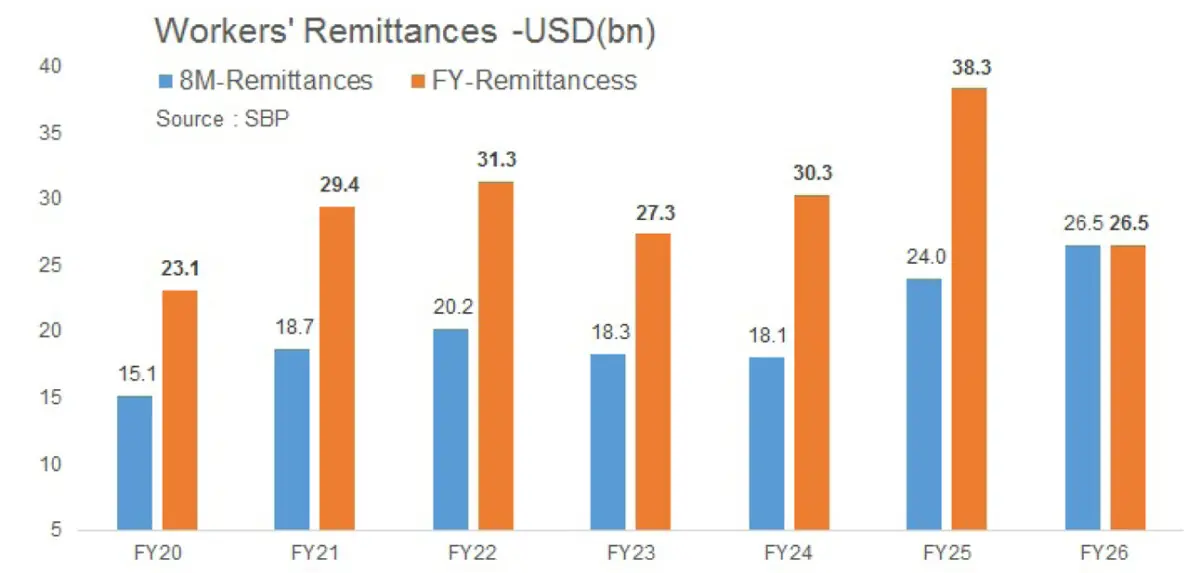

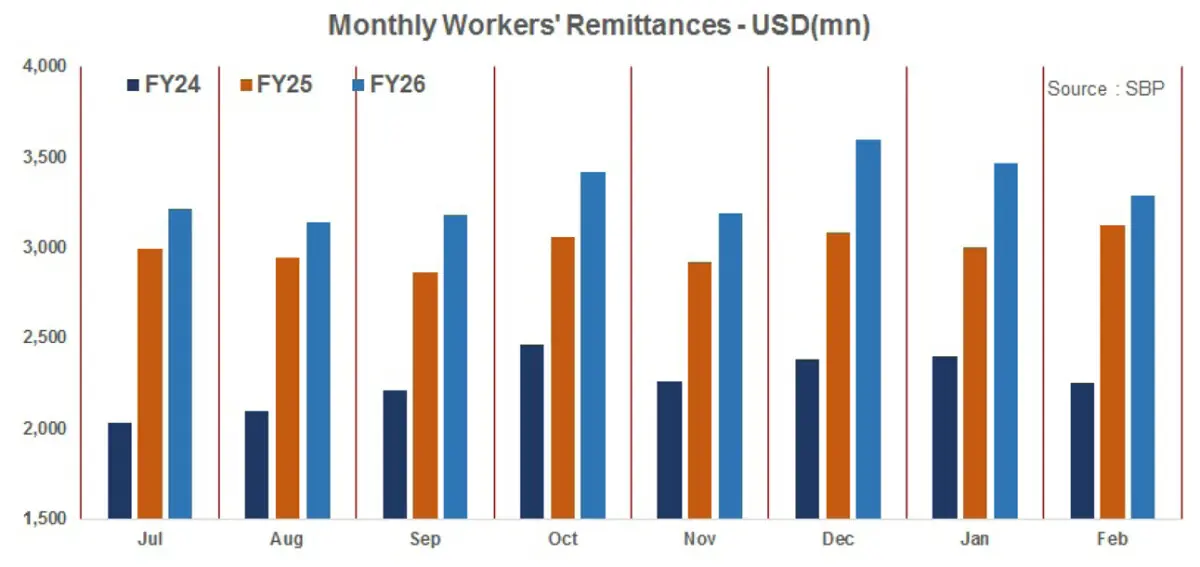

Pakistan’s remittances have remained remarkably resilient so far this year. According to SBP, workers’ remittances stood at $3.29 billion in February 2026, up 5.2 percent year-on-year. Cumulatively, inflows reached $26.5 billion in 8MFY26, compared with $24.0 billion in the same period last year, an increase of 10.5 percent. On the surface, these are comforting numbers. But the real question is not what remittances look like today. It is how long this strength can last in the ongoing war between Iran and the US/Israel.

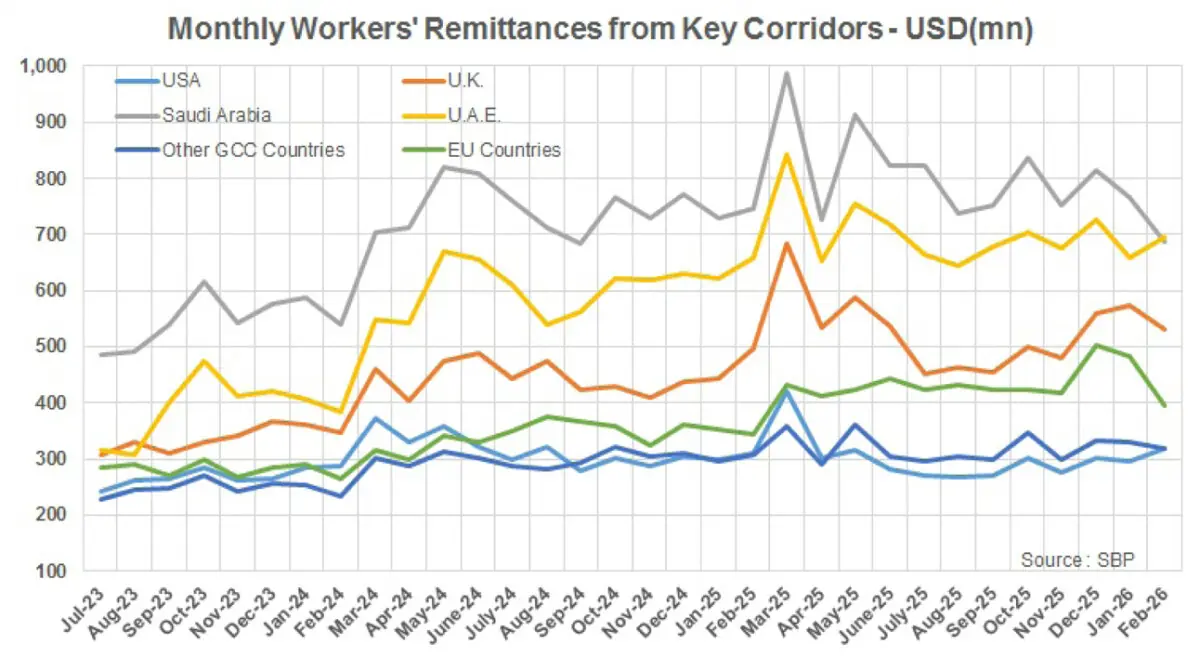

Pakistan’s direct economic exposure to Iran may be limited, but its indirect exposure through the Gulf is anything but small. According to SBP’s March 2026 monetary policy compendium, Saudi Arabia accounted for 23.5 percent of remittances in FY26 through February, the UAE for 20.6 percent, and the rest of the GCC for another 9.5 percent. That means more than half of Pakistan’s remittance inflows are tied to Gulf economies. This is where the real vulnerability lies. Any conflict that unsettles the Gulf, disrupts trade routes, weakens business confidence, or affects employment conditions can eventually feed into Pakistani households through the remittance channel.

The issue is not only near-term disruption. It is also the growing concentration of Pakistan’s external lifeline in a region which is not secure and thriving as it was before. If the present conflict leaves behind a lasting perception that the region is no longer fully insulated from geopolitical escalation, the consequences may extend well beyond oil.

