Al-Ghazi Tractors Limited (PSX: AGTL) was incorporated in Pakistan as a public limited company in June, 1983. AGTL is a subsidiary of Al-Futtaim Group of Dubai.

The company is engaged in the business of providing agricultural solutions by manufacturing and selling tractors, generators, implements and spare parts. Its operational hub is located in Dera Ghazi Khan which has technical collaboration with Case New Holland (CNH), the largest manufacturer of agricultural tractors in the world.

Pattern of Shareholding

As of December 31, 2024, AGTL has 57.964 million shares outstanding shares which are held 2801 shareholders. Associated companies, undertakings and related parties which include Al-Futtaim Industries Company (LLC) and CNH Industrial N.V. hold 50.02 and 43.17 percent shares of AGTL respectively.

These are followed by local general public accounting for 5.10 percent shares of the company. The remaining shares are held by other categories of shareholders.

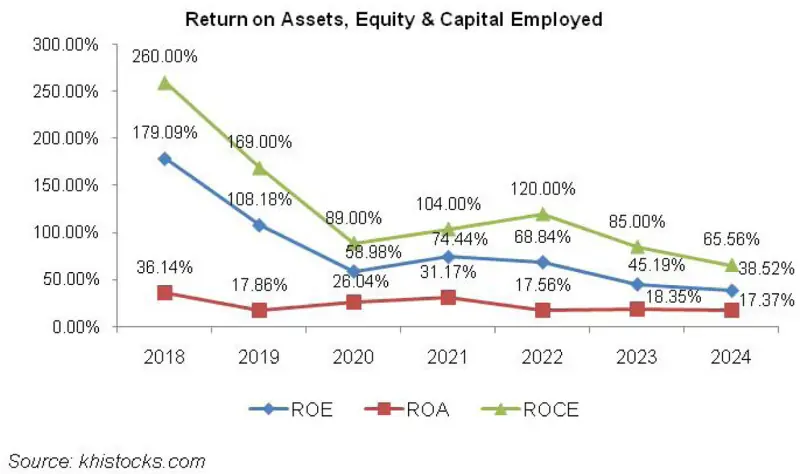

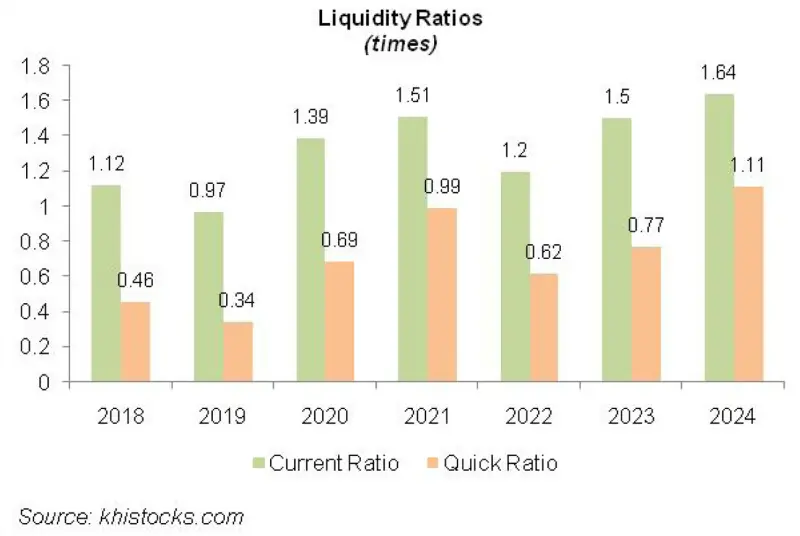

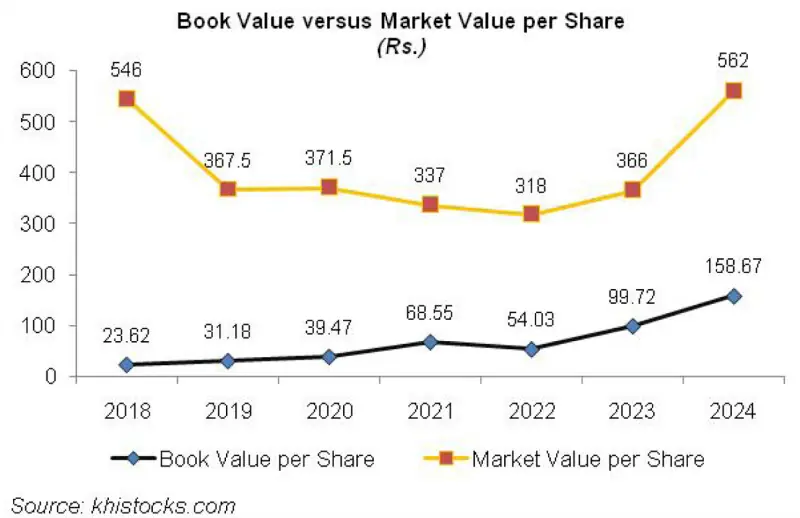

