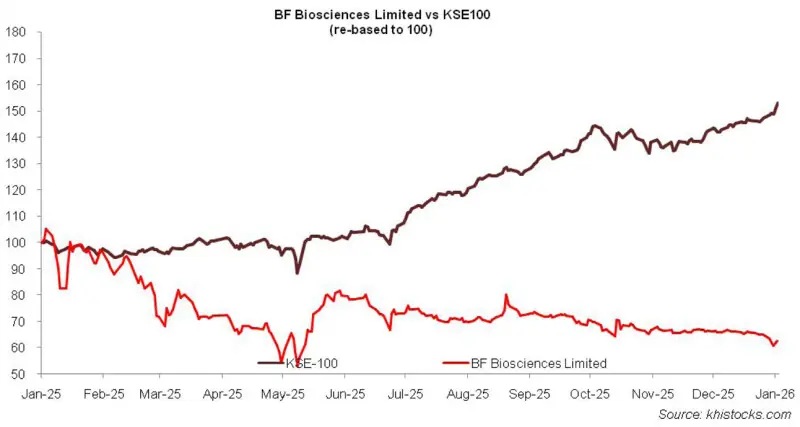

BF Biosciences Limited (PSX: BFBIO) was incorporated in Pakistan as a public unlisted company in 2006. It is a 80/20 joint venture between Ferozsons Laboratories Limited and Bago Group of Argentina. The company is engaged in the import, manufacturing, marketing and distribution of pharmaceutical products.

Pattern of Shareholding

As of June 30, 2025, BFBIO has a total of 88.333 million shares outstanding which are held by 7114 shareholders. Associated companies, undertakings and related parties have the majority stake of 71.70 percent in the company followed by local general public holding 23.51 percent shares.

Around 2.46 percent of the company’s shares are held by other local companies and 1.35 percent by Modarabas & Mutual Funds. The remaining ownership is distributed among other categories of shareholders.

Historical Performance (2024-2025)

BFBIO’s topline and bottomline registered year-on-year growth in 2024 and 2025. The company’s margins which posted reasonable growth in 2024 receded in 2025. The detailed performance review of the period under consideration is given below.

In 2024, BFBIO’s net sales recorded a splendid year-on-year growth of 102.19 percent to clock in at Rs.3658.72 million. During the year, the company’s pre-filled syringes line was fully commissioned with the commencement of commercial production.

Lyophilizer and Combi-filling lines were also commissioned during the year, however, were undergoing internal validation, hence, commercial production was not initiated. While export sales also ticked up during the year, local sales growth was the main driving force behind the robust topline growth posted in 2024.

Local sales also form the largest chunk of the company’s overall sales mix. Further break-up of sales depicted that in-market generic sales grew by 130 percent in 2024 while institutional sales posted 13 percent rise during the year. It is pertinent to note that the company achieved a stupendous topline growth in 2024 on the back of change in its sales mix and superior sales volume.

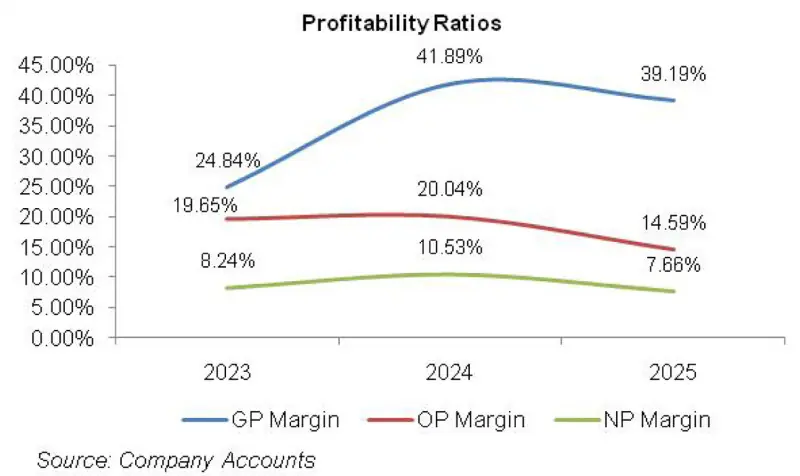

This resulted in lower overhead cost per unit which translated into GP margin of 41.89 percent in 2024 versus GP margin of 24.84 percent recorded in the previous year. In absolute terms, gross profit mounted by 240.91 percent in 2024.

Administrative expense hiked by 73.53 percent in 2024 due to one-off fee payment to increase the paid-up capital. Distribution expense surged by 421.52 percent in 2024 as the company aggressively invested in its field force and promotional activities for the launch of its products.

Other expense mounted by 132.39 percent in 2024 due to higher provisioning done for WWF, WPPF, CRF and ECL. Conversely, other income deteriorated by 76.38 percent during the year due to lesser dividend income and lower realized gain recorded on the sale of short-term investments.