Investment decisions could become more cautious, expansion plans could slow, and future job creation may soften. For a country like Pakistan, which relies heavily on Gulf-based workers and businesses for remittance support, which would create a medium-term risk even if current hostilities ease in the short run.

If the war drags on, those risks become more serious. A prolonged conflict would not just keep oil and energy prices elevated; it could also raise shipping and insurance costs, delay projects, dent investor sentiment, and slow private-sector activity across the Gulf. That is when remittances could begin to weaken. Not necessarily through a sudden collapse, but through a gradual squeeze: fewer new jobs, slower wage growth, delayed payments, reduced working hours, and softer demand in sectors that employ large numbers of migrant workers.

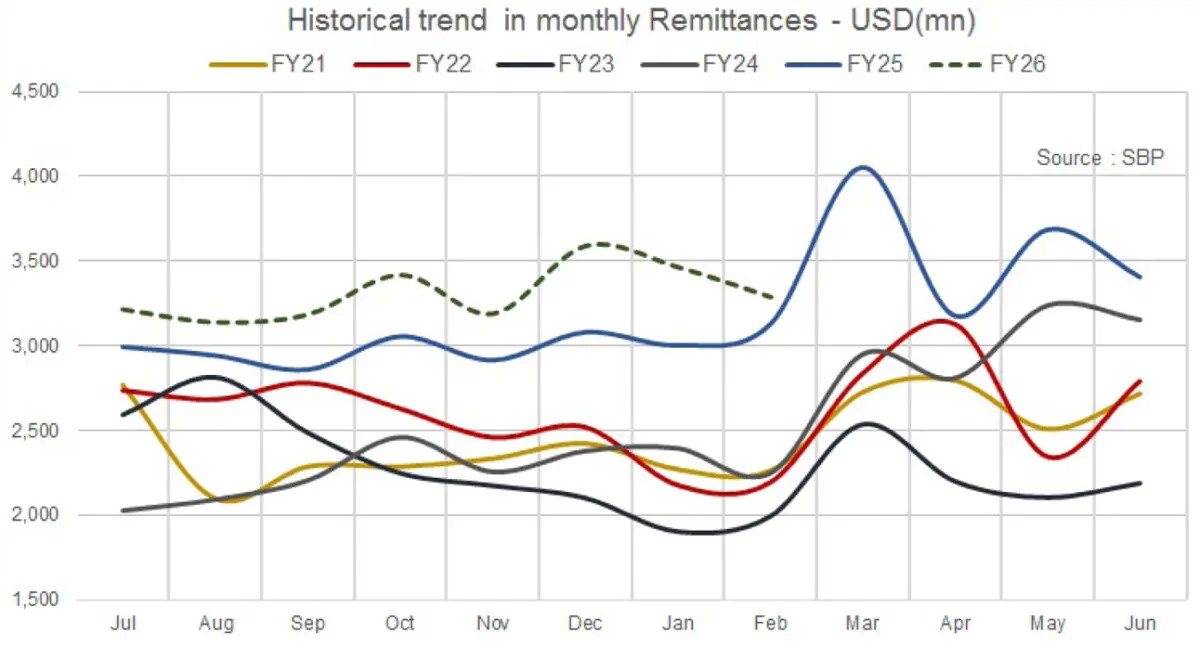

There is also an important timing issue. The next few months may not immediately reveal this pressure. Around Ramadan and Eid, remittances often receive a seasonal boost as overseas Pakistanis send more money home for family support and religious spending.

In times of uncertainty, precautionary transfers may even increase. So, the first effect of the conflict may not show up as falling remittances at all. It may instead appear as continued strength in the numbers, even while the underlying risks are becoming more pronounced. That is especially plausible given the already strong base.

This is why Pakistan should be careful not to read current remittance resilience as a sign that all is well. Remittances are not just family transfers; they are one of Pakistan’s most important economic shock absorbers.

They support household consumption, help finance the trade gap, and reduce pressure on the external account. If Gulf labour markets remain unstable, that cushion may start thinning at exactly the wrong time.

For now, the remittance lifeline is still intact. But the larger concern is no longer just whether the current war causes a temporary shock. It is whether it marks the start of a more fragile Gulf environment in which repeated episodes of conflict, higher perceived risk, and slower economic momentum gradually erode the job and income base that sustains remittances to Pakistan. That is the risk worth watching now.

Comments