Historical Performance (2019-2024)

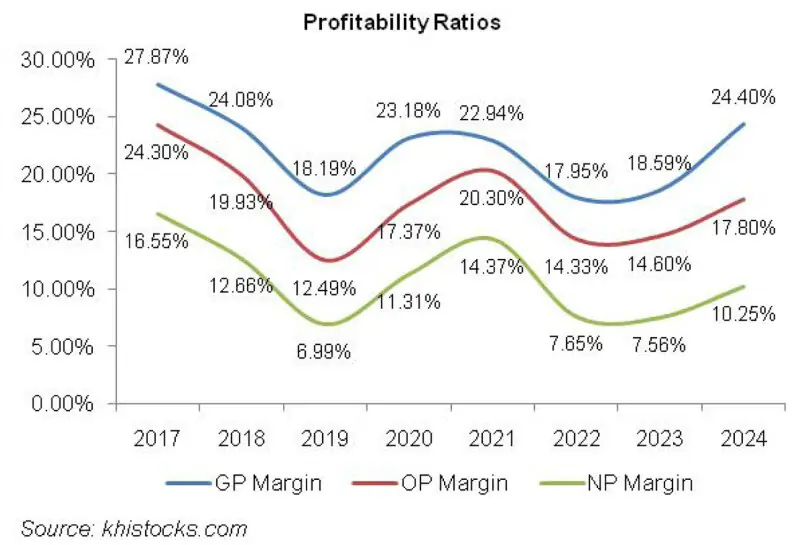

During the period under consideration, AGTL’s topline slid in 2019 and 2020. Its bottomline posted decline in 2019 and 2022. The company’s margins which drastically fell in 2019 recorded a staggering rebound in 2020.

In 2021, gross margin slightly fell while operating and net margins continued to expand notably. In 2022, AGTL’s margins considerably plunged followed by 2023 where gross and operating margins picked up while net margin ticked down. In 2024, all the margins registered considerable improvement.

The detailed performance review of the period under consideration is given below.

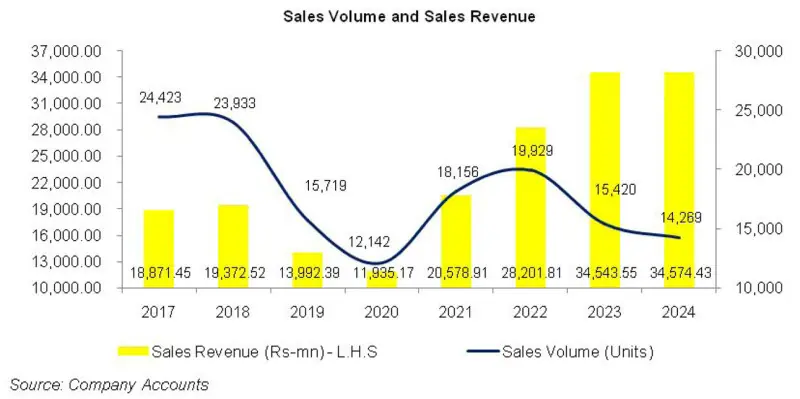

In 2019, AGTL sold 15,719 tractors which were 34 percent less than what it sold in 2018 (see the graph of sales volume and sales revenue). This resulted in 27.77 percent year-on-year drop in net sales of the company which clocked in at Rs.13,992.388 million in 2019. Low sales volume was attributable to persistent economic slowdown coupled with worsening water crisis which affected farmers’ economic health.

