The history of sovereign insolvency is rarely just about ledger balances; it is a story of the erosion of the state and society itself. In 1881, the Ottoman Empire, crushed by decades of unproductive borrowing and a crumbling revenue base, was forced to sign the Decree of Muharram.

This established the Ottoman Public Debt Administration (OPDA), a foreign-controlled body that directly collected taxes on salt, tobacco, and customs to satisfy European creditors. The OPDA became a “state within a state,” stabilizing the currency while hollowly presiding over the death of Ottoman sovereignty.

Today, Pakistan finds itself navigating a modern, technocratic iteration of this historical trap. While we lack a formal OPDA building in Islamabad, the functional reality of our current engagement with the International Monetary Fund is increasingly indistinguishable from nineteenth-century debt administrations. To avoid a catastrophic default, a crisis that would undoubtedly shatter the social fabric, the country has traded its long-term developmental agency for short-term liquidity. But in doing so, the “cure” prescribed is not only failing to heal the patient; it is systematically dismantling the country’s future growth prospects, entrenching a new era of economic decline.

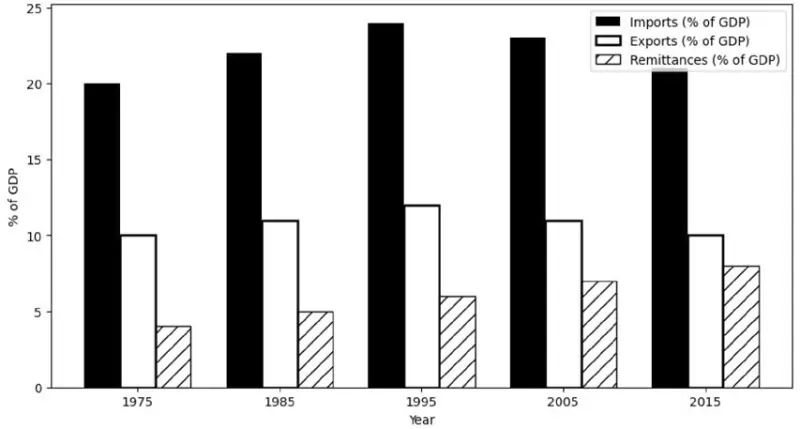

There is little disagreement on the diagnosis. Pakistan suffers from a chronic twin deficit: a fiscal gap (spending more than we collect) and a balance of payments crisis (consuming more foreign exchange than we earn). For fifty years, our imports have hovered at double the rate of our exports as a percentage of GDP. Simply, Pakistan is a country that has failed to produce.

There is broad consensus on failure of Pakistan’s economic model. Decades of stopgap measures, sector-specific exemptions, and a convoluted web of “incentives” have created a distorted business environment. This “handout economy” has resulted in a fiscal deficit that is now the culmination of decades of accumulated errors. However, if the diagnosis is correct, the prescription—i.e., the specific conditionalities and targets of the current programme — is a master class in economic self-sabotage.

The fundamental flaw in the IMF’s approach is a dogmatic adherence to revenue extraction at the cost of value creation. By forcing the government to meet rigid fiscal targets, and through any means necessary at this point, the Fund has encouraged policies that stifle the very export-led growth required to break the debt cycle. Two specific examples illustrate this detachment from economic logic.

The first is the amendment to the Export Facilitation Scheme (EFS). In a bid to raise revenue, the policy was shifted to withdraw the zero-rating of sales tax on local inputs for export manufacturing, while inexplicably maintaining it for imported inputs. This decision defies the basic tenets of industrial economics. The purpose of an EFS is to allow exporters to source materials without the burden of domestic taxes that render their final products uncompetitive globally.

By taxing local inputs but allowing sales tax-free access to imported ones, the policy effectively creates a structural barrier to the development of backward linkages. It incentivizes Pakistani exporters to import raw materials rather than sourcing them domestically, effectively outsourcing the supply chain. This is happening at a time when the global economy is shifting. Global value chains are being downscaled into regional ones due to increasing geopolitical tensions and climate risks. Countries like Vietnam and Bangladesh are rushing to deepen their local supply chains to insulate themselves from these shocks. Pakistan, under the guise of IMF-mandated tax harmonization, is doing the opposite: deepening its import dependence and permanently damaging the prospect of domestic industrial depth and forcing already developed export supply chains to become “assembly plants” for foreign components.

The second example is the policy regarding gas supply for industrial captive power usage. The 2021 decision by the Cabinet Committee on Energy (CCoE) to transition industry away from captive gas generation was born of a specific context: a desire to utilize surplus generation capacity by shifting single-cycle captive users to national power grid. However, the implementation under the current IMF programme has ignored the vastly different global and local energy dynamics of today, especially the influx of solar PV and Battery Energy Storage Systems (BESS), and the operational realities of the grid itself.

