International Packaging Films Limited: performance and outlook

International Packaging Films Limited was established in Pakistan as a Greenfield project in 2015 to manufacture Biaxially Oriented Polypropylene (BOPP) films. Initially the company was incorporated as a private limited company in 2015 and was later converted into public limited company in 2021.

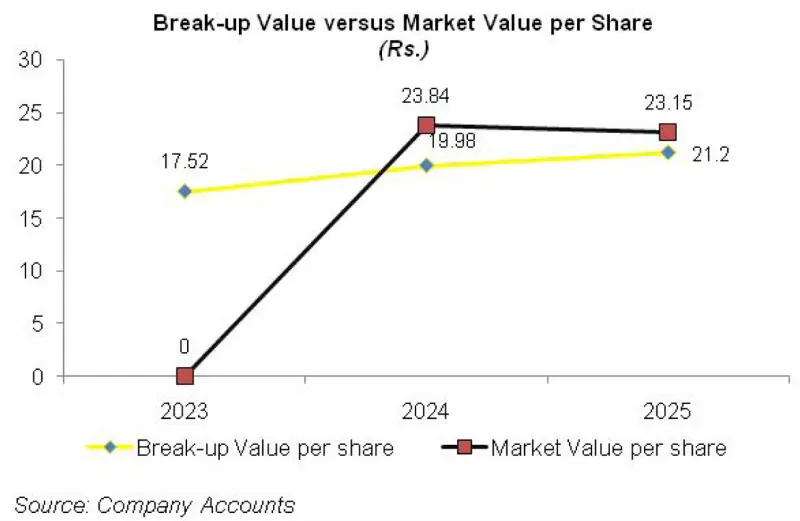

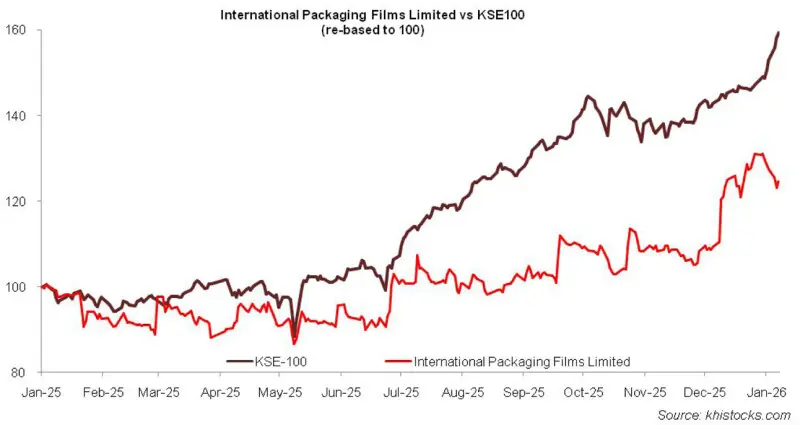

The company got listed on the Pakistan Stock Exchange in June 2024. The company is engaged in the manufacturing and sale of BOPP, CPP and BOPET films for both domestic and international markets.

Pattern of Shareholding

As of June 30, 2025, IPAK has a total of 700.200 million shares outstanding which are held by 1523 shareholders. Directors, CEO, their spouse and minor children have the majority stake of 41.52 percent in the company followed by associated companies, undertakings and related parties holding 38.71 percent shares.

Local general public accounts for 14.77 percent shares of IPAK. The remaining ownership is distributed among other categories of shareholders.

Historical Performance (2024-25)

