The Searle Company Limited (PSX: SEARL) was incorporated in Pakistan as a private limited company in 1965 and was later converted into a public limited company.

The principal activity of the company is the manufacturing and sale of pharmaceutical, consumer health and nutritional products. SEARL is a subsidiary of International Brands (Private) Limited.

Pattern of Shareholding

As of June 30, 2025, SEARL has a total of 511.494 million shares outstanding which are held by 21,458 shareholders. International Brands (Private) Limited, the parent company of SEARL, holds 51.89 percent of its outstanding shares followed by local general public having a stake of 26.43 percent in the company.

Around 5.34 percent of the company’s shares are held by Trusts & Funds, 4.89 percent by foreign companies and 4.01 percent by Banks, DFIs and NBFIs.

Modarabas & Mutual funds account for 3.24 percent of SEARL’s shares while joint stock companies hold 2.91 percent shares. Foreign general public hold 1.69 percent shares of SEARL. The remaining shares are held by other categories of shareholders.

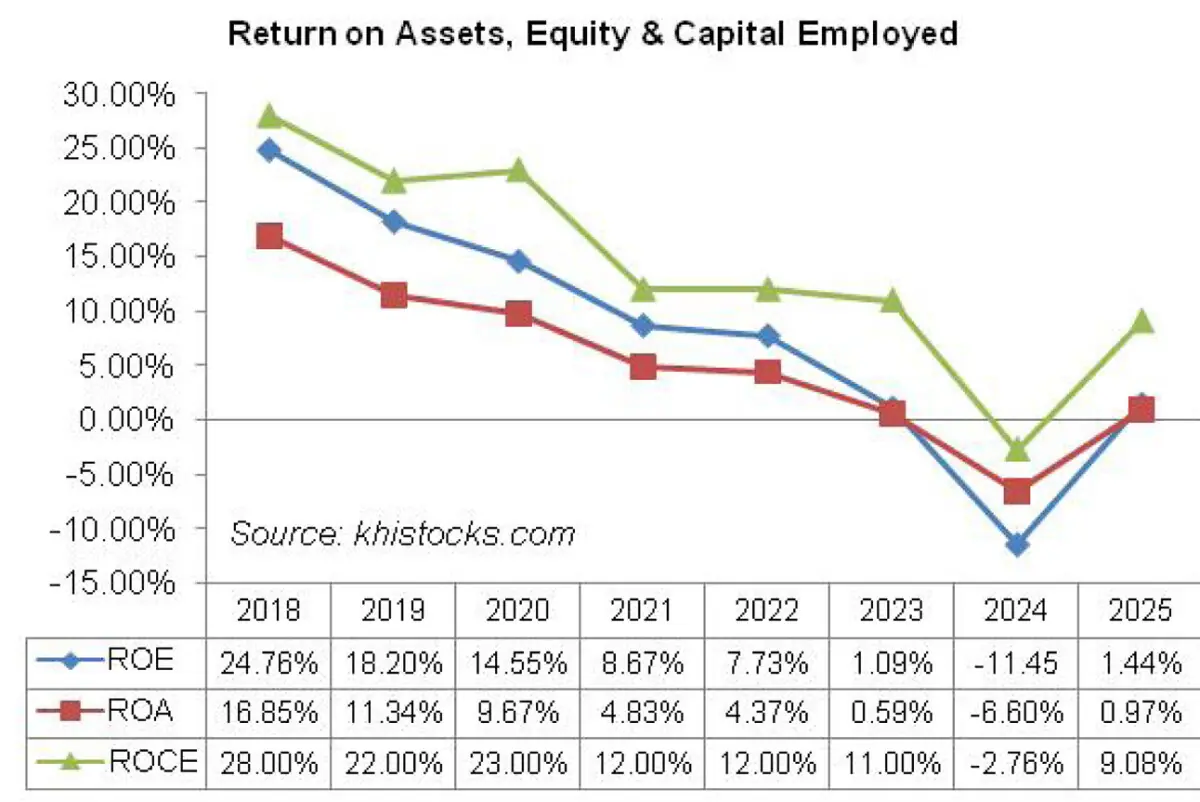

Historical Performance (2019-25)