Moreover depreciation of Pak Rupee, heightened prices of raw materials and high conversion cost culminated into higher pricing rendering AGTL’s products unaffordable for the farmer community in the absence of any significant support scheme by the government.

Low off-take coupled with high cost of production took its toll on the margins of the company. GP margin clocked in at 18.19 percent in 2019 as against GP margin of 24.10 percent recorded in 2018. In absolute terms, gross profit dwindled by 45.56 percent in 2019.

Distribution and administrative expenses dropped by 4.70 percent and 2.84 percent respectively in 2019 due to lower plant operations and curtailed sales volume.

The company also undertook lesser advertisement and sales promotion activities in 2019. Other income dipped by 0.77 percent in 2019 due to lower return on bank deposits. While the company booked considerably lesser provisioning for WWF and WPPF, elevated provisioning for slow moving and obsolete inventories resulted in 4.86 percent uptick in other expense in 2019.

AGTL recorded 54.75 percent year-on-year slump in its operating profit in 2019. OP margin dipped to 12.50 percent in 2019 vis-à-vis OP margin of 19.93 percent posted in the previous year.

Finance cost gave another major blow to the bottomline as it surged by 217.33 percent in 2019 owing to higher interest rate and increased bank borrowings.

AGTL increased the utilization of overdraft facilities during the year to sustain its operational activities amidst low sales and depressed liquidity.

The bottomline nosedived by a massive 60.14 percent year-on-year in 2019 to clock in at Rs.977.652 million with EPS of Rs. 16.87 versus EPS of Rs. 42.31 percent recorded in 2019. NP margin also nosedived from 12.66 percent in 2018 to 7 percent in 2019.

While the company was still grieving over its performance in 2019, the global pandemic hit in 2020, further crippling the economy. The topline further shrank by 14.7 percent year-on-year to clock in at Rs.11,935.172 million.

AGTL could only sell 12,142 tractors during the year which was 22.7 percent lesser than the sales volume recorded in 2019.

This was the consequence of economic downturn amidst COVID-19 coupled with low purchasing power of the farmer community.

AGTL increased the prices of its tractors to absorb the cost shocks. This resulted in 8.70 percent uptick in AGTL’s gross profit in 2020 with its GP margin of recovering from the trough it saw in 2019 to clock in at 23.18 percent.

Lower sales volume helped the company record 15.93 percent year-on-year plunge in its distribution expense in 2020.

Conversely, administrative expense grew by 8.73 percent in 2020 due to inflationary pressure. This was despite the fact that AGTL streamlined its workforce from 436 employees in 2019 to 402 employees in 2020.

Other income declined by 4.27 percent in 2020 due to lower scrap sales. Other expense also tapered off by 30.80 percent in 2020 due to lower provisioning done for WWF, WPPF and obsolete and slow moving inventory.

AGTL’s operating profit strengthened by 18.70 percent in 2020 while its OP margin climbed up to 17.37 percent.

The company overcame the liquidity crunch it experienced in the previous year through efficient equity management. This coupled with low discount rate reduced the finance cost for the company by 63.41 percent in 2020 and helped the bottomline grow by 38 percent year-on-year to clock in at Rs.1349.657 million with EPS of Rs.23.28 and NP margin of 11.31 percent.

2021 proved to be a buoyant year for AGTL where its sales volume grew by a whopping 49.5 percent year-on-year to clock in at 18,156 units. This resulted in 72.42 percent higher net sales to the tune of Rs.20,578.906 million in 2021. There were multiple factors behind this jaw-dropping growth in topline.

Firstly, the economy was showing the signs of recovery post pandemic. Secondly, the farmers had enough liquidity available due to government support initiatives.

Moreover, satisfactory water availability also resulted in encouraging performance of the agriculture sector which created a ripple effect for the related industries such as tractors, fertilizers etc. High sales volumes and better pricing couldn’t fully offset the high cost of sales and GP margin for the year dipped slightly to clock in at 22.94 percent.

