Khyber Tobacco Company (PSX: KHTC) was incorporated in Pakistan as a public limited company in 1954. The company manufactures and sells cigarettes besides re-drying of tobacco.

The company also has filter rods and other non-tobacco materials in its portfolio.

KHTC has a strong market presence in Pakistan and it has also expanded its distribution network in Eastern Europe, South & West Africa, Central & South Asia and Middle East.

Pattern of Shareholding

As of June 30, 2025, KHTC has a total of 6.92 million shares outstanding which are held by 1234 shareholders. Local general public has the majority stake of 94.28 percent in KHTC, followed by Insurance companies holding 3.46 percent shares of the company.

Around 0.98 percent of the company’s shares are held by the government sector. The remaining ownership is distributed among other categories of shareholders.

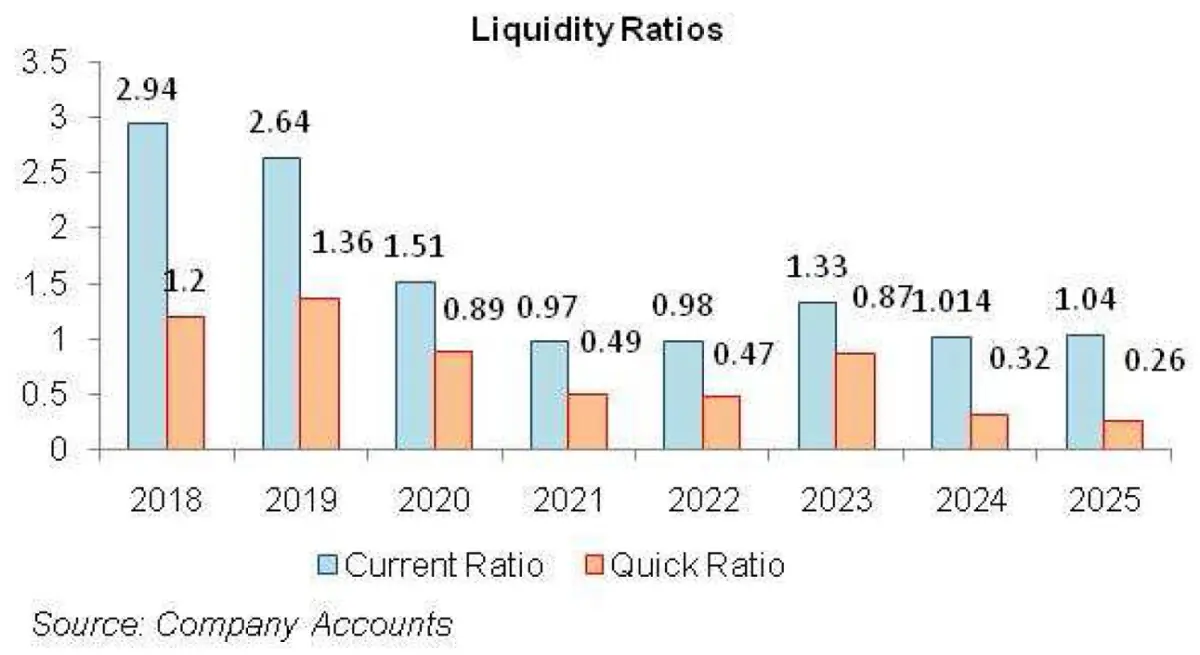

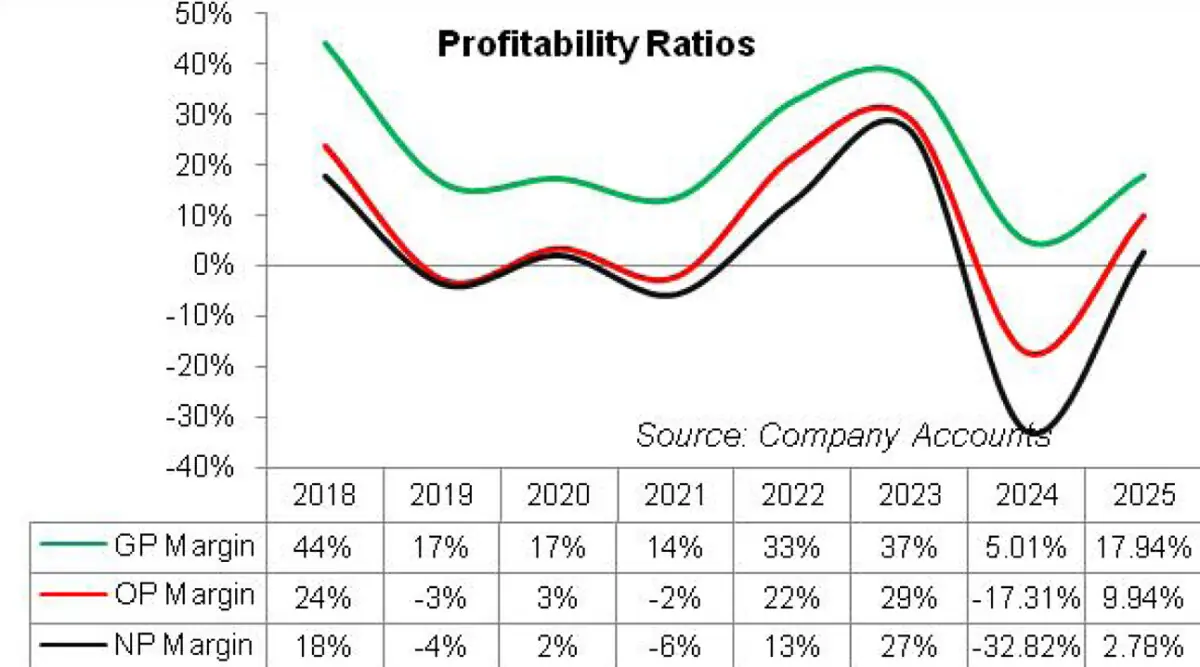

Historical Performance (2019-25)

Over the period under consideration, KHTC’s topline plunged thrice i.e. in 2019, 2021 and 2024. These were also the years where the company posted a negative bottomline. The remaining years are characterized by staggering topline and bottomline growth. The margins of the company witnessed a drastic slump in 2019 followed by some recovery in 2020.

However, in 2021, the margins dwindled yet again. The subsequent two years marked the period of financial vividness and exuberance for KHTC where it illustrated staggering recovery in its margins. In 2024, KHTC’s margins portrayed their lowest ever values. This was followed by a rebound in 2025 (see the graphs of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, KHTC’s net sales slumped by 4.93 percent year-on-year to clock in at Rs.1070.17 million. While export sales boasted an astounding growth of over 42 times to clock in at Rs.235.76 million, local sales nosedived by 16 percent year-on-year to clock in at Rs2102 million.

The drop in net sales came on the back of low volumetric sales in the cut tobacco and cigarette categories while off-take of re-dried tobacco grew to 1.42 million kilograms in 2019 compared to 0.166 million kilograms in 2018, up 754 percent year-on-year (see the table of sales volume).