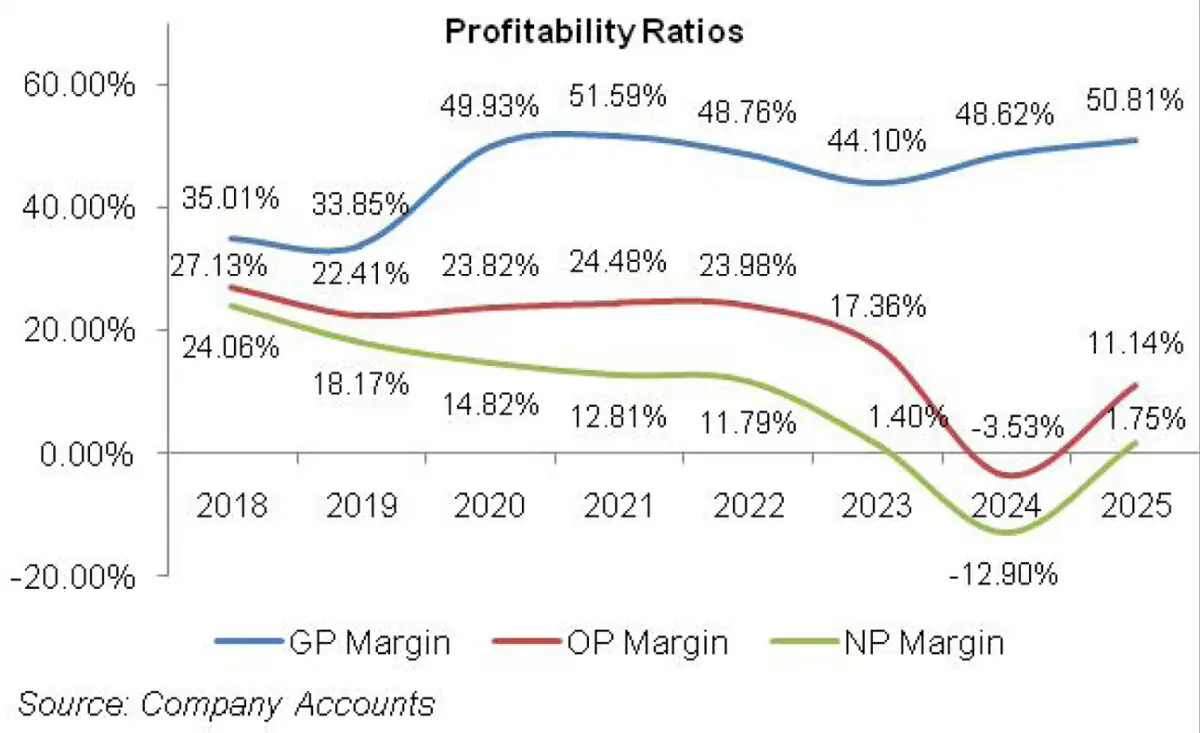

Except for a marginal downtick recorded in 2025, SEARL’s topline posted year-on-year growth in all the years under consideration. Its bottomline which had been shrinking since 2018 posted net loss in 2024. In 2025, despite thinner topline, the company recovered from net loss.

Gross and operating margins assumed their optimum level in 2021 which was the time of outbreak of COVID-19. The margins subsided in the subsequent three years except for an uptick posted by gross margin in 2024. In 2025, all the margins considerably recovered. The detailed performance review of the period under consideration is given below.

In 2019, SEARL’s topline touted 14.69 percent year-on-year growth to clock in at Rs. 14,537.20 million. This came on the back of strengthened demand, rich product mix and stringent branding efforts.

As local pharmaceutical industry heavily relied on the imports of active pharmaceutical ingredient (API), local currency depreciation resulted in 16.74 percent year-on-year surge in cost of sales.

This pushed GP margin down from 35 percent in 2018 to 33.85 percent in 2019. In absolute terms, gross profit ticked up by 10.88 percent in 2019. Distribution expense went up by 17.43 percent year-on-year in 2019 on the back of rise in salaries and wages of sales force coupled with extensive advertising and promotion, samples expense etc.

Administrative expense largely remained in check in 2019. SEARL booked lesser provisioning for WWF and WPPF which pushed other expense down by 13.36 percent year-on-year in 2019. Other income slightly dwindled by 3.98 percent in 2019 due to lesser dividend income from subsidiary companies.