Operating profit strengthened by 106.23 percent in 2024 with OP margin clocking in at 20.04 percent versus OP margin of 19.65 percent recorded in 2023.

Finance cost ticked down by 1.30 percent in 2024 due to lower outstanding liabilities. This resulted in a gearing ratio of 50.90 percent in 2024 versus gearing ratio of 58.30 percent recorded in 2023.

Drop in liabilities was due to the fact that the company had scheduled fund raising via Initial Public Offering. Net profit rose by 158.57 percent to clock in at Rs.385.413 million in 2024. This translated into EPS of Rs.6.09 in 2024 versus EPS of Rs.2.35 recorded in 2023. NP margin improved from 8.24 percent in 2023 to 10.53 percent in 2024.

In 2025, BFBIO posted 59.55 percent spike in its net sales which clocked in at Rs.5837.466 million. During the initial months of 2025, the company conducted IPO and utilized the funds to undertake capital expenditure, acquire international certifications and launch several new products.

During the year, the trading of the company’s shares at the PSX also began. This year, the company’s institutional sales posted 127 percent growth while in-market generic sales grew by 50 percent. While gross profit enhanced by 49.29 percent in 2025, GP margin dipped to 39.19 percent due to higher overhead cost due to commissioning of Line II.

Administrative expense grew by 49.57 percent in 2025 due to higher payroll expense as the company expanded its workforce from 386 employees in 2024 to 535 employees in 2025 in order to operationalize its new plant. Extensive hiring of field force and cutthroat promotional and marketing activities to penetrate the market and launch its products resulted in 101.64 percent higher distribution expense in 2025.

Other expense ticked up by 9.89 percent in 2025 due to higher exchange loss and increased provisioning done for WWF, WPPF and CRF.

Unlike previous year, no provisioning was done for ECL in 2025. Other income posted a phenomenal growth of 528.67 percent in 2025 due to superior dividend income, higher profit on bank deposits, reversal of provisioning done for ECL and higher realized gain on the sale of short-term investments.

BFBIO’s operating profit improved by 16.12 percent in 2025 with OP margin ticking down to 14.59 percent. Finance cost dropped by 15.65 percent in 2025 due to lower outstanding liabilities. This culminated into a gearing ratio of 31.3 percent in 2025. Net profit progressed by 16 percent to clock in at Rs.447.147 million in 2025 with EPS of Rs.5.52 and NP margin of 7.66 percent. Decline in EPS in 2025 was due to an increase in the number of shares from 63.3 million in 2024 to 80.9 million in 2025 due to IPO.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, BFBIO posted 75.44 percent development in its net sales which clocked in at Rs.2432.294 million. This came on the back of 57 percent growth in in-market generic sales and 209 percent growth in institutional sales during 1QFY26.

Higher sales volume, improved sales mix and better capacity utilization resulted in lower overhead cost per unit. This translated into GP margin of 42.69 percent in 1QFY26 versus GP margin of 40.67 percent recorded in 1QFY25. Gross profit posted 84.16 percent enhancement in 1QFY26.

Continuous workforce expansion coupled with inflationary pressure drove administrative expense up by 234.45 percent in 1QFY26. Distribution expense posted 132.62 percent growth during the period due to spreading out of field force and enrichment of marketing and promotional activities.

Other expense dipped by 3.85 percent in 1QFY26 seemingly due to decline in exchange loss. Other income posted a stupendous growth of 1350.83 percent in 1QFY26 apparently due to greater return on short-term investments as the company made tremendous short-term investments during the period and also recorded unrealized gain on the re-measurement of its short-term investments.

Operating profit posted 34.25 percent growth in 1QFY26 with OP margin clocking in at 12.21 percent versus OP margin of 15.96 percent recorded in 1QFY25.

Finance cost dipped by 24.67 percent in 1QFY26 due to monetary easing. Net profit clocked in at Rs.159.521 million in 1QFY26, up 38.38 percent year-on-year. This translated into EPS of Rs.1.81 in 1QFY26 versus EPS of Rs.1.82 recorded in 1QFY25.

The decline in EPS was due to an increase in the number of shares to 88.3 million as of September 30, 2025 due to IPO. NP margin dropped from 8.31 percent in 1QFY25 to 6.56 percent in 1QFY26.

Future Outlook

While the company made great stride in terms of capital expansion, product launches, volumetric growth and topline development, however, the same couldn’t be depicted in its margins due to higher operating expense and hefty factory overheads due to commissioning of new product lines and rigorous promotional drives to achieve market penetration.

The company is expected to absorb these costs with anticipated growth in its sales volume and diversification of its product portfolio.

Comments

Comments are closed for this article.