In absolute terms, gross profit picked up by 70.69 percent in 2021. The company was able to contain its distribution cost by 45.64 percent in 2021 despite high sales. This was due to considerably lower warranty expense and freight charge reversal of Rs.10.945 million in 2021 versus freight expense of Rs.61.417 million in 2020. Administrative expense surged by 9.66 percent in 2021. This was due to higher fee & subscription charges as well as elevated legal & professional charges incurred during the year which offset the impact of lower payroll expense.

AGTL further cut down its workforce to 393 employees in 2021.

Another positive development during the year was 148.40 percent year-on-year rise in other income which came on the back of higher return on deposit and other accounts as well as scrap sales.

Other expense inched up by 3.77 percent in 2021 due to considerably higher profit related provisioning, the impact of which was partially offset by reversal booked on slow moving and obsolete inventory.

AGTL’s operating profit enhanced by 101.50 percent in 2021. OP margin also significantly improved in 2021 to stand at 20.30 percent. Finance cost dropped by 94 percent year-on-year in 2021 owing to low discount rate.

The company believed that the financial cost would have dropped further, had the authorities released the sales tax refund amounting to Rs. 2.99 billion which was creating liquidity crunch for the company and compelling it to knock the doors of external creditors.

Net profit grew by 119.16 percent to clock in at Rs.2957.862 million in 2021 with EPS of Rs.51.03 and NP margin of 14.37 percent.

AGTL’s topline continued to impress in 2022 with its market share clocking in at 45 percent versus market share of 32 percent in 2021. With the sale of 19,929 tractors – up 9.77 percent year-on-year - the topline of AGTL grew by 37 percent year-on-year to clock in at Rs.28,201.812 million in 2022. This was despite the fact that the agricultural sector was under extreme stress during the year due to severe floods in the 2HCY22.

Currency depreciation, high prices of raw material, elevated indigenous inflation and energy tariff resulted in 45.93 percent spike in cost of sales in 2022.

This resulted in a paltry 7.21 percent uptick in gross profit in 2022. GP margin of the company shrank to 17.95 percent in 2022. Massive increase of 167.71 percent in the distribution cost was the result of higher salaries of sales force, provision booked against doubtful receivables, advertising & promotion expense and warranty expense incurred during the year.

Administrative expense also escalated by 51.68 percent in 2022 primarily due to elevated payroll expense despite the fact that number of employees stood intact at 393. Other income expanded by 26.40 percent in 2022 due to higher income on bank deposits as well as scrap sales recorded during the year.

The impact of other income was conveniently offset by 61.17 percent higher other expense recorded in 2022. This was due to provision booked for slow moving and obsolete inventory in 2022.

AGTL recorded 3.29 percent downtick in its operating profit in 2022 with OP margin falling down to 14.33 percent. Finance cost also jolted AGTL’s bottomline in 2022 not only because of several hikes in the discount rate but also because of increase in short-term borrowings.

AGTL’s recorded finance cost of Rs.245.035 million in 2022 which was 2699.12 percent higher than the finance cost recorded in 2021. The imposition of super tax was another whammy for AGTL’s bottomline which shrank by 27.11 percent year-on-year to clock in at Rs.2156.044 million in 2022 with EPS of Rs.37.20 and NP margin of 7.65 percent.

In 2023, AGTL’s net sales grew by 22.49 percent to clock in at Rs.34,543.545 million. The company’s sales volume stood at 15,420 units - down 22.63 percent year-on-year. This indicates that the topline growth was due to upward price revision.

High level of political and economic instability not only took its toll on the purchasing power of consumers but also halted the production activities of the companies due to intermittent restrictions on the import of essential raw materials and machinery.

The company’s market share fell to 36 percent in 2023. Cost of sales grew by 21.52 percent in 2023, however, with price escalation; AGTL was able to record 26.90 percent higher gross profit in 2023 with GP margin jumping up to 18.59 percent.

Distribution expense mounted by 32.98 percent in 2023 due to higher salaries expense, advertising and promotion, freight and after sales expenses incurred during the year.

101.30 percent higher administrative expense incurred during the year was the result of elevated payroll expense, depreciation expense, vehicle running & maintenance charges, fee & subscription charges specifically paid for cloud & related services as well as transformation & consultancy charges paid for quality & standards improvement.

During the year, the company also increased its headcount to 410 employees. Other income magnified by 203.39 percent in 2023 particularly due to higher return on bank deposits. Other expense soared by 24.43 percent in 2023 due to higher provisioning done for WWF, WPPF and slow moving and obsolete inventory.