All these factors contributed to 5.23 percent year-on-year slide in operating profit during 2019 which culminated into OP margin of 22.41 percent as against OP margin of 27.13 percent posted in the previous year. To further weaken the bottomline, finance cost amplified by a massive 108.89 percent year-on-year in 2019 which was the result of rate hike coupled with increased short-term borrowings during the year.

Exchange loss also contributed a great deal in driving the finance cost up in 2019. Consequently, bottomline slumped by 13.36 percent year-on-year to clock in at Rs.2641.95 million in 2019 with NP margin of 18.17 percent as against NP margin of 24 percent posted in 2018. EPS also dropped from Rs.14.35 in 2018 to Rs.12.44 in 2019.

In 2020, SEARL’s revenue grew by 13.96 percent year-on-year to clock in at Rs.16,657.22 million. While many other businesses suffered due to COVID-19 and the associated measures and restrictions imposed by the government to contain the disease, the novel virus proved to be a boon for the pharmaceutical sector and harnessed its integration among the masses.

Pakistan’s pharmaceutical sector’s sales grew by 13.23 percent during the year. Besides, volumetric growth, Drug Regulatory Authority of Pakistan (DRAP) pricing policy which was linked to CPI also produced a positive impact on the revenue of SEARL and its counterparts.

SEARL enjoyed market share of 6.5 percent in 2020 as against market share of 5.3 percent recorded during the last year. Cost of sales went down by 13.74 percent year-on-year as the company discontinued toll manufacturing services from its subsidiary Searle Pharmaceuticals (Private) Limited.

This reduced its processing charges by manifold. The result was 68.12 percent year-on-year surge in gross profit, driving the GP margin up to 49.93 percent in 2020. Distribution expense grew by a marginal 1.72 percent year-on-year in 2020 as SEARL considerably trimmed its advertising and promotion budget, sample expense as well as travelling expense due to restriction on the movement of people and goods on account of COVID-19.

Administrative expense ticked up by 18.97 percent year-on-year during 2020 owing to a hike in salaries and wages, corporate services charged by the holding company as well as generous donations and charities given during the year. Other expense posted a humungous 70.17 percent year-on-year rise on the back of higher provisioning done for WPPF, WWF and Central Research fund (CRF).

Other income shrank by 74.83 percent year-on-year as SEARL received lesser dividend income from subsidiary companies. The major impact was created by Searle Pharmaceutical (Private) Limited which had a lion’s share in last year’s other income pie, however, it didn’t pay any dividend in 2020. Operating profit magnified by 21.11 percent year-on-year in 2020 with OP margin clocking in at 23.82 percent.

Finance cost grew by 49.87 percent year-on-year as discount rate was higher during the first three quarters of FY20 coupled with increased borrowings during the year.

Higher taxation due to the imposition of super tax as well as elevated finance cost barred the growth in operating profit from cascading down and pushed net profit down by 7 percent year-on-year in 2020.

Net profit clocked in at Rs.2455.08 million in 2020 with EPS of Rs.11.56. Higher taxation trimmed down the NP margin to 14.82 percent.

In 2021, SEARL’s topline posted a negligible year-on-year growth of 0.01 percent to clock in at Rs.16,569.60 million.

Cost of sales slid by 3.31 percent year-on-year due to lesser raw and packing materials charges as well as processing charges incurred during the year due to stability shown by Pak Rupee. GP margin hit its optimum level of 51.59 percent in 2021. Distribution and administrative expense posted year-on-year rise of 9.14 percent and 9.39 percent respectively in 2021.

The main growth drivers were higher salaries and wages, carriage and duties, sample expense and travelling expense. Other expense took 21 percent nosedive in 2021 due to lesser provisioning done for WWF,WPPF and CRF. Other income ascended by 28.84 percent year-on-year in 2021 on the back of handsome dividend from OBS Pakistan (Private) Limited, a subsidiary of SEARL. Operating profit inched up by 2.81 percent year-on-year with OP margin reaching 24.48 percent in 2021. A steep 106.14 percent rise in finance cost despite monetary easing was the result of a sizeable Rs.9.5 billion worth Musharaka facility (long-term) obtained by the company coupled with higher running finance facility availed during the year.

