Shield Corporation Limited (PSX: SCL) was incorporated in Pakistan as a public limited company in 1975. The company’s principal business activity is the manufacturing, trading and sale of oral hygiene and baby care products. SCL caters to the needs of over 300 towns and cities of Pakistan. Besides, the company has its presence in Europe, Asia and Africa.

Pattern of Shareholding

As of June 30, 2025, SCL has a total of 3.9 million shares outstanding which are held by 440 shareholders.

Directors, CEO, their spouse and minor children have the majority stake of 74.44 percent in the company followed by local general public holding 25.20percent shares of SCL. The remaining shares are held by other categories of shareholders.

Performance Trail (2019-24)

Over the period under consideration, SCL topline dipped in 2020, 2024 and 2025. Its bottomline eroded in 2019 and 2020. In 2020, the company posted net loss. SCL’s bottomline boasted a massive turnaround in 2021, however, the fortune turned out to be momentary as the bottomline slidback in the consequent year. In 2023, SCL’s bottomline greatly recovered, followed by net loss in 2024 and 2025. The company’s margins followed a similar trajectory to its bottomline. The detailed performance review of the period under consideration is given below.

In 2019, net sales of SCL grew by a marginal 5.95 percent year-on-year to clock in at Rs.1778.79 million. Locally, both oral care and baby care segments recorded an increase in revenue, however, the export sales massively dropped during the year especially in the oral care segment. Afghanistan, the main export destination of SCL witnessed a year-on-year drop of 80 percent in sales revenue. Moreover, there were no sales to Europe during the year.

