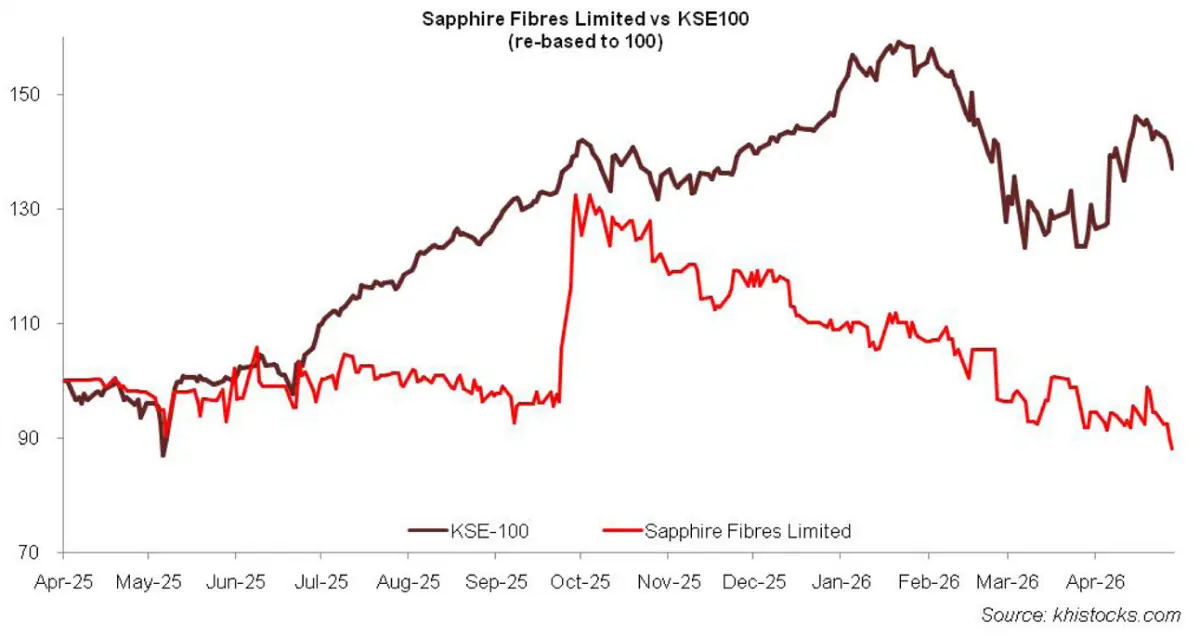

Recent Performance (9MFY26)

During the nine-month period of the ongoing fiscal year, SFL’s net sales ticked down by 12.33 percent to clock in at Rs.34,586.997 million. Both local and export sales dipped during the period under review.

High cost of sales squeezed the company’s gross profit by 56 percent in 9MFY26 resulting in GP margin of 4.87 percent versus GP margin of 9.70 percent recorded in 9MFY25. Lower sales pushed down distribution expense by 17.81 percent in 9MFY26.

Conversely, administrative expense continued to spike to the tune of 22.33 percent in 9MFY26 due to revision of minimum wage rate. 90.64 percent stronger other income recorded in 9MFY26 was the result of superior dividend income from related parties particularly UCH-I Power (Private) Limited and UCH-II Power (Private) Limited, both incorporated in the UAE.

Increased provisioning for doubtful receivables as well as elevated profit related provisioning appears to have inflated other expense by 41 percent in 9MFY26. SFL’s operating profit ticked up by 8.47 percent in 9MFY26 with OP margin clocking in 13 percent versus OP margin of 10.54 percent in 9MFY25.

Despite monetary easing, finance cost surged by 14.61 percent in 9MFY26 due to increased outstanding debt at the end of the period. Net profit progressed by 13.87 percent to clock in at Rs.1541.676 million in 9MFY26. This translated into EPS of Rs.74.58 and NP margin of 4.46 percent in 9MFY26 versus EPS of Rs.65.49 and NP margin of 3.43 percent recorded in 9MFY25.

Future Outlook

Besides spreading its wings in the local and export markets, SFL is actively seeking to broaden the avenues of its alternate including both interest and non-interest income. After completing the acquisition of 50 percent shares each in UCH-I Power(Private) Limited and UCH-II Power (Private) Limited, the company has announced the amalgamation of Reliance Cotton Spinning Mills Limited (an Associated Company) with and into the Company to further expand its operations.

On the downside, rising geopolitical tensions have raised uncertainty in the global market resulting in demand destruction.

Meanwhile, rising cost pressures in the local market is taking its toll on the cost competitiveness of the local textile companies. How SFL and other indigenous textile peers perform in this challenging time is yet to be seen.

Comments