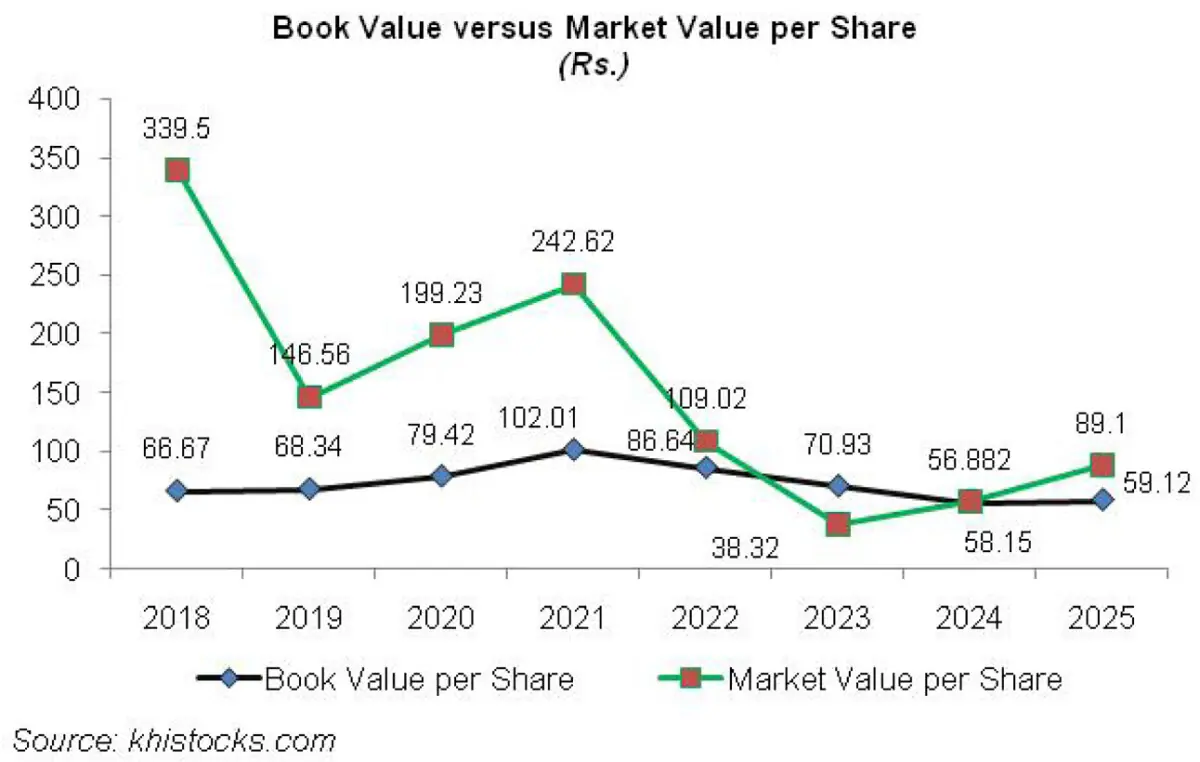

This translated into 13.53 percent year-on-year drop in net profit of SEARL which stood at Rs.2122.92 million in 2021 with NP margin of 12.81 percent. High finance cost diluted NP margin of SEARL in 2021 while its GP and OP margin during the year were visibly greater than the last year’s margins. The issue of 27.6 million right shares during the year resulted in 39.36 percent year-on-year decline in EPS which stood at Rs.7.01 in 2021.

In 2022, SEARL’s topline grew by 7 percent year-on-year to clock in at Rs.17,737.28 million. High cost of sales on the back of unprecedented level of inflation and rapidly depreciating value of local currency resulted in 13.32 percent rise in cost of sales which eclipsed the growth of gross profit. GP margin went down to 48.76 percent in 2022. Distribution expense multiplied by 19 percent year-on-year in 2022 due to higher advertising budget, traveling charges, carriage and duties incurred and salaries including bonus given to salesmen.

Administrative expense grew by a mere 3.19 percent during 2022 which was the result of higher depreciation as well as repair and maintenance charges incurred during the year. Other expense and other income showed favorable movements during the year whereby the former slid by 27.92 percent while the latter rose by 85.54 percent.