Cost of sales expanded by 41.50 percent in 2019 which not only lowered the gross profit by 64.12 percent in 2019 but also squeezed the GP margin to 16.59 percent in 2019 from GP margin of 43.96 percent in the previous year. Administrative expense slid by 25.94 percent year-on-year in 2019 mainly on account of lesser trade debts written off during the year and lower rent expense.

Conversely, distribution expense grew by 32.92 percent year-on-year on 2019 due to extensive marketing of re-dried tobacco, custom, clearance and freight on export sales as well as training of sales staff. This culminated into operating loss of Rs.29.47 million in 2019 versus operating profit of Rs.268.47 million posted in 2018.

Finance cost surged by 381.92 percent in 2019 owing to higher discount rate coupled with increased borrowing to meet working capital requirements.

As a consequence, KHTC posted net loss of Rs.38.27 million in 2019 versus net profit of Rs.199.87 million registered in the previous year. The company recorded loss per share of Rs.7.96 in 2019 versus EPS of Rs.41.57 recorded in 2018.

In 2020, KHTC registered year-on-year topline growth of 70.88 percent which took its net sales to Rs.1828.70 million. This came on the back of higher off-take in all three categories i.e. re-dried tobacco; cut tobacco and cigarette (see the table of sales volume). Both local and export sales boasted a massive turnaround in 2020 despite the eruption of COVID-19.

GP margin increased to 17.39 percent in 2020 with gross profit strengthening by 79.12 percent in absolute terms. Administrative expense hiked by 13.20 percent year-on-year in 2020 mainly on account of higher payroll expense.

Distribution expense also escalated by 21.36 percent year-on-year in 2020 due to higher custom, clearance & freight on export and training of sales staff during the year. This translated into operating profit of Rs. 62.74 million in 2020 and OP margin of 3.43 percent.

Finance cost slid by 56.83 percent in 2020. KHTC registered net profit of Rs.38.54 million in 2020 with NP margin of 2.11 percent and EPS of Rs.8.02.

