Airlink Communication Limited (PSX: AIRLINK) was incorporated in Pakistan as a private limited company in January 2014 and was converted into a public limited company in April 2019. The company is engaged in import, export distribution, identing, wholesale and retail of communication and IT related products and services including smart phone/ cellular phones, tablets, laptops accessories and related products.

Pattern of Shareholding

As of June 30, 2025, AIRLINK has a total of 395.269 million shares outstanding which are held by 13,041 shareholders. Sponsors have the majority stake of 71.69 percent in the company followed by foreign companies holding 14.90 percent shares.

Local general public accounts for 6.06 percent shares of AIRLINK while Directors, CEO, their spouse and minor children hold around 2.15 percent shares. About 1.26 percent of the company’s shares are held by Insurance companies. The remaining shares are held by other categories of shareholders.

Historical Performance (2021 – 2025)

AIRLINK posted its first annual report as a public listed company in 2020. In 2021, the company’s topline inched up followed by a decline for the successive two years. In 2024, AIRLINK’s topline posted a staggering growth which was followed by a downtick in 2025. Its bottomline expanded in 2021 and 2022 followed by a steep plunge in 2023. In 2024 and 2025, the company’s bottomline strengthened to attain an unparalleled level in 2025.

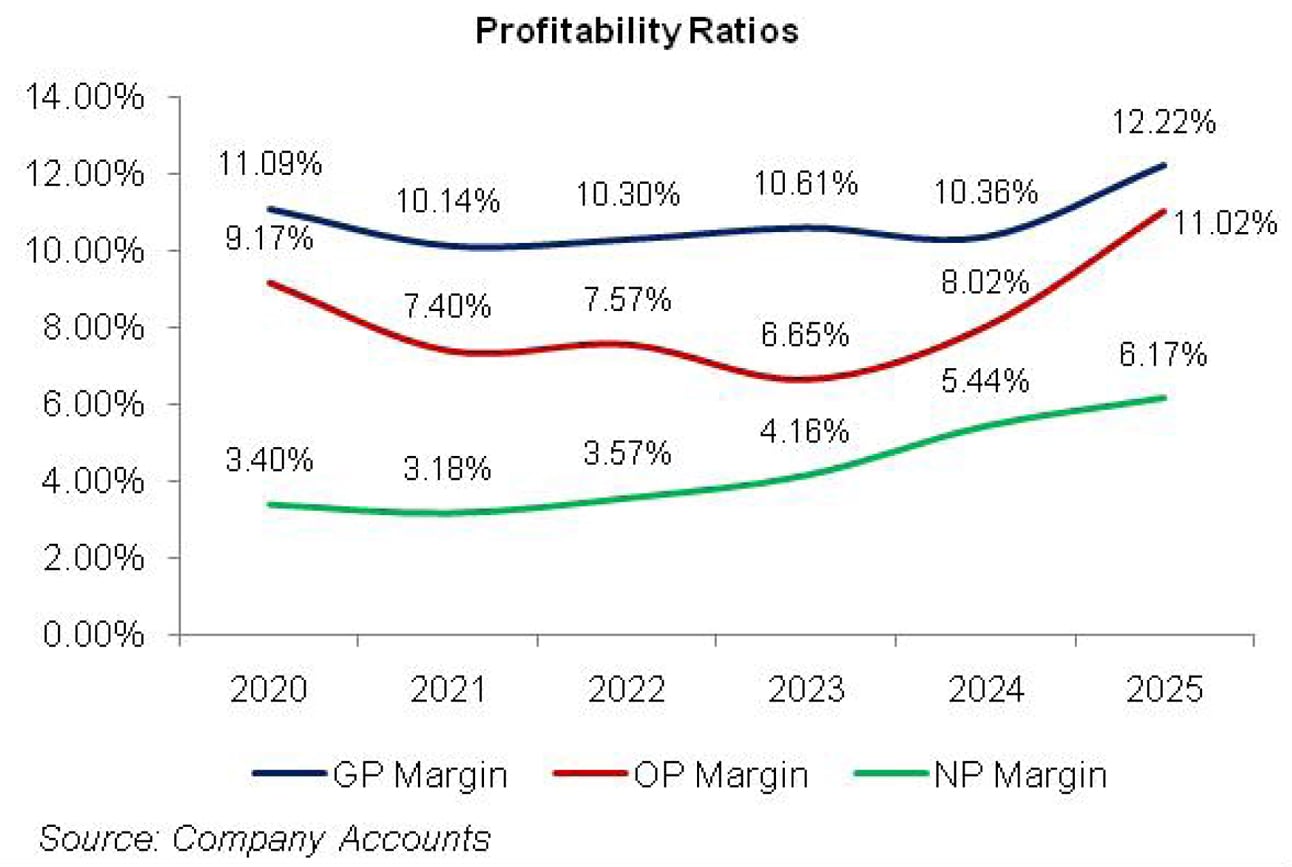

AIRLINK’s margins which considerably eroded in 2021, bounced back in the next year. The company’s gross and net margins improved in 2023, however, its operating margin ticked down. In 2024, AIRLINK’s gross margin slightly dropped while its operating and net margins greatly improved. In 2025, AIRLINK’s margins attained their optimum level. The comprehensive performance evaluation of AIRLINK since its public listing is outlined below.

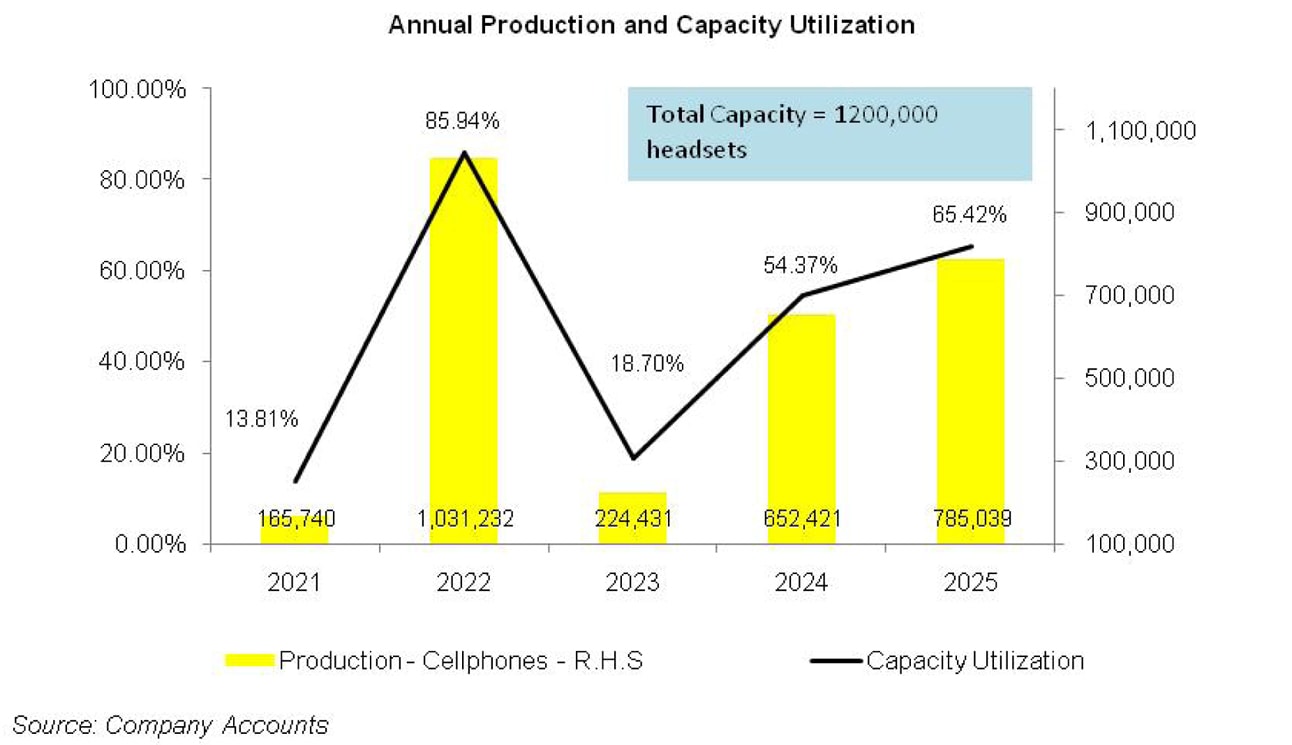

In 2021, AIRLINK’s topline grew by 10.15 percent year-on-year to clock in at Rs.47,372.80 million. The company’s production plant became operational in April 2021 with the total production capacity of 1.2 million cell phones; however, the company was able to utilize 13.8 percent of its installed capacity.