The staggering growth in other income came on the back of handsome dividend from subsidiary companies particularly Searle Pakistan Limited. Operating profit registered 4.86 percent year-on-year rise while OP margin slightly lowered to clock in at 23.98 percent during 2022. Finance cost surged by 45.56 percent year-on-year in 2022 due to excessive monetary tightening which drastically increased the cost of borrowing during the year. Higher short-term borrowings also contributed to an increase in finance cost during 2022. SEARL’s bottomline slipped by 1.52 percent year-on-year in 2022 to clock in at Rs.2090.72 million with NP margin of 11.80 percent. EPS slid to Rs.5.36 in 2022.

During 2023, SEARL’s topline boasted a staggering 22 percent year-on-year rise to clock in at Rs. 21,641.28 million. Yet, it couldn’t trickle down to produce a robust bottomline. Significant Pak Rupee depreciation, increase in global commodity prices as well as increased energy cost resulted in 33.10 percent increase in cost of sales in 2023. This pushed GP margin down to 44.10 percent in 2023.

High operating expense due to unsurpassed inflation level coupled with deteriorating other income on the back of low dividend income shoved operating profit down by 11.67 percent year-on-year in 2023. OP margin also slumped to 17.36 percent in 2023. 73.95 percent higher finance cost due to multiple rounds of monetary tightening resulted in 85.55 percent year-on-year shrinkage in net profit which clocked in at Rs.302.137 million in 2023. This translated into a thin NP margin of 1.40 percent in 2023. EPS was recorded at Rs.0.75 in 2023.

In 2024, SEARL’s topline strengthened by 19.34 percent year-on-year to clock in at Rs.25,827.21 million. This was mainly driven by price increase due to deregulation of prices of non-essential medicines by the DRAP. Cost of sales grew by 9.70 percent in 2024. This translated into 31.57 percent higher gross profit recorded in 2024 with GP margin clocking in at 48.62 percent.

Distribution expense grew by 30.18 percent in 2024 due to increased salaries and bonuses to salesmen as well as elevated advertising and travelling expenses incurred during the year. Administrative expense also escalated by 18.96 percent in 2024 mainly on account of reimbursement of expenses incurred on behalf of the holding company for tender based sales. The company didn’t do any provisioning for WPPF and ECL, resulting in 55 percent lower other expense recorded during the year. The divestiture of Searl Pakistan (Private( Limited resulted in no dividend income from the company.

This translated into 63.88 percent year-on-year decline in other income in 2024. SEARL also booked impairment loss of Rs. 5200 million on its investment in subsidiary, Searl Pakistan Limited. This resulted in operating loss of Rs.910.611 million recorded in 2024. Finance cost posted a paltry growth of 6.36 percent in 2024 due to reduced borrowings. This was the result of divesture of Searl Pakistan Limited which provided enough liquidity to the company. SEARL posted net loss of Rs.3330.859 million in 2024. This translated into loss per share of Rs.6.95 in 2024.

In 2025, SEARL’s topline posted a paltry year-on-year dip of 4 percent to clock in at Rs.24,773.37 million. This was the result of external supply chain challenges coupled with the company’s strategy to enhance efficiency in channel inventories. Around 62.22 percent of the company’s net sales comprised of revenue from IBL Operations (Private) Limited - a related party of SEARL. Its share was recorded at 76.41 percent of the SEARL’s net revenue in the previous year.

In absolute terms, gross profit ticked up by 0.25 percent in 2025, however, GP margin climbed up to 50.81 percent. This was due to upward price adjustments following the deregulation of prices of non-essential medicines and also because of stability of Pak Rupee which eased the cost pressures. Distribution expense inched up by only 4.17 percent in 2025 due to no considerable movement recorded in sales volume. Conversely, administrative expense mounted by 21.55 percent in 2025 mainly on the back of elevated payroll expense, legal and professional charges paid for the disposal of subsidiary as well as software maintenance charges incurred during the year. SEARL expanded its workforce from 3036 employees in 2024 to 3308 employees in 2025. Higher profit related provisioning and provisioning done for ECL and CRF was the cause of 202 percent spike recorded in other expense in 2025.

Other income strengthened by 11.20 percent in 2025 due to unwinding of deferred consideration and interest on delayed payments as well as higher rental income from investment property. SEARL’s other income completely wiped off its other expense, resulting in net other income of Rs.307.95 million in 2025. Impairment loss on investment in subsidiary dropped by 82.16 percent in 2025. The company was able to post operating profit of Rs.2760.76 million in 2025 with OP margin clocking in at 11.14 percent. Finance cost slumped by 43 percent in 2025 due to lower discount rate and settlement of long-term liabilities to its entirety. The long-term debt had originally been obtained for the acquisition of Searle Pakistan Limited. This helped the company record net profit of Rs.434.038 million in 2025 with EPS of Rs.0.85 and NP margin of 1.75 percent.