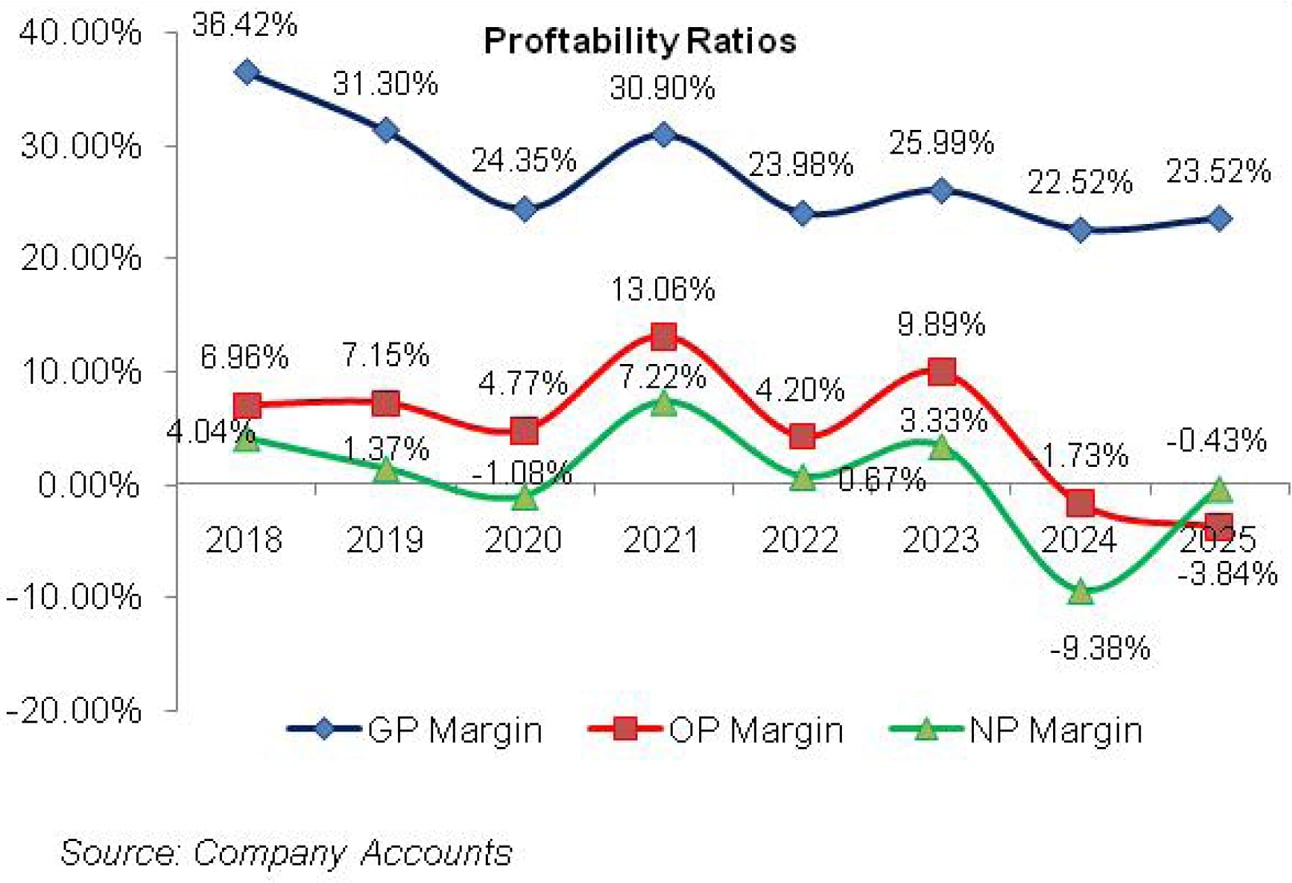

Cost of sales grew by 14.49 percent year-on-year in 2019 on the back of Pak Rupee depreciation which rendered imported raw materials expensive. Consequently, GP margin of SCL dropped from 36.42 percent in 2018 to 31.30 percent in 2019. Gross Profit, in absolute terms,also slid by 8.95 percent year-on-year in 2019. Operating expenseslid by 15.65 percent during the year as the company spent less on advertising and promotion activities and focused more on trade promotion through discounts. Other income behaved favorably as the company made scrap sales during the year.

Conversely, other expense didn’t offer any support and grew by 50.28 percent year-on-year mainly on the back of loss on foreign exchange. Operating profit managed to post a marginal 8.88 percent year-on-year growth in 2019. OP margin slightly moved up from 6.96 percent in 2018 to 7.15 percent in 2019. What gave a major blow to the bottomline was a whopping 122.26 percent year-on-year rise in finance cost in 2019. This was on the back of higher discount rate and increased borrowings during the year.