Modest revenue growth was the result of low penetration level of 3G/4G services. Moreover, the economy had recently started recovering from the shocks of COVID-19.

The company didn’t make any export sales in 2021. Service income significantly grew during the year; however, it had a very insignificant contribution in the total sales mix of AIRLINK in 2019. High cost of sales due to Pak Rupee depreciation and elevated level of inflation resulted in a paltry 0.67 percent rise in gross profit with GP margin sliding down from 11.09 percent in 2020 to 10.14 percent in 2021.

Administrative expense hiked by 39.74 percent in 2021 as a result of higher payroll expense as AIRLINK’s number of employees increased from 477 in 2020 to 530 in 2021. Other factors which drove up administrative expense in 2021 were high depreciation, repair & maintenance and allowance for ECL.

Distribution expense spiked by 21.83 percent in 2021 due to higher payroll expense, freight outward and depreciation while AIRLINK considerably reduced its advertising & promotion budget in 2021. Other income slid by 59.91 percent in 2021 on account of considerably low profit recognized on investments. Other income was almost wiped off by considerably higher other expense recorded by AIRLINK during the year due to higher provisioning for WWF, loss on termination of lease as well as exchange loss.

Operating profit plummeted by 11.05 percent in 2021 with OP margin slipping to 7.40 percent from 9.17 percent in 2020. Due to lower short-term and long-term borrowings as well as monetary easing, AIRLINK’s finance cost dropped by 21.15 percent in 2021.

AIRLINK’s gearing ratio also nosedived from 65 percent in 2020 to 48 percent in 2021. Lower effect of tax on import stage drove down the company’s total tax expense for the year by 16.72 percent in 2021. As a consequence, net profit rose by 2.79 percent year-on-year in 2021 to clock in at Rs.1505 million with EPS of Rs.4.47 versus EPS of Rs.4.71 in the previous year. NP margin eroded from 3.40 percent in 2020 to 3.18 percent in 2021.

AIRLINK’s topline slumped by 2.56 percent to clock in at Rs. 46,159.70 million in 2022. At the onset of the year, the country was witnessing strong impetus in its economic activity; however, towards the end of the financial year, worsening politico-economic conditions of the country resulted in ban on imports of luxury items which restricted AIRLINK to import cell phones in CBU condition. After that, the SBP also issued notification to seek prior approval to establish L/Cs for the import of cell phones in CKD/SKD condition. With Russia-Ukraine war in full swing, there was an acute shortage of commodities, resulting in hike in prices.

Moreover, diminishing foreign exchange reserves of Pakistan resulted in drastic depreciation in the value of local currency. Demand for AIRLINK’s products also dipped due to decline in the purchasing power of consumers. During the year, the company utilized 85.94 percent of its installed capacity and produced 1.031 million cell phones. While gross profit tumbled by 0.96 percent in 2022, stringent cost control measures put in place by the management enabled AIRLINK to slightly drive up its GP margin to 10.30 percent in 2022.

Administrative expense escalated by 17.42 percent in 2022 as number of employees increased to 806 in 2022 which culminated into higher payroll expense. Higher fee & subscription charges followed by towering utility charges, travelling & conveyance and entertainment also pushed up the administrative expense in 2022.

Conversely, distribution expense slumped by 5.39 percent in 2022 on account of lower freight outward, salaries & wages as well as packing expense due to lower sales. Other income magnified by 235 percent in 2022 mainly on account of reversal of ECL, gain on termination of lease and modification gain on long-term loans.

Other expense also surged by 54.89 percent in 2022 due to increased profit related provisioning. Operating profit marched down by 0.38 percent in 2022; however, OP margin rebounded to 7.57 percent.