The government, driven by programme targets, imposed a levy on gas supply for captive power usage. When calculated according to the law, it yields a negative value, implying no levy should exist. Yet, it was imposed to force industries off gas and onto the national grid. The logic was to “save” the grid by increasing demand. But the grid was already dying, plagued by inefficiencies, theft, cross-subsidies and capacity payment issues that are the underlying reasons for diminishing industrial and overall demand.

A working regime of captive power generation, which provided reliability to industrial and export sectors was dismantled to provide a fleeting lifeline to an unsustainable grid. This created an artificial over-supply of gas, leading to direct losses of hundreds of millions of dollars. The industry is now saddled with higher energy costs and unreliable power, while the grid remains as insolvent as ever. The general wisdom that “if it ain’t broke, don’t fix it” was ignored, and now both the alternative (captive) and the primary (grid) are broken.

In both the EFS and gas levy cases, the IMF programme, ostensibly designed to dismantle structural barriers, has erected new ones. These policies have suffocated the country’s businesses and people, proving fully counter-productive to the goal of fiscal and external solvency.

Everyone agrees that the historic economic model of state patronage was flawed and resulted in suboptimal allocation of resources. But there is a difference between weaning an addict off drugs and starving a healthy person. The IMF programme appears unable to distinguish between withdrawing support and subsidies, and actively destroying the ecosystem required for legitimate businesses to function.

This raises the uncomfortable question of ownership. On paper, the IMF deals with the Finance Minister and the Governor of the State Bank. Technically, all policies within the Letter of Intent are the government’s own ideas. In reality, the programme reflects the behest of those holding the greatest political and economic leverage. When policies fail, the IMF claims the government designed them; the government claims the IMF demanded them. This ambiguity serves everyone but the country and its citizens.

We are witnessing the institutionalization of a “survivalist” economy. Every policy choice is dictated by the need to pass the next IMF review, regardless of whether that policy erodes the tax base for the next decade. When you tax the most compliant sectors of the economy to the point of bankruptcy, you aren’t fixing the fiscal deficit; you are liquidating the state’s future assets. In the rush to make the balance sheet look palatable for the next tranche, we are the forest for the trees: the economy is as vulnerable as ever, headed nowhere except, most likely, into another IMF program.

This cycle must be broken, and the timeline is very tight. The current programme ends in September 2027, less than two years from now. Unless the ship is turned around within the next twelve months, Pakistan will inevitably sleepwalk into yet another bailout, likely with even harsher conditions.

The core issue remains that the government’s expenditure is unsustainable. Tax revenue has not kept pace with needs, despite the Federal Board of Revenue (FBR) enforcing higher rates and “smarter” collection methods. The reason for this stagnation is not just evasion, but the destruction of the tax base. By depressing thousands of businesses that were already on the brink, the government has shrunk the pie it wants to eat more of.

To exit this trap, the government must go the extra mile. It must ruthlessly cut its own expenditure to create fiscal space. We cannot ask the private sector to endure “austerity” while the machinery of the state remains bloated and inefficient. The FBR’s “enforcement” must move away from squeezing existing taxpayers and toward expanding the net. This space must then be used to provide relief to the private sector, particularly on taxes—both explicit and implicit, such as the cross-subsidies embedded in energy prices. There is no other way out. The private sector is the engine of growth; the government is just the regulator. If the regulator consumes all the fuel, the engine stalls.

If Pakistan is to exit this perpetual cycle of IMF programmes, the next eighteen months must see a radical shift. True economic sovereignty cannot be “granted” by a lender; it must be earned through fiscal discipline that the state imposes on itself, rather than having it imposed from abroad. The solution is not complex, just politically difficult.

If Pakistan fails to make these choices, it will continue to mirror the late Ottoman experience. The OPDA did not officially end the Ottoman Empire, but it ensured the Empire could never again compete as a sovereign power. It became an entity that existed merely to pay its bills, while its people grew poorer and territory more vulnerable.

Pakistan stands at a similar crossroads. We are currently trading our long-term socioeconomic interests for the privilege of staying afloat. But staying afloat is not the same as moving forward. Unless we reclaim our policymaking from the narrow, revenue-centric confines of IMF programmes, we are not just managing a crisis but rather our own decline.

Copyright Business Recorder, 2025

PUBLIC SECTOR EXPERIENCE: He has served as Member Energy of the Planning Commission of Pakistan & has also been an advisor at: Ministry of Finance Ministry of Petroleum Ministry of Water & Power

PRIVATE SECTOR EXPERIENCE: He has held senior management positions with various energy sector entities and has worked with the World Bank, USAID and DFID since 1988. Mr. Shahid Sattar joined All Pakistan Textile Mills Association in 2017 and holds the office of Executive Director and Secretary General of APTMA.

He has many international publications and has been regularly writing articles in Pakistani newspapers on the industry and economic issues which can be viewed in Articles & Blogs Section of this website.

Comments