Oil and Gas Development Company Limited: performance and outlook

Oil and Gas Development Company Limited (PSX: OGDC) is Pakistan’s largest exploration and production company, engaged in exploration, drilling, production, reservoir management, and engineering support.

It holds the most extensive exploration acreage in the country, covering over 40 percent of awarded blocks, giving it a leading role in the development of Pakistan’s oil and gas resources.

OGDC in the recent past – (FY19-FY24)

OGDC has as managed to remain profitable despite structural challenges such as declining production from mature reserves. Its financial performance has moved in line with international oil prices and currency movements, with cost management and exploration results shaping overall earnings.

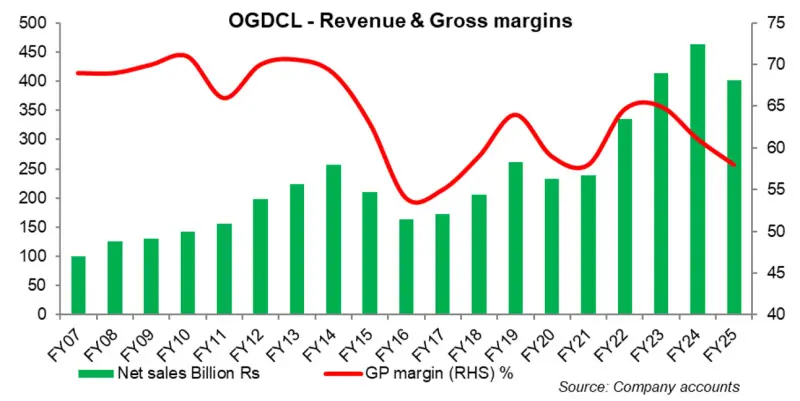

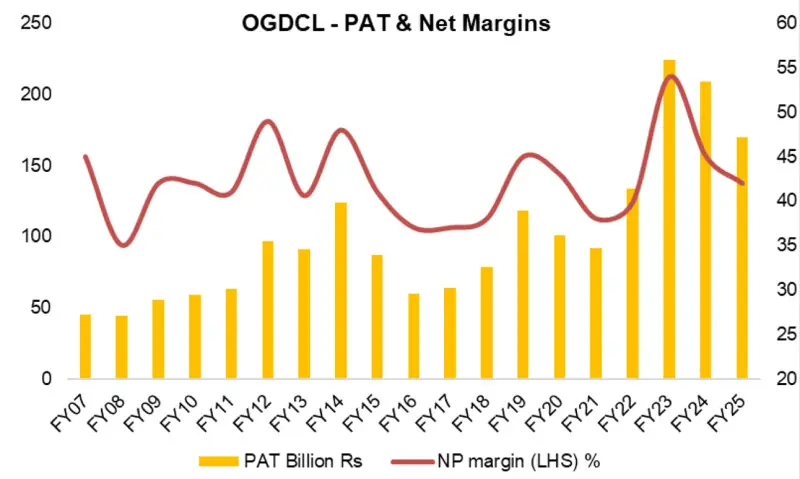

In FY19, the company’s revenues grew by 27 percent, leading to a 57 percent increase in net profit. This improvement was due to higher realized crude oil and gas prices, while crude oil and gas production levels were flat and LPG production increased modestly.

The company drilled 16 wells and reported three discoveries. Additional support to earnings came from exchange rate gains, higher other income, profit contributions from associates, and lower exploration costs, although rising operating costs, particularly amortization, partly offset these gains.

FY20 reflected a sector-wide downturn due to falling oil prices and COVID-19 disruptions, resulting in a 15 percent decline in net profit.

