The Federal State-Owned Enterprises Annual Aggregate Report FY25 is a sobering read. Pakistan’s federal SOEs recorded a net adjusted loss of Rs 123 billion — more than four times last year’s loss. But the real concern is not just one bad year. It is the direction of travel.

Revenues fell 8 percent to Rs 12.4 trillion, and profits from the better-performing entities also declined. While total equity rose to Rs 6.2 trillion, this increase did not come from stronger performance. It came mainly from government recapitalisation, especially in the power sector, to manage circular debt. In simple terms, taxpayers stepped in to repair balance sheets that operations could not sustain.

The broader picture is worrying. The average return on invested capital across SOEs is just 2.2 percent, while the cost of capital is about 15 percent. No private investor would accept this. The state absorbs it — for now.

Government support to SOEs increased 37 percent to Rs 2 trillion, equal to roughly 16 percent of federal tax revenue. At the same time, the net cash these enterprises returned to the government collapsed to just Rs 41 billion. In effect, SOEs are taking far more from the budget than they are giving back. Financial stress indicators, including solvency measures, suggest the portfolio is operating dangerously close to distress.

READ MORE: FY25 SOE losses hit Rs832.848bn mark

Profits are heavily concentrated. Nearly 90 percent of total profits come from a few large entities — mainly in oil and gas and banking. Companies such as Oil and Gas Development Company Limited, Pakistan Petroleum Limited, and National Bank of Pakistan remain the main profit engines, along with WAPDA and Government Holdings (Private) Limited. Yet even here, profits are under pressure.

On the other side are 25 loss-making SOEs, with combined annual losses of Rs 833 billion and accumulated losses of Rs 6.8 trillion. The biggest burdens come from National Highway Authority, Pakistan Railways, PIA Holding Company Limited, and several power distribution companies such as Quetta Electric Supply Company and Peshawar Electric Supply Company. Many of these entities recover only 80 paisa for every rupee they spend. The rest is financed through borrowing or government transfers.

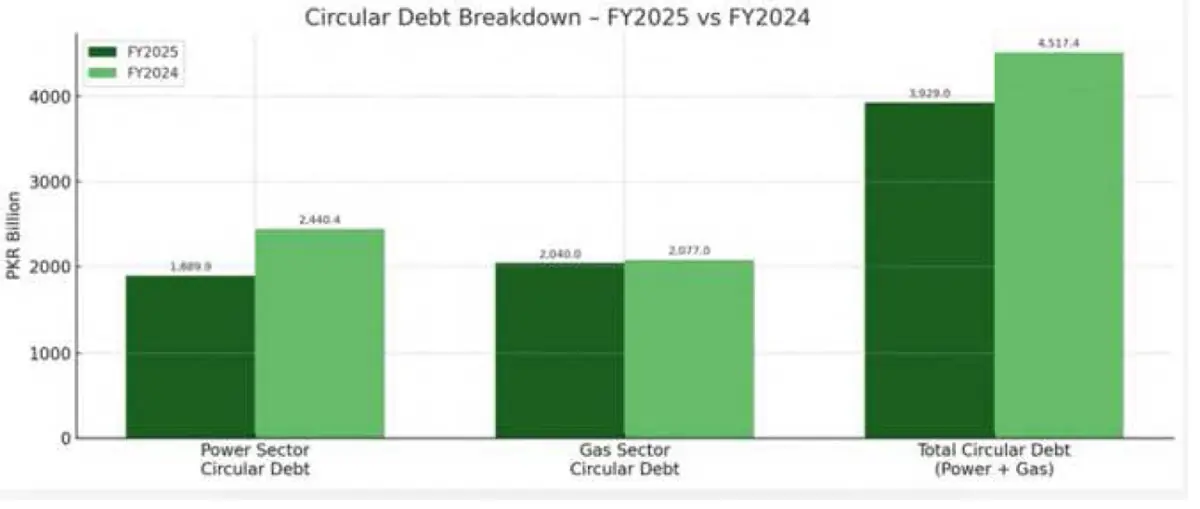

Circular debt remains a central problem. In the power sector, the stock has fallen to Rs 3.9 trillion, but mainly because of equity injections and accounting adjustments — not because underlying issues have been fixed.

Low recovery rates, technical losses, and theft continue to generate fresh debt. In the gas sector, circular debt remains high at Rs 2.04 trillion, largely sitting with Sui Northern Gas Pipelines Limited and Sui Southern Gas Company. Pricing distortions and operational inefficiencies keep the pressure on.

Governance remains a core challenge. Boards often lack technical depth, leadership changes are frequent, and many SOEs do not complete audits on time. Pension liabilities — now above Rs 2 trillion — add another long-term burden. Privatization efforts struggle because balance sheets are weighed down by legacy debt and unresolved liabilities.

The report outlines sensible solutions: better billing and recovery systems, automated tariff adjustments, digital metering to reduce theft, and stronger financial discipline. But Pakistan has long understood the problems. The harder task is consistent execution.

FY25 confirms that the SOE sector is not just underperforming — it is placing a growing strain on public finances. Without structural reform, recapitalization will continue to shift losses onto the balance sheet.

The numbers are technical, but the message is simple: reform cannot be postponed indefinitely.

Comments