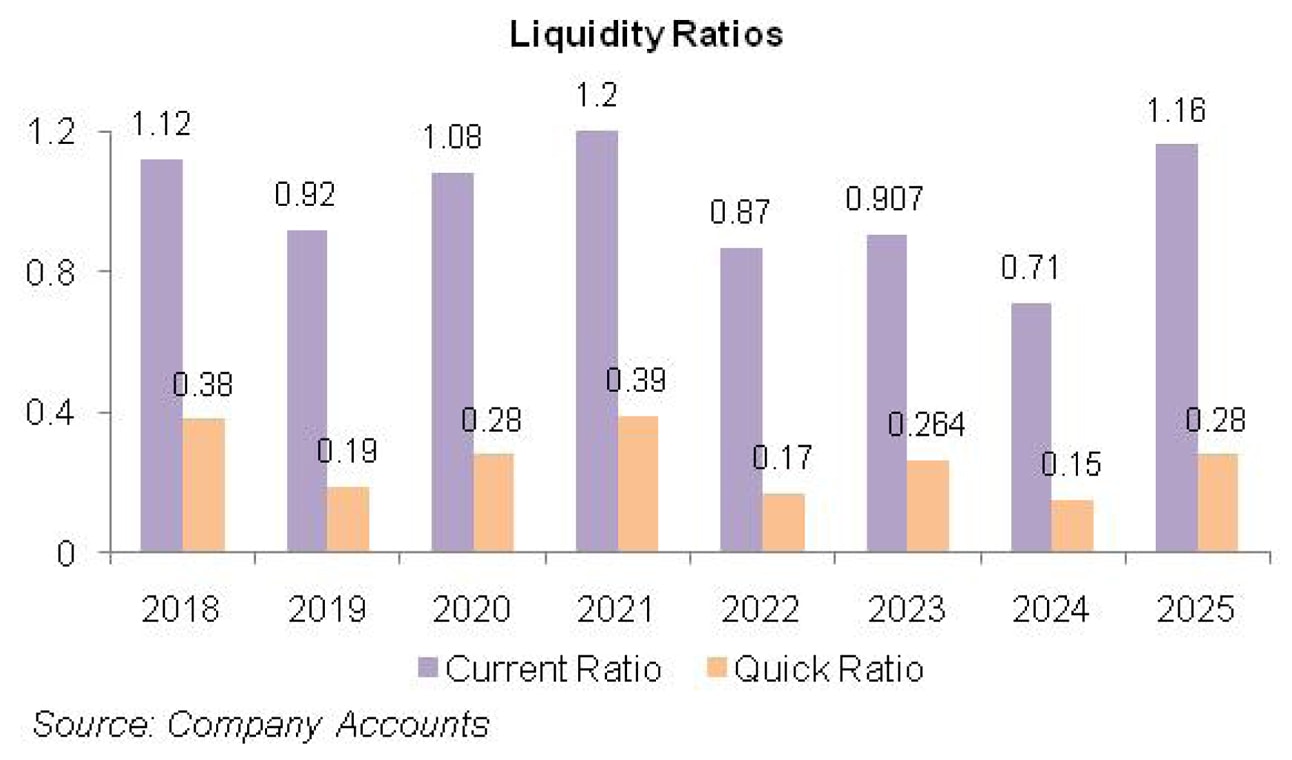

Debt-to-equity ratio of SCL rose from 22 percent in 2018 to 33.5 percent in 2019. The bottomline posted a major slump of 64.17 percent in 2019 to clock in at Rs.24.33 million. NP margin dropped to 1.37 percent in 2019 from 4 percent in 2018. EPS also dropped to Rs. 6.24 in 2019 from Rs.17.4 in the previous year.

In 2020, the world economy was marred by the global pandemic which also took its toll on the topline of SCL. The topline dropped by 3.95 percent year-on- year in 2020 to clock in at Rs. 1708.62 million. This was because the export sales of the company continued to shrink. During the year, the company only made export sales to Mozambique. Locally, the baby care segment posted 18 percent year-on-year uptick, however, oral care and hygiene segment remained tamed.

Gross profit also slid by 25.28 percent year-on-yearin 2020 as high cost of raw and packaging material as well as fuel and energy coupled with Pak Rupee depreciation pushed the cost up by 5.77 percent year-on-year in 2020. GP margin also nosedived to 24.35 percent in 2020.

Operating expenses slid by 14.58 percent in 2020 as the company massively cut down its expenditure on advertisement and promotional activities. Other expense dropped by 97.74 percent year-on-year in 2020 due to high-base effect as provision for WWF, WPFF, doubtful advances, slow moving stores and spares which were booked last year weren’t recorded in 2020. Moreover, loss on foreign exchange and disposal of fixed assets also dipped during 2020. Other income grew by 296.63 percent in 2020 on the back of reversal of aforementioned provisions coupled with scrap sales made during the year.