KHTC’s topline once again took a hit in 2021 and dropped by 33.5 percent year-on-year to clock in at Rs.1216.04 million. This was on the back of a massive drop in the off-take of re-dried tobacco.

The dispatches of other two categories marginally increased but couldn’t create any impact on the topline (see the table of sales volume). Export sales also registered over 50 percent dip in 2021 due to low demand of Pakistani tobacco in the international market.

Cost of sales nosedived by 30.38 percent year-on-year in 2021 resulting in 48.32 percent thinner gross profit in 2021. GP margin shrank to 13.52 percent in 2021.

Lesser export sales saved the company from customs, clearance and freight on export. This coupled with lower advertisement and promotion activities resulted in 46.21 percent year-on-year dip in the distribution expense in 2021. Administrative expenses also slipped by 7.68 percent year-on-year in 2021. Despite keeping the operating expenses in check, KHTC posted an operating loss worth Rs26.93 million in 2021.

Finance cost spiked by 171.62 percent year-on-year in 2021 despite low discount rate during the year. This was the result of a massive hike in current liabilities during the year. This produced a major dent on the bottomline and resulted in net loss of Rs68.65 million in 2021 with loss per share of Rs.14.28.

KHTC posted a staggering 102.68 percent year-on-year growth in its topline which clocked in at Rs.2464.71 million in 2022. This came on the back of increase in off-take across categories particularly re-dried tobacco (see the table of sales volume). The company also undertook rigorous marketing initiatives during the year which boosted its export sales.

The depreciation of Pak Rupee also played its part in keeping the net sales robust. GP margin flew up to 32.55 percent in 2022 while gross profit multiplied by 388.15 percent in absolute terms.

Customs, clearance and freight on export sales expanded the distribution expense by 114.80 percent year-on-year in 2022. Administrative expense grew in line with inflation and also because the workforce grew from 372 employees in 2021 to 460 employees in 2022 which drove up the payroll expense.

KHTC posted operating profit of Rs.532.76 million in 2022 which translated into OP margin of 21.62 percent. Finance cost grew by 140.91 percent in 2022 owing to higher borrowings and record high discount rate during the year. The net profit stood at Rs.315.45 million in 2022 culminating into NP margin of 12.80 percent and EPS of Rs.65.62.

In 2023, KHTC registered a splendid 201.64 percent year-on-year growth in net sales which clocked in at Rs.7434.55 million. This was the result of a staggering increase in sales volume across categories (see the table of sales volume).

Export sales registered a whopping increase over 400 percent and stood at 55 percent of KHTC’s gross sales in 2023 versus its share of 27.6 percent in 2022. Higher proportion of export sales also buttressed the GP margin amid Pak Rupee depreciation.

KHTC’s GP margin climbed to 37.28 percent in 2023. Administrative expense hiked by 58.91 percent year-on-year in 2023 mainly on account of higher payroll expense as the number of employees grew to 598 in 2023. Distribution expense surged by 149.25 percent in 2023 primarily due to higher custom, clearance and freight on export sales.

Research expense and promotion expense also spiked in 2023. There was a significant rise in impairment loss on trade debts in 2023 which clocked in at Rs.61.96 million, up over 2245 percent year-on-year.

Operating profit widened by 309 percent in 2023 with OP margin rising up to 29.32 percent. Other expense escalated by 483.83 percent in 2023 on account of increased profit related provisioning, FED and sales tax written off during the year. However, other expense was absorbed by other income which grew by 940.33 percent in 2023 on account of robust exchange gain.

Finance cost mounted by 112.30 percent in 2023 on account of higher discount rate although borrowings notably dived down in 2023. The company posted 533.50 percent year-on-year growth in its net profit which stood at an unprecedented level of Rs.1998.40 million in 2023 with EPS of Rs.288.68 and NP margin of 26.88 percent – the highest among all the years under consideration.

KHTC’s net sales slumped by 58.12 percent to clock in at Rs.3113.76 million in 2024. This was on account of a massive decline in sales volumes across categories. Both local and export sales declined during the year.

KHTC made no sales to African and European region in 2024 and sales to Middle East region also enormously deteriorated. Out of the total capacity of 9288 million cigarettes, the company utilized 6.8 percent capacity in 2024 and produced 631 million cigarettes. This was in line with lackluster demand.

KHTC’s capacity utilization was recorded at 10 percent in 2023. Cost of sales dropped by 36.57 percent in 2024 resulting in 94.37 percent thinner gross profit recorded during the year. GP margin also drastically fell to its lowest level of 5 percent in 2024.