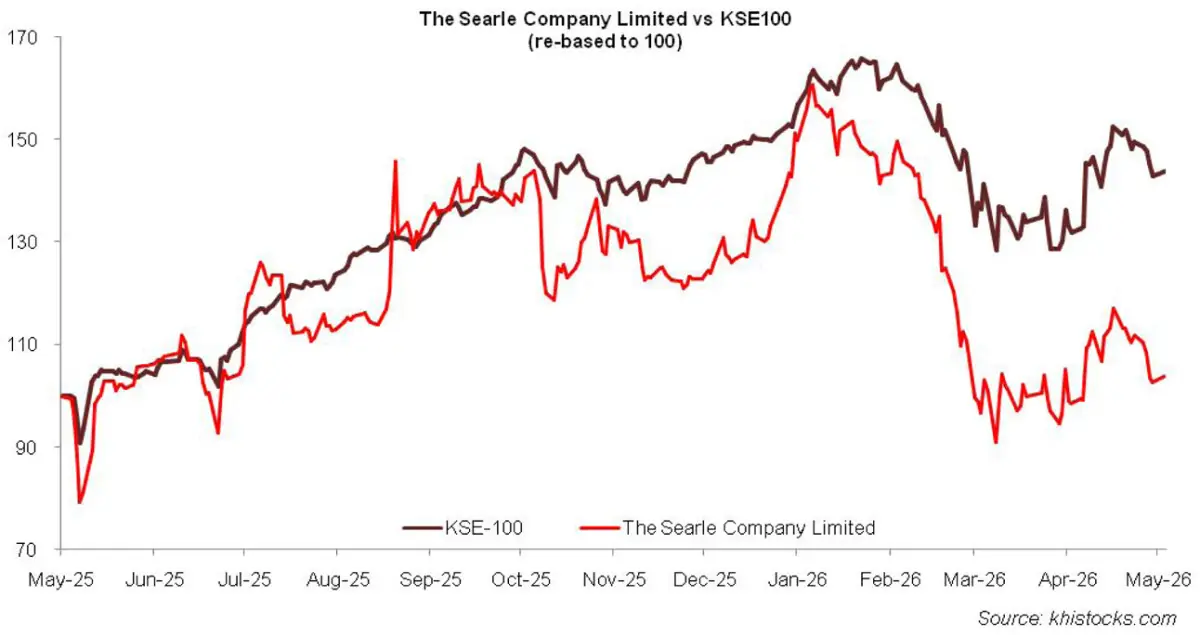

Recent Performance (9MFY26)

During the nine-month period of the ongoing fiscal year, SEARL posted a phenomenal 37 percent growth in its net sales which was recorded at Rs.26,185.46 million. This was the result of optimization of supply chain operations which improved the product availability, favorable sales mix and strategic price adjustments undertaken during the period. Gross profit strengthened by 50.17 percent in 9MFY26 with GP margin clocking in at 55.12 percent versus GP margin of 50.28 percent recorded in 9MFY25. Stability of local currency also had a prominent role to play in supporting the company’s gross margin. Greater sales volume and superior commercial execution pushed up distribution expense by 52.50 percent in 9MFY26.

Conversely, administrative expense dipped by 21.97 percent in 9MFY26 likely due to high-base effect as the company incurred legal charges pertaining to divestment of Searle Pakistan Limited in the comparative period. Increased provisioning done for WWF, WPPF, ECL and CRF appear to have pushed up SEARL’s other expense by 1024.47 percent in 9MFY26. Other income also ticked up by 19.70 percent in 9MFY26, however, couldn’t offset other expense. This resulted in net other expense of Rs.62.22 million in 9MFY26 versus net other income of Rs.236.62 million registered in 9MFY25. No impairment loss recorded on the investment in subsidiary in 9MFY26 also buttressed SEARL’s profitability in 9MFY26.