Despite monetary tightening, AIRLINK was able to cut down its finance cost by 7 percent in 2022 due to lower lease liabilities and short-term borrowing. AIRLINK’s gearing ratio fell to 27 percent in 2022.

The effect of expenses not allowed for tax, effect of deferred tax, prior year tax and FTR collectively lowered tax expense by 8.86 percent in 2022. This resulted in 9.54 percent rise in net profit which clocked in at Rs.1648.59 million with EPS of Rs.4.30 and slightly higher NP margin of 3.57 percent in 2022.

AIRLINK’s topline drastically fell by 53.41 percent to clock in at Rs. 21,503.91 million in 2023. The macroeconomic environment remained quite challenging characterized by Pak Rupee depreciation, import restrictions, commodity super cycle, high indigenous inflation and soaring discount rate.

The company was able to operate at 18.7 percent capacity owing to restriction on import. Shallow demand also played a pivotal role in thin revenue registered during the year.

The company was able to significantly cut down its cost of sales by 53.57 percent in 2023. Although gross profit thinned down by 52 percent in 2023, GP margin slightly improved to 10.61 percent.

Administrative expense was scaled down by 29.42 percent in 2023 as AIRLINK aggressively streamlined its workforce to 191 employees in 2023 versus 806 employees in the previous year.

Distribution expense also dipped by 39.18 percent in 2023 mainly on account of lower payroll expense, freight charges and advertising budget. Lower profit related provisioning resulted in 38 percent lesser other expense incurred by AIRLINK in 2023.

Other income also plunged by 38.34 percent in 2023 due to lesser reversal of ECL. Operating profit eroded by 59 percent in 2023 with the lowest OP margin of 6.65 percent. Regardless of high discount rate, AIRLINK was able to cut down its finance cost by 29.92 percent in 2023 by rationalizing its long-term and short-term borrowings. This resulted in its gearing ratio falling down to its lowest level of 20 percent in 2023.

Nevertheless, net profit plummeted by 45.74 percent in 2023 to clock in at Rs.894.54 million with EPS of Rs.2.33 – the lowest since 2020. On the positive front, AIRLINK was able to record a matchless NP margin of 4.16 percent in 2023 by streamlining its outstanding loans and overcoming its finance cost.

In 2024, AIRLINK’s topline registered a whopping year-on-year growth of 161.73 percent to clock in at Rs.56,282.42 million.

Measured recovery in economic activity, removal of import restrictions coupled with the company’s strategic measures over the course of the year and its ability to leverage its partnerships resulted in remarkable recovery in its sales volumes.

During the year, the company produced 652,421 cell phones which resulted in capacity utilization of 54.37 percent. Cost of sales surged by 162.44 percent in 2024 due to heightened cost of raw materials consumed coupled with elevated energy tariffs.

Spike in regulatory duties, clearing charges and sales tax on mobile phones paid during the year also drove the cost of sales up. In absolute terms, gross profit grew by 155.77 percent in 2024, however, GP margin slid to 10.36 percent.

Administrative expense escalated by 35 percent in 2024 due to higher payroll expense incurred during the year as AIRLINK expanded its workforce from 191 employees in 2023 to 390 employees in 2024.

Distribution expense plummeted by 4.60 percent in 2024 due to lesser salaries expense incurred in the distribution network, lower advertising and promotion budget and considerably lower depreciation charge.

Other income stayed at the same level as recorded in 2023, however, it was conveniently offset by 499 percent higher other expense incurred in 2024 due to higher provisioning done for WWF, WPPF, slow-moving and obsolete stocks. Moreover, loss on disposal of TFCs and operating fixed assets also drove other expense up in 2024.

AIRLINK recorded 215.59 percent stronger operating profit in 2024 with OP margin rising up to 8 percent. Finance cost mounted by 81.42 percent in 2024 due to higher discount rate and tremendous rise in the company’s short-term borrowings to meet its working capital requirements.

AIRLINK’s gearing ratio bounced back to 32 percent in 2024. The company recorded net profit of Rs.3059.34 million in 2024, up 242 percent year-on-year. This translated into EPS of Rs. 7.74 and the highest ever NP margin of 5.44 percent.