Administrative expense heightened by 43.37 percent in 2024 mainly on account of higher payroll as well as fuel & power expense incurred during the year. Distribution expense went down by 29.63 percent in 2024 due to lower custom, clearance and freight charges on account of petite sales volume.

KHTC recorded operating loss of Rs.467.94 million in 2024. Other income eroded by 99.19 percent in 2024 due to absence of exchange gain as well as lesser written back of accrued liabilities. Other expense surged by 34.35 percent in 2024 due to higher sales tax/ FED written off during the year.

Despite high discount rate, finance cost ticked down by 2.41 percent in 2024 due to lower interest paid on loans by sponsors. This was regardless of the fact that outstanding loan from sponsors massively grew from Rs.101.036 million in 2023 to Rs.901.036 million in 2024. The company recorded net loss of Rs.1021.997 million in 2024 with loss per share of Rs.147.63.

In 2025, KHTC posted a staggering year-on-year growth of 217.65 percent in its topline which recorded the highest ever level of Rs.9890.70 million. This came on the back of increase in all sales volume of all the categories of products (see the graph of sales volume). Both local and export sales posted significant improvement during the year.

Besides Asia, KHTC also exported to Europe, Africa and North America in 2025. In line with the increased demand, production also rose. This resulted in capacity utilization of 16.39 percent versus capacity utilization of 6.79 percent recorded in the previous year.

Cost of sales mounted by 174.39 percent in 2025. The growth in cost was considerably low when compared to topline growth.

This was due to rigorous cost control measures implemented by the company, robust sales volume and upward price revision.

KHTC recorded 1037.89 percent higher gross profit in 2025 with GP margin climbing up to 17.94 percent. Administrative expense ticked up by only 6.55 percent in 2025 mainly on the back of payroll expense.

This was despite the fact that the company streamlined its workforce from 595 employees in 2024 to 575 employees in 2025.

Distribution expense escalated by 57.31 percent in 2025 particularly due to higher freight charges as well as custom & clearance charges incurred during the year due to increased sales volume. Impairment loss on financial assets surged by 34.56 percent in 2025.

KHTC posted operating profit of Rs.983.575 million in 2025 with OP margin of 9.94 percent. Other income recorded a phenomenal growth of 538.21 percent in 2025 due to exchange gain, rental income and scrap sales.

However, it was wiped off by 9.35 percent bigger other expense incurred in 2025 on account of provisioning done for WWF, WPPF, and higher advances written off during the year as well as sales tax written off during the year.

Finance cost multiplied by 21.74 percent in 2025 despite monetary easing. This was due to increased borrowings from sponsors. KHTC posted net profit of Rs.274.648 million in 2025. This translated into EPS of Rs.39.67 and NP margin of 2.78 percent in 2025.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, KHTC recorded 27.21 percent improvement in its net sales which clocked in at Rs.1581.64 million. Gross local sales posted a drastic decline of 58.88 percent to clock in at Rs. 1797.433 million during the period.

Conversely, export sales (gross) mounted by 315.13 percent to clock in at Rs.1206.118 million in 1QFY26. Export sales grabbed 40.16 percent of the gross turnover of the company in 1QFY26 versus its share of 6.23 percent in 1QFY25. Changes in sales mix, better pricing and cost management allowed KHTC to record gross profit of Rs.263.46 million in 1QFY26 versus gross loss of Rs.341.45 million recorded in 1QFY25.

GP margin clocked in at 16.66 percent in 1QFY26. Increase in the minimum wage rate resulted in 16.94 percent escalation in administrative expense in 1QFY26. Conversely, distribution expense tumbled by 34.69 percent during the period seemingly due to lower sales volume in the local market. KHTC posted other income of Rs.16.03 million in 1QFY26 versus no other income posted in 1QFY25.

This might be due to exchange gain on the back of improved export sales. Operating profit clocked in at Rs.82.40 million in 1QFY26 versus operating loss of Rs.523.47 million posted in 1QFY25. OP margin was recorded at 5.21 percent in 1QFY26.

Finance cost ticked up by 4.51 percent in 1QFY26 despite monetary easing. This was on the back of increased outstanding liabilities which largely comprised of loan from directors. KHTC registered net profit of Rs.36.97 million in 1QFY26 with EPS of Rs.5.34 and NP margin of 2.34 percent. This was against the net loss of Rs.813.03 million and loss per share of Rs.117.45 recorded in 1QFY25.

Future Outlook

The complete implementation of Track & Trace system is likely to result in increase in local sales. The company is planning to further expand its footprint in the local and international market particularly in the category of re-dried tobacco.

Comments