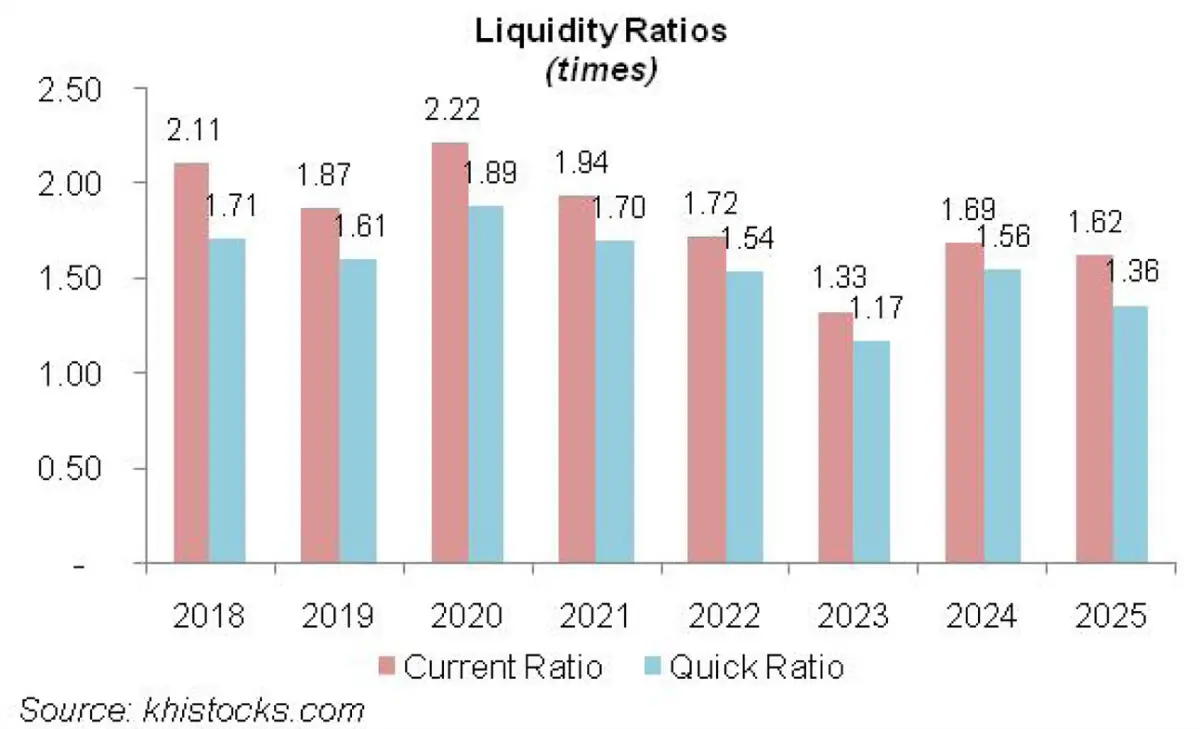

Operating profit mounted by 145.57 percent in 9MFY26 with OP margin clocking in at 19.84 percent versus OP margin of 11 percent posted in 9MFY25. Finance cost diminished by 53.72 percent in 9MFY26 due to monetary easing and settlement of long-term loan following the divestment of Searle Pakistan Limited. This resulted in a gearing ratio of 21 percent in 2025 versus 31 percent in 2024. SEARL’s net profit enhanced by a staggering 759 percent to clock in at Rs.2309.160 million in 9MFY26. This translated into EPS of Rs.3.93 and NP margin of 8.82 percent in 9MFY26 versus EPS of Rs.0.46 and NP margin of 1.41 percent recorded in 9MFY25.

Future Outlook

The company has been able to muster healthier net sales and margins due to an end to restrictive drug pricing mechanism. This coupled with favorable sales mix, new product launches, discharge of liabilities and divestment of subsidiary will pave way for further improvement in SEARL’s financial performance. The company is also continually expanding its footprint in GCC and CIS which will further diversify its geographical mix.

SEARL is in the process of relentlessly rationalizing its product portfolio by transferring a few products to its subsidiaries. This will enable the company to focus more on its strategic product lines and undertake R&D to introduce new unmatched products. The recent approval for the selling and marketing of Denosumab injections (used for osteoporosis management and oncology care) by the DRAP will further enhance SEARL’s leadership in the fields of biotechnology and biosimilars. Earlier, the company had also gained approval for Adalimumab (used for rheumatoid arthritis and Crohn’s disease) which was Pakistan’s first locally manufactured biosimilar.

Comments