In 2025, AIRLINK recorded year-on-year dip of 0.26 percent in its topline which clocked in at Rs.56,135.42 million. At the start of the year, the government imposed 18 percent sales tax on mobile phones which took its toll on the market demand.

Capacity utilization stood at 65.42 percent resulting in the production of 785,039 headsets during the year.

Improvement in macroeconomic indicators particularly decline in inflation and stability of Pak Rupee enabled the company to reduce its cost by 2.33 percent in 2025. This resulted in 17.63 percent improvement in gross profit in 2025 with GP margin clocking in at its optimum level of 12.22 percent.

Administrative expense surged by 11.55 percent in 2025 due to higher payroll expense as the company expanded its workforce from 390 employees in 2024 to 671 employees in 2025. Distribution expense mounted by 15.51 percent in 2025 primarily on the back of higher salaries of sales force and increased travelling & conveyance charges incurred during the year.

What gave a considerable boost to AIRLINK’s bottomline in 2025 was 433.57 percent improvement in its other income which was the result of profit on saving accounts and a massive spike in mark-up income on loan to subsidiary. 54.24 percent decline in other expense in 2025 proved to be another favorable thing for the company. This was predominantly the consequence of lesser provisioning done for WWF, WPPF as well as low moving and obsolete stock.

The high-base effect due to loss on disposal of TFCs and operating fixed assets also resulted in a dip in other expense in 2025.

AIRLINK’s operating profit grew by 37 percent in 2025 with OP margin jumping up to 11 percent.

Finance cost surged by 57.65 percent in 2025 despite monetary easing. This was due to a spike in short-term borrowings as the company had to pay sales tax of 18 percent at the import stage which raised its working capital requirements. Gearing ratio escalated to 53 percent in 2025.

AIRLINK recorded net profit of Rs.3461.31 million in 2025, up 13.14 percent year-on-year. This translated into EPS of Rs.8.76 and NP margin of 6.17 percent.

Recent Performance (1QFY26)

AIRLINK’s topline ticked up by 2.17 percent in 1QFY26 to clock in at Rs.13,423.11 million. This appears to be the result of price optimization and change of sales mix. Cost of sales dropped by 1.57 percent during the period under consideration due to stability of Pak Rupee and controlled inflation. This enabled the company to attain 42.65 percent improvement in its gross profit in 1QFY26 with GP margin inching up to 11.80 percent versus GP margin of 8.45 percent recorded in 1QFY25.

Administrative expense posted a negligible year-on-year growth of 0.90 percent in 1QFY25 while distribution expense shrank by 24.88 percent due to dejected sales volume. Monetary easing appears to be the cause of shrunken other income in 1QFY26.

Moreover, the company’s saving accounts also drastically contracted in 1QFY26 which might have squeezed the profit on bank deposits. Other expense escalated by 33.50 percent in 1QFY26 seemingly due to increased provisioning done for WWF and WPPF.

AIRLINK recorded 56.64 percent higher operating profit in 1QFY26 with OP margin rising up to 9.41 percent from 6.14 percent in 1QFY25.

Despite monetary easing, finance cost multiplied by 16.76 percent in 1QFY26. Despite all the odds, the company’s ability to contain its cost and operating expenses allowed it to record 72.94 percent growth in its net profit in 1QFY26.

AIRLINK’s bottomline was recorded at Rs.608.34 million in 1QFY26 with EPS of Rs.1.54 versus EPS of Rs.0.89 recorded in 1QFY25. NP margin strengthened from 2.68 percent in 1QFY25 to 4.53 percent in 1QFY26.

Future Outlook

AIRLINK strategic partnership with Xiaomi TV and Acer Gadgets Inc. will strengthen its footprint in the local market. The company is already producing smart phones of renowned brands such as TCL, Tecno, alcatel, itel, Huawei, MI etc. With the aim to take optimum benefit of the growing urban population and technological consciousness, the company is not only enhancing its global partnerships to diversify its product mix but also expanding its distribution network, production capacity and geographical presence.

Comments

Comments are closed for this article.