AGTL recorded 24.81 percent higher operating profit in 2023 with OP margin slightly ticking up to clock in at 14.60 percent. Finance cost enlarged by 45.45 percent in 2023 due to higher discount rate. Net profit improved by 21.14 percent to clock in at Rs.2611.772 million in 2023 with EPS of Rs.45.06 and NP margin of 7.56 percent.

In 2024, AGTL posted a paltry 0.09 percent uptick in its net sales which clocked in at Rs.35,574.43 million. Sales volume went down by 7.46 percent to clock in at 14,269 units in 2024. This implies that upward revision in the prices of tractors kept AGTL’s topline afloat in 2024.

While the local economy showed signs of improvement in 2024 characterized by decline in inflation and discount rate and stability of local currency. Conversely, the tractor industry couldn’t do well because of wheat price crisis which took its toll on the farmers’ liquidity and also because of imposition of 10 percent sales tax on tractors as per the Finance Act, 2024.

The farmer community also delayed their purchase decision in anticipation of government’s green tractor scheme which was launched in November and December. Lower sales and production volume enabled AGTL to record 7 percent downtick in its cost which resulted in 31.32 percent higher gross profit in 2024. GP margin attained its optimum level of 24.40 percent in 2024.

Distribution expense mounted by 87.39 percent in 2024 due to the launch of a new tractor, NH850 during the year and also because of provisioning done for doubtful receivables.

Administrative expense surged by 35.74 percent in 2024 due to increased fee & subscription charges particularly in respect of cloud & related services. Other income deteriorated by 43.65 percent in 2024 due to thinner income on bank deposits owing to monetary easing. Other expense slid by 24.73 percent in 2024 due to reversal of provision booked on slow-moving and obsolete inventory.

AGTL recorded 22 percent stronger operating profit in 2024 with OP margin jumping up to 17.80 percent – the highest level achieved since 2019. Finance cost soared by 25.36 percent in 2024 due to increased short-term financing. Net profit picked up by 35.63 percent to clock in at Rs.3542.275 million in 2024 with EPS of Rs.61.11 and NP margin of 10.25 percent.

Recent Performance (9MCY25)

AGTL’s net sales drastically weakened by 59 percent to clock in at Rs.9760.75 million in 9MCY25. This was due to poor farm economics on account of recent floods which badly affected the agricultural regions of Punjab and Sindh.

The Punjab government launched its green tractor scheme towards the end of the year, the impact of which will be visible in the last quarter results of CY25. During the 9-month period under review, AGTL sold 4126 tractors, down 57.11 percent year-on-year.

Cost of sales dipped by 55.71 percent in 9MCY25 due to curtailed operations and sales volume. Gross profit tumbled by 69.98 percent in 9MCY25 with GP margin clocking in at 17.71 percent versus GP margin of 23.92 percent recorded in 9MCY24.

Distribution expense ticked up by a paltry 2.27 percent in 9MCY25 while administrative expense recorded 19.55 percent surge during the period. Lower profit on bank deposits appear to be the cause of 57.72 percent thinner other income in 9MCY25.

Other expense also fell by 64.85 percent in 9MCY25 probably due to lower profit related provisioning done during the period. AGTL also booked Rs.129.86 million provision for ECL in 9MCY25. All these factors translated into operating loss of Rs.157.72 million in 9MCY25. Finance cost nosedived by 7 percent during the period under review due to monetary easing.

The company registered net loss of Rs.269.78 million in 9MCY25 with loss per share of Rs.4.65. This was against net profit of Rs.2368.922 million and EPS of Rs.40.87 posted in 9MCY24.

Future Outlook

Near-term stabilization in economy and a downtick in discount rate may bode well for the auto industry volumes in the coming months. The company is optimistic on its sales volume on the back of Green tractor scheme announced by the Punjab Government.

AGTL successfully secured 3728 units which represented 35 percent of the 9500 tractors allocated under Phase I of the scheme. Phase II of the scheme with 10,000 tractors is yet to be rolled out. On the flipside, the export operations of the company are vulnerable owing to conflicts at the Western border.

Comments

Comments are closed for this article.