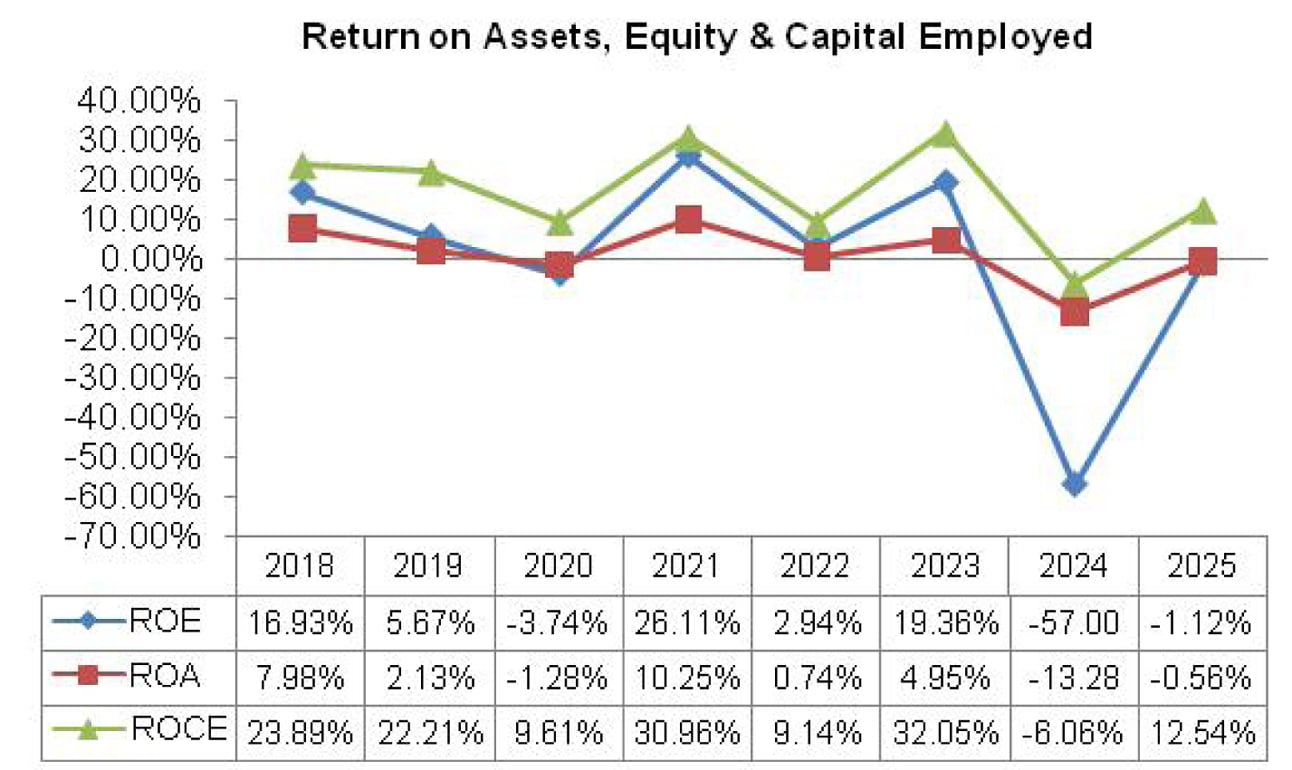

Despite all the positive developments on the operational front, operating profit dropped by 35.91 percent year-on-year in 2020 while OP margin moved down to 4.77 percent in 2020. Finance cost also grew by a massive 142.54 percent in 2020 on the back of high discount rate in the initial quarters of FY20 coupled with increased short-term and long-term borrowings during the year. Debt-to-equity ratio soared to 70.64 percent in 2020. This dragged the bottomline into red zone with net loss of Rs.18.45 million in 2020. Loss per share stood at Rs. 4.73 in 2020.

2021 was the most privileged year for SCL as not only did its topline grow by 25.75 percent year-on-year to clock in at Rs.2148.55 million, the bottomline also recovered from net loss to boast the highest ever net profit. While local sales showed a stunning growth in 2021, export sales also witnessed some signs of recovery especially in Mozambique. The company also added Ireland to its export destination during the year.

High sales volume, better sales mix and revised pricing enabled the company to absorb the fixed overhead and post a year-on-year growth of 59.57 percent in its gross profit. GP margin also improved to 30.90 percent in 2021.

Operating expense grew by 7.1 percent in line with inflation, however, other expense multiplied by over 5243 percent in 2021 on the back of provisions booked for WWF and WPFF coupled with loss on disposal of fixed assets and impairment of fixed assets. This whopping rise in other expense was partially offset by a favorable movement in other income on the back of scrap sales, grant income and exchange gain.

SCL’s operating profit posted a staggering year-on-year growth of 244 percent in 2021 with OP margin standing at its highest level of 13 percent. Finance cost was also under control due to low discount rate coupled with lesser borrowings during the year. Debt-to-equity ratio dropped to 52 percent in 2021. SCL posted net profit of Rs. 155.11 million in 2021 with the highest ever NP margin of 7.22 percent. EPS for the year was Rs. 39.77.