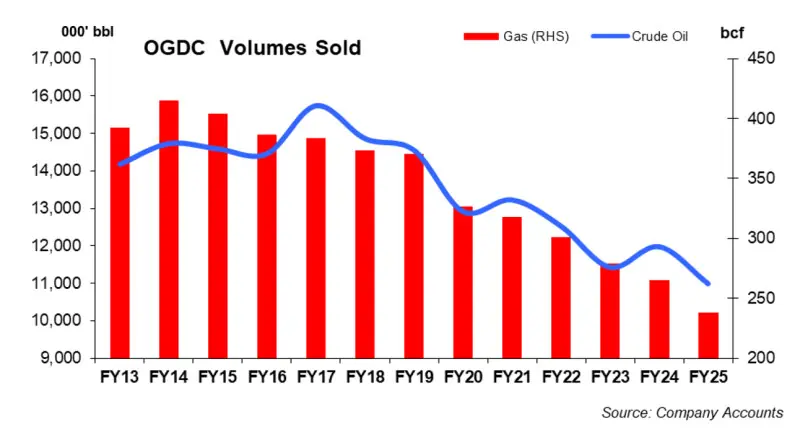

Revenues were down 6 percent as realized crude oil and LPG prices fell by 20 percent and 11 percent, respectively, while oil, gas, and LPG production volumes declined by about 12 percent, 12 percent, and 11 percent.

Higher exploration costs, including dry well expenses, added further pressure on margins.

The sector began to recover in FY21. OGDC’s crude oil production increased by 2.3 percent while gas output fell 2.6 percent.

Revenues grew by 2.65 percent, supported by higher gas prices and LPG output, while net profit increased by 9.3 percent due in part to lower exploration costs and fewer dry wells. These gains were offset by reduced other income and higher amortization and repair costs.

In FY22, higher oil prices and currency depreciation boosted revenue by 40 percent, with realized crude oil and gas prices increasing by 62 percent and 14 percent, respectively.

Production of crude oil and gas fell by 4 percent and 5 percent, but exploration costs were down 10 percent on account of fewer dry wells. The company drilled 13 wells, made seven discoveries, and added ten wells to production. Profit before tax rose by 80 percent, while net profit increased 46 percent due to the imposition of a Super Tax.

The following year, earnings rose 68 percent as revenues grew 23 percent amid a 28 percent rupee depreciation. Exploration costs increased 22 percent due to dry wells, while other income doubled because of exchange gains.

In FY24, revenue grew 12 percent despite a 4.3 percent fall in realized crude oil prices and a 6 percent decline in gas production from major fields. Net profit fell by 7 percent as higher operating costs, including rents, taxes, and asset amortization, offset a 5 percent improvement in gross profit.

Exploration costs dropped 34 percent due to fewer dry wells, while drilling activity remained steady with 13 wells spudded and five discoveries made. Non-operating income declined 73 percent due to exchange losses and fewer one-off gains, reducing the net profit margin to 45 percent from 54 percent in FY23.

OGDC FY25 Performance

The E&P giant closed FY25 with a mixed set of results, reflecting the twin pressures of declining production volumes and lower global oil prices, offset partially by robust other income and the company’s continued exploration drive.

The firm reported after-tax earnings of around Rs170 billion, representing a 19 percent year-on-year decline compared to FY24.

The fall in profitability was primarily attributable to a 13 percent drop in net sales, caused by a 6–7 percent decline in oil output to around 30,900 barrels per day, a 9 percent decline in gas production to 652 mmcfd, and lower realized oil prices averaging $60.8 per barrel versus USD 68.7 last year.

Gas curtailment by SNGPL due to surplus RLNG was particularly costly, with management estimating a revenue loss of Rs40–43 billion.

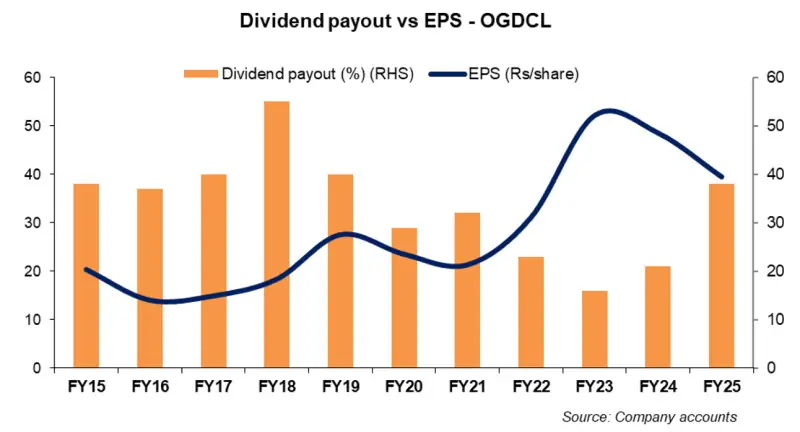

Despite weaker earnings, OGDC declared its highest ever full-year dividend at Rs15.05 per share, compared to Rs10.10 in FY24.

