Crescent Fibres Limited (PSX: CFL) was incorporated in Pakistan as a public limited company in 1977. The company is engaged in the manufacturing and sale of yarn.

Pattern of Shareholding

As of June 30, 2025, CFL has a total of 12.418 million shares outstanding which are held by 1412 shareholders. Local general public has the majority stake of 48.45 percent in the company followed by Directors, CEO, their spouse and minor children holding 36.98 percent of shares.

NIT & ICP accounts for 6.91 percent of CFL’s shares while joint stock companies hold 4.72 percent shares. Around 1.05 percent of the company’s shares are held by Banks, DFIs and NBFIs. The remaining shares are held by other categories of shareholders.

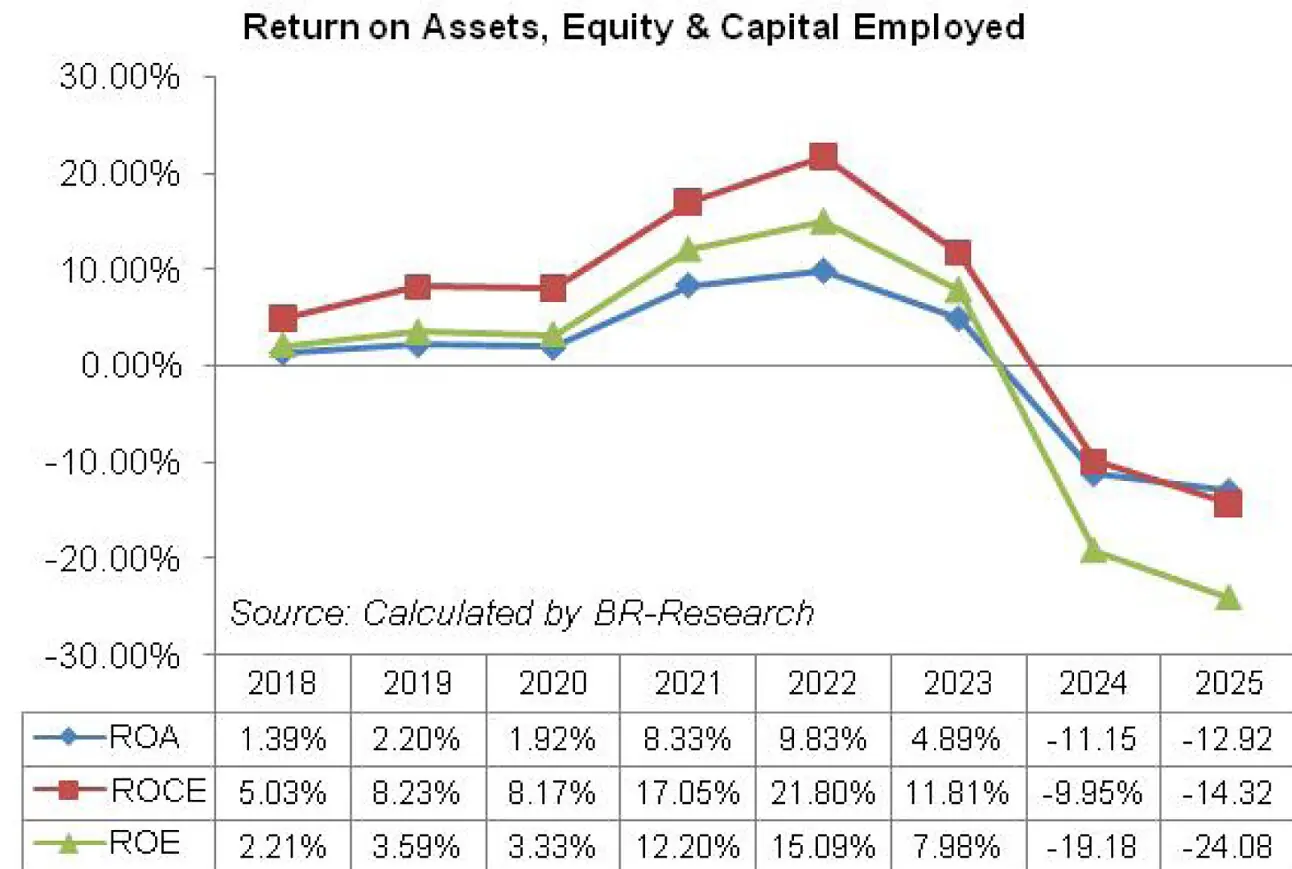

Historical Performance (2019-25)