As the signs of COVID-19 began to fade, 2022 brought another list of challenges for the company and for the economy as a whole. Political instability, record high inflation, discount rate and sharp depreciation of Pak Rupee, once again wreaked havoc on the profitability and margins of SCL.

While the topline grew by 23.90 percent year-on-year to clock in at Rs.2662.05 million on the back of volumetric growth as well as upward revision in price, high cost of sales on the back of rising commodity prices and exchange rate fluctuations put pressure on the GP margin which slid to 23.98 percent in 2022.

Gross profit also shrank by 3.85 percent in absolute terms in 2022. Operating expense also grew by 43.89 percent in 2022 owing to inflationary pressure coupled with increased spending on advertising and promotion. Freight charges also expanded owing to increase in offtake both in local and export markets.

The company once again started making sales to Afghanistan which were discontinued for quite some time. Other income provided support to the bottomline as it grew by 136.38 percent in 2022 on the back of rental income, scrap sales and grant income. Other expense also gave a breather and dipped by 13 percent in 2022. SCL couldn’t sustain its operating profit, which dropped by 60.17 percent year-on-year with OP margin squeezing to 4.20 percent in 2022.

Finance cost grew by 62 percent on the back of increased borrowings and high discount rate. Debt-to-equity ratio clocked in at 119.82 percent in 2022. SCL’s bottomline also plunged by 88.55 percent year-on-year in 2022 to clock in at Rs.17.76 million with NP margin of 0.67 percent. EPS massively dipped to Rs.4.55 in 2022.

In 2023, SCL recorded a massive year-on-year growth of 63.69 percent to clock in at Rs.4357.63 million. This was on account of enhancement in sales volume as well as upward price revision during the year. Both local and export sales boasted improvement during the year. The company exported its products to new destinations which it didn’t cater to in the previous year. These included Sudan, UAE, Yemen, Ghana, Ireland etc.

Cost of sales grew by 59.37 percent in 2023 due to commodity super cycle, Pak Rupee depreciation, elevated energy tariff and high indigenous inflation. Despite that, upward prices revision enabled the company to record 77.4 percent stronger gross profit in 2023 with GP margin climbing up to 26 percent. Operating expense mounted to 29.38 percent in 2023 due to higher payroll expense, freight expense as well as travelling & conveyance allowance incurred during the year.

Other expense escalated by 69.48 percent in 2023 due to hefty exchange loss incurred on purchases as well as higher allowance booked for WWF and WPPF. Other expense was greatly offset by 7.79 percent higher other income recognized during the year, which was the result of higher rental income and grant income. Operating profit strengthened by 285.72 percent in 2023 with OP margin jumping up to 9.89 percent.

Finance cost surged by 138.87 percent in 2023 due to high discount rate coupled with increased short-term borrowings to meet working capital requirements. Despite increased borrowings, higher revenue reserve didn’t allow the debt-to-equity ratio to pick up during the year which stood at 84.9 percent in 2023. Net profit registered a whopping growth of 716 percent to clock in at Rs.144.96 million in 2023 with EPS of Rs.37.17 and NP margin of 3.33 percent.

After recording a stunning growth in 2023, SCL’s topline dipped by 11.26 percent to clock in at Rs.3867.12 million in 2024. This was due to a slump recorded in the sales volume of the company owing to a shift in the buying pattern of the company’s consumers on account of acute inflationary pressure. Both local and export sales weakened during the year. The company didn’t make any sales to Yemen, UAE, Sudan, Ireland and Afghanistan in 2024.

Higher utility prices, and high cost of raw materials coupled with overall inflationary pressure resulted in 23.1 percent decline in SCL’s gross profit in 2024 with GP margin slipping to 22.52 percent.