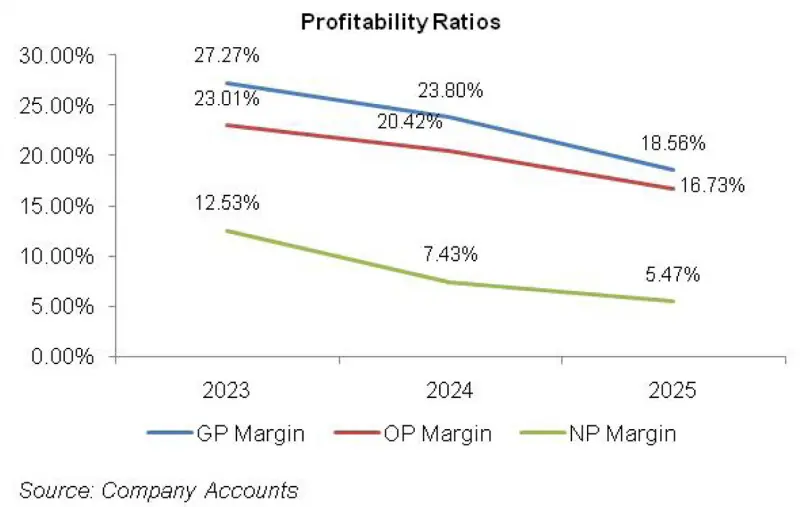

IPAK’s topline inched up in 2024 however bounced back in the succeeding year. Its bottomline registered decline in both the years.

The company’s margins also followed a downward trajectory from 2023 to 2025. The detailed performance review of the period under consideration is given below.

In 2024, IPAK’s topline posted 2.84 percent year-on-year growth to clock in at Rs.17088.89 million. This came on the back of a massive rise in export sales of the company particularly to Asia and Europe. After tremendous growth, export sales comprised of 11 percent of IPAK’s sales mix in 2024 versus its share of 0.514 percent recorded in the previous year.

Local sales which constituted the major chunk of IPAK’s sales mix greatly offset the impact of robust export sales in 2024, resulting in a marginal topline growth. Cost of sales mounted by 7.74 percent in 2024 which resulted in 10.23 percent lower gross profit and GP margin clocking in at 23.80 percent in 2024 versus GP margin of 27.27 percent recorded in the previous year.

Decline in GP margin was due to high-base effect as the company recognized inventory gain from excess inventory level in 2023.

Marketing expense surged by 26.31 percent in 2024 particularly on the back of export charges, outward freight as well as travelling & conveyance charges incurred during the year. Administrative expense mounted by 20.51 percent in 2024 due to higher payroll expense, travelling & conveyance charges and license fee incurred during the year.

IPAK also expanded its workforce from 351 employees in 2023 to 395 employees in 2024. Other expense dipped by 24.43 percent in 2024 due to lower provisioning done for WWF and WPPF. Lesser provisioning offset the impact of exchange loss and loss on disposal of fixed assets recorded in 2024.

Other income provided much needed support to the company as it strengthened by 96.49 percent in 2024 due to mark-up income recognized on loan to subsidiary (PETPAK) and export rebate received during the year.

As against loss allowance of Rs.50.782 million recorded on trade receivables in 2023, IPAK recorded reversal of Rs.7.67 million on trade receivables in 2024. All in all, operating profit registered 8.74 percent shrinkage in 2024 with OP margin clocking in at 20.42 percent versus OP margin of 23 percent posted in 2023.

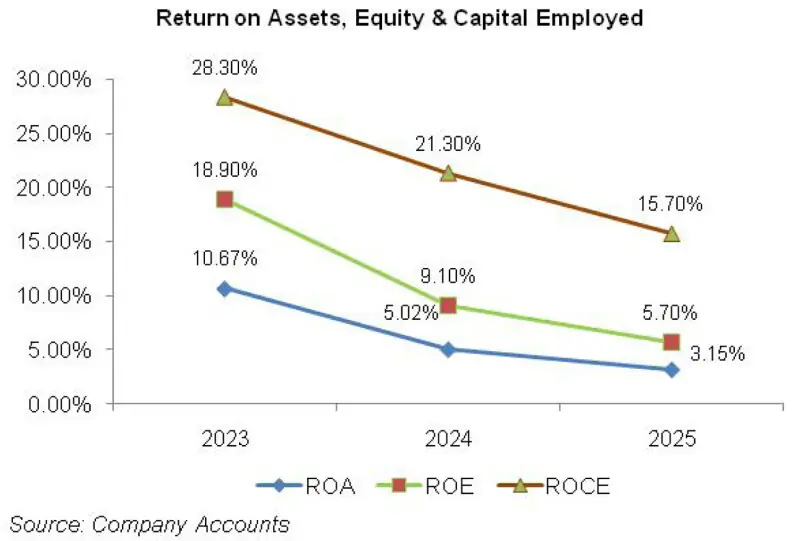

Finance cost spiked by 141,42 percent in 2024 due to monetary tightening and increased borrowings to materialize the expansion plans. This resulted in debt-to-equity ratio of 47.14 percent in 2024 versus 43.08 percent in 2023.