Gross margins narrowed to 57.7 percent from 61.1 percent, reflecting the impact of lower volumes and prices, while the effective tax rate rose sharply to 39.2 percent against 28.9 percent in FY24.

Exploration costs climbed 49 percent to Rs18.8 billion, largely due to three to four dry wells and intensified seismic activity across blocks. However, other income nearly doubled to Rs82 billion, driven by interest income from TFCs, delayed payment surcharges, and significant foreign exchange gains amid PKR volatility.

While FY25 earnings were subdued, OGDC’s record dividend payout underscores its resilience, underpinned by strong reserves, active exploration, and stable cash generation along with ongoing production revival projects and planned capex.

OGDC in FY26 and beyond

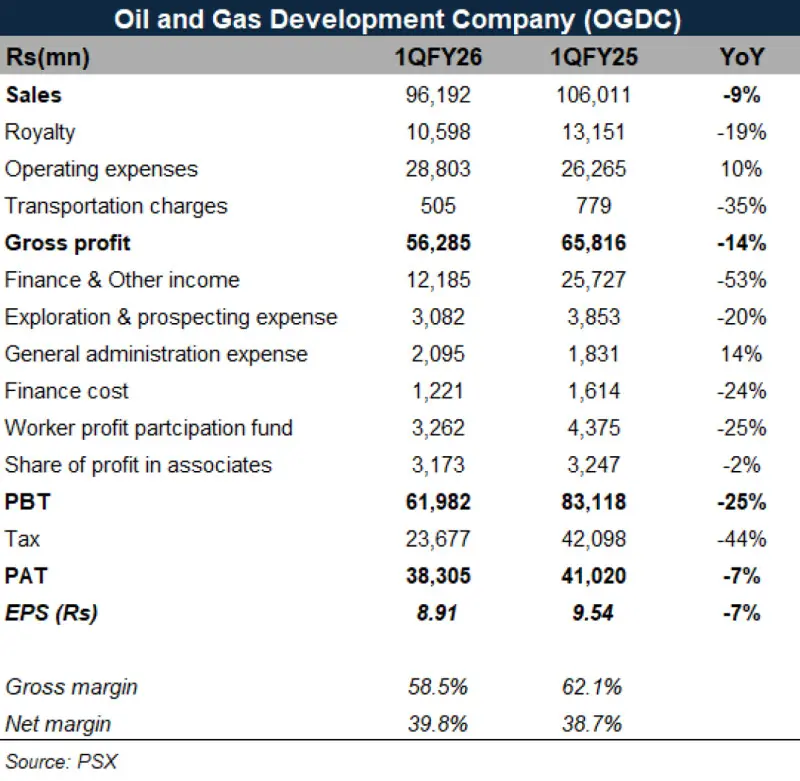

OGDC reported a 7 percent year-on-year decline in 1QFY26 earnings, driven by a 9 percent fall in revenue amid lower oil realizations, a modest drop in oil output, and steeper gas curtailments. Arab Light prices averaged in the low $70s per barrel, down from above $80 a year earlier. Despite this, gross margins remained resilient at around 59 percent.

Other income was the main weak spot, dropping by more than half as last year’s penal income, high TFC returns, and supportive FX gains were absent, while lower interest rates compressed yields. Some of this pressure was offset by reduced exploration spending and a lower effective tax rate.

Operationally, trends are improving. Cash recoveries now exceed billings, power-sector receivables have declined sharply, and the remaining backlog is expected to clear this quarter.

Gas curtailments are being applied only to non-oil fields under an arrangement with SNGPL, while management expects gas to regain prominence in the production mix as new finds come online. Offshore exploration remains a longer-term prospect.

In sum, near-term earnings softened, but underlying operational and balance-sheet indicators point to a steadier medium-term outlook.

Comments

Comments are closed for this article.