Operating expense multiplied by 39.35 percent in 2024 predominantly due to higher payroll expense, advertisement & promotion budget, freight expense as well as travelling & conveyance charges incurred during the year. Other expense plunged by 80.83 percent in 2024 due to no provisioning done for WWF, WPPF, lesser provisioning done for slow moving stores and spares as well as considerably lower exchange loss incurred during the year due to stability in Pak Rupee. Other income also eroded by 11.22 percent in 2024 due to lower scrap sales and no gain on foreign exchange recorded during the year. For the first time during the period under consideration, SCL recorded operating loss of Rs.66.91 million in 2024.

Finance cost increased by 48.17 percent in 2024 due to heightened discount rate. The company recorded net loss of Rs.362.68 million with loss per share of Rs.92.99 in 2024.

In 2025, SCL posted year-on-year decline of 23.31 percent in its net sales which clocked in at Rs.2965.83 million. While local sales still form the largest chunk of SCL’s sales mix, it dipped by 25.77 percent year-on-year to clock in at Rs.2991.113 million in 2025. Conversely, export sales strengthened by 181.96 percent to clock in at Rs.64.060 million. Surge in export sales mainly came on the back of export proceeds from Afghanistan, Sudan, Muritania, Senegal, Madagascar, Uzbekistan and Jordan.

Majority of the export destinations were added by the company only in 2025. Cost of sales slid by 24.30 percent in 2025 resulting in 19.89 percent plunge in gross profit. GP margin slightly improved to clock in at 23.52 percent in 2025. This was because of stability of Pak Rupee and decline in the prices of some commodities in the international market. Distribution expense dropped by 28.90 percent in 2025 as the company considerably squeezed its sales promotion budget as well as its sales force.

Administrative expense slid by 4.57 percent in 2025 due to a downtick in legal & professional charges as well as payroll expense. SCL streamlined its workforce from 128 employees in 2024 to 117 employees in 2025. During the year, the company booked 78.62 percent lesser provisioning for ECL.

Conversely, other expense mounted by 1408.07 percent in 2025 due to massive loss incurred on the disposal of operating fixed assets and impairment booked on non-current assets (particularly diaper related assets) held for sale. Other income also nosedived by 37 percent in 2025 due to less rental income, grant income and scrap sales recognized during the year.

SCL recorded 70 percent higher operating loss to the tune of Rs.113.79 million in 2025. Two positive developments during the year which enabled the company to reduce its net loss were gain worth Rs.285.51 million recorded on the disposal of investment property and 51.86 percent diminution recorded in finance cost on the back of monetary easing and lesser borrowings. Debt-to-equity ratio fell from 95.87 percent in 2024 to 28.31 percent in 2025. Net loss shrank by 96.51 percent to clock in at Rs.12.66 million in 2025. This translated into loss per share of Rs.3.25 in 2025.

Recent Performance (1QFY26)

During the first quarter of the ongoing fiscal year, SCL recorded a marginal decline of 0.31 percent in its net sales, which clocked in at Rs.717.67 million. While local sales improved by 4.95 percent to clock in at Rs.734.695 million, export sales drastically fell by 92.73 percent to clock in at Rs.2.73 million.

The company made export sales only to Ghana in 1QFY26. Improvement in macroeconomic indicators such as inflation, stability of Pak Rupee and steadiness in global commodity prices enabled the company to cut down its cost by 2.78 percent in 1QFY26. This enabled the company to record 7.85 percent stronger gross profit in 1QFY26 with GP margin clocking in at 25.14 percent versus GP margin of 23.23 percent recorded in 1QFY25.

Distribution expense stayed intact in 1QFY26. Conversely, administrative expense surged by 10.30 percent in 1QFY26 probably due to higher payroll expense. As against reversal booked in 1QFY25, SCL booked allowance worth Rs.2.43 million on ECL. Other expense also massively surged during the period to clock in at Rs.9.08 million. This majorly included loss incurred on the disposal of investment property.

Other income also diluted by 89.12 percent in 1QFY26 seemingly due to less rental income, grant income and scrap sales recorded during the period. SCL posted operating loss of Rs.6.299 million in 1QFY26 versus operating profit of Rs.2.14 million recorded in 1QFY25.