Net profit dwindled by 39 percent to clock in at Rs.1269.464 million in 2024. This culminated into EPS of Rs.2 in 2024 versus EPS of Rs.3.58 recorded in 2023. NP margin also fell from 12.53 percent in 2023 to 7.43 percent in 2024.

In 2025, IPAK registered 8.92 percent decline in its net sales which clocked in at Rs.15564.54 million. The same pattern was repeated in 2025 whereby export sales continued to grow while local sales receded. Export sales stood at 30.47 percent of IPAK’s sales mix in 2025.

Export sales were heavily concentrated in Asia. The company intentionally focused on export markets in 2025 despite its low margins in order to attain long-term growth. GP margin fell to 18.56 percent in 2025 due to change in sales mix. Marketing expense posted a paltry 2.64 percent uptick in 2025 due to higher salaries of sales force and export charges.

Administrative expense ticked down by 6.28 percent in 2025 due to thinner travelling & conveyance charges as well as lower licensing fee incurred during the year. IPAK further enlarged its workforce to 444 employees in 2025. Other expense dropped by 47.22 percent in 2025 due to lower provisioning done for WWF and WPPF and no exchange loss and loss on disposal of fixed assets recorded during the year.

Other income mounted by 62.25 percent in 2025 due to higher mark-up income on loan to subsidiary company (PETPAK), higher scrap sales, export rebate and exchange gain recognized during the year. IPAK also recorded Rs.19.13 million worth reversal on allowance booked on trade receivables in 2025, up 149.60 percent year-on-year.

Operating profit thinned down by 25.37 percent in 2025 with OP margin falling down to 16.73 percent. Finance cost dipped by 13.50 percent in 2025 despite increased short-term borrowings. This appears to be the result of the onset of monetary easing towards the end of the fiscal year. Debt-to-equity ratio surged to 53.11 percent in 2025. IPAK registered net profit of Rs.850.995 million in 2025, down 32.96 percent year-on-year. This translated into EPS of Rs.1.22 and NP margin of 5.47 percent in 2025.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, IPAK posted 13.966 percent decline in its net sales which clocked in at Rs.2948.08 million. Unlike the previous two years, export sales massively fell in 1QFY26 while local sales ticked up.

While the company still aims to strengthen its footprint in the international market, thinner export sales during the quarter was a transient instance apparently due to geopolitical tensions. High margin local sales resulted in GP margin of 21.77 percent in 1QFY26 versus GP margin of 13.81 percent recorded in 1QFY25.

Marketing expense fell by 51.68 percent in 1QFY26 seemingly due to lower freight charges and export expense on the back of thinner export volumes. Administrative expense also dipped by 20.39 percent in 1QFY26 certainly due to lower travelling & conveyance charges. IPAK recorded net other income of Rs.56.27 million in 1QFY26, down 63 percent year-on-year due to higher other expense seemingly due to increased provisioning done for WWF and WPPF.

Conversely, mark-up income on loan to subsidiary company shrank due to monetary easing. Operating profit grew by 31.66 percent in 1QFY26 with OP margin clocking in at 19.50 percent versus OP margin of 12.75 percent posted in 1QFY25.

Finance cost dipped by 37 percent in 1QFY26 due to lower discount rate and reduced borrowings. Net profit posted phenomenal growth of 818.253 percent in 1QFY26 to clock in at Rs.182.613 million with EPS of Rs.0.26 versus EPS of Rs.0.03 recorded in 1QFY25. NP margin jumped up from 0.58 percent in 1QFY25 to 6.19 percent in 1QFY26.

Future Outlook

Going forward, the company not only aims to mark more profound presence in the export market but also diversify its product mix to come up with specialized and high-barrier films to attain stronger margins. Measures taken to attain cost optimization and operational efficiency will also play a vital role in boosting profitability.

Comments

Comments are closed for this article.