Finance cost tapered off by 57.55 percent in 1QFY26 due to monetary easing and lower borrowing level as sponsors are granting loan to the company. Net loss plunged by 37.44 percent to clock in at Rs.36.226 million in 1QFY26. This translated into loss per share of Rs.9.29 in 1QFY26 versus loss per share of Rs.14.85 recorded in 1QFY25.

Future Outlook

The company is planning to tap new geographical locations. The company also has a sizeable share in the local market, which is showing further improvement due to progress witnessed in the macroeconomic indicators. To optimize its financial performance in both local and export markets, SCL is required to play with its sales mix and pricing strategy as well as raw material sourcing to strengthen margins.

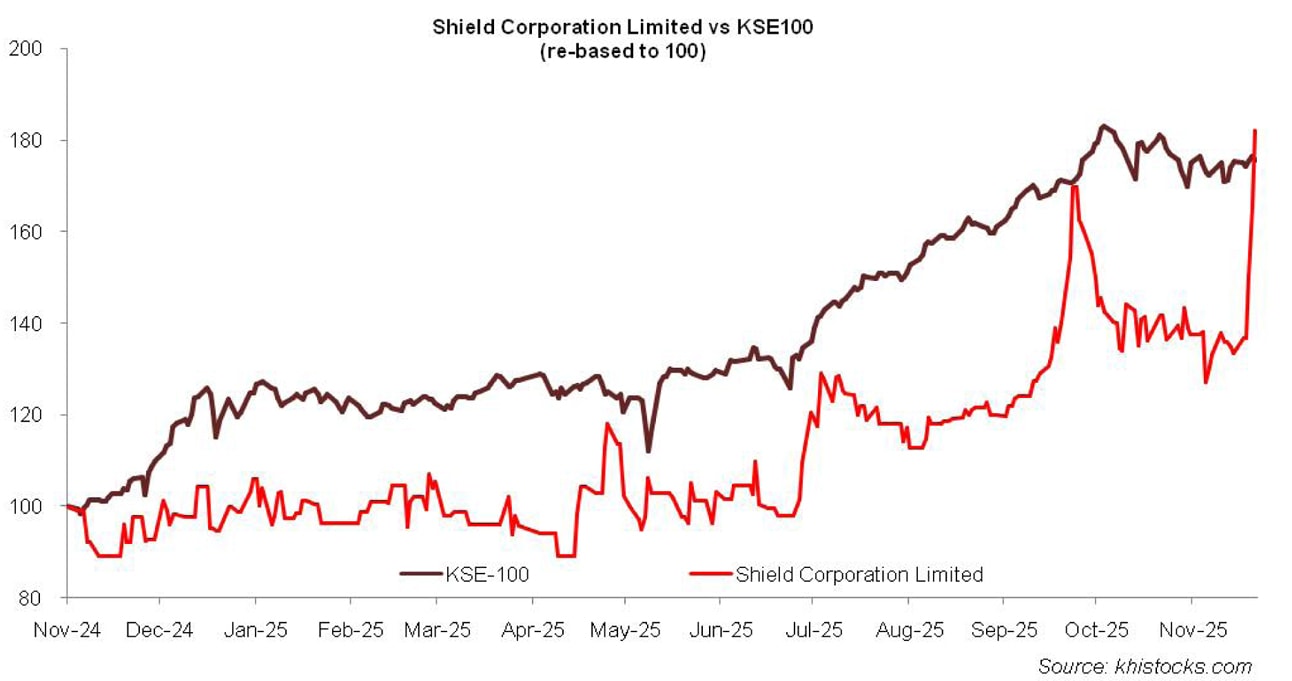

The company has recently announced to undergo voluntary delisting of its shares from PSX. The sponsors of the company have been authorized to buy back the shares from the minority shareholders. This is because the liquidity of the company’s shares has been quite low with an average daily trading volume of 923 shares for the past one year. The company has been incurring net losses for the past two years and has not been able to pay dividend to its shareholders. Hence, delisting will free up the company’s resources and enable the management to focus on the core business of the company.

Comments

Comments are closed for this article.