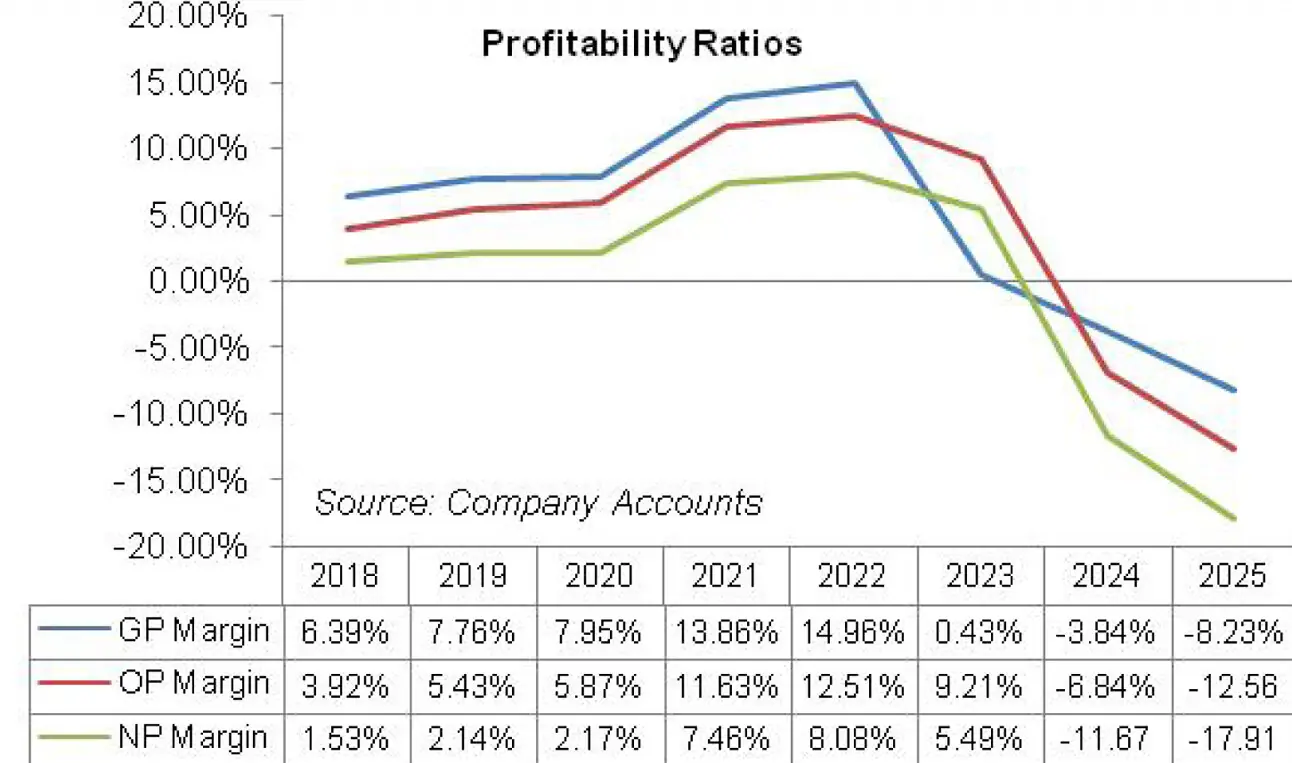

Over the period under consideration, CFL’s topline and bottomline slid in 2020, 2023, 2024 and 2025. In the last two years, the company also posted gross, operating and net losses. CFL’s margins strengthened until 2022 followed by a decline therafter. The detailed performance review of the period under consideration is given below.

In 2019, CFL’s net sales grew by 19.15 percent year-on-year to clock in at Rs.5289.441 million. This was mainly on account of higher product prices which led to an improved GP margin of 7.76 percent in 2019 versus GP margin of 6.39 percent recorded in 2018.

In absolute terms, gross profit grew by 44.67 percent in 2019. Distribution expense inched up by 4.57 percent in 2019 due to higher local freight & insurance charges incurred during the year. Administrative expense also climbed up by 11.41 percent in 2019 due to higher payroll expense on account of inflationary pressure and increase in number of employees from 1028 in 2018 to 1047 in 2019.

Other income expanded by 13 percent in 2019 mainly due to higher rental income. Gain on valuation of investment property, gain on sale of fixed assets and interest on bank deposits also contributed in driving up other income in 2019.

Other expense multiplied by 27.55 percent in 2019 due to higher profit related provisioning and loss on revaluation of investment. Operating profit rose by 65 percent in 2019 with OP margin jumping up from 3.92 percent in 2018 to 5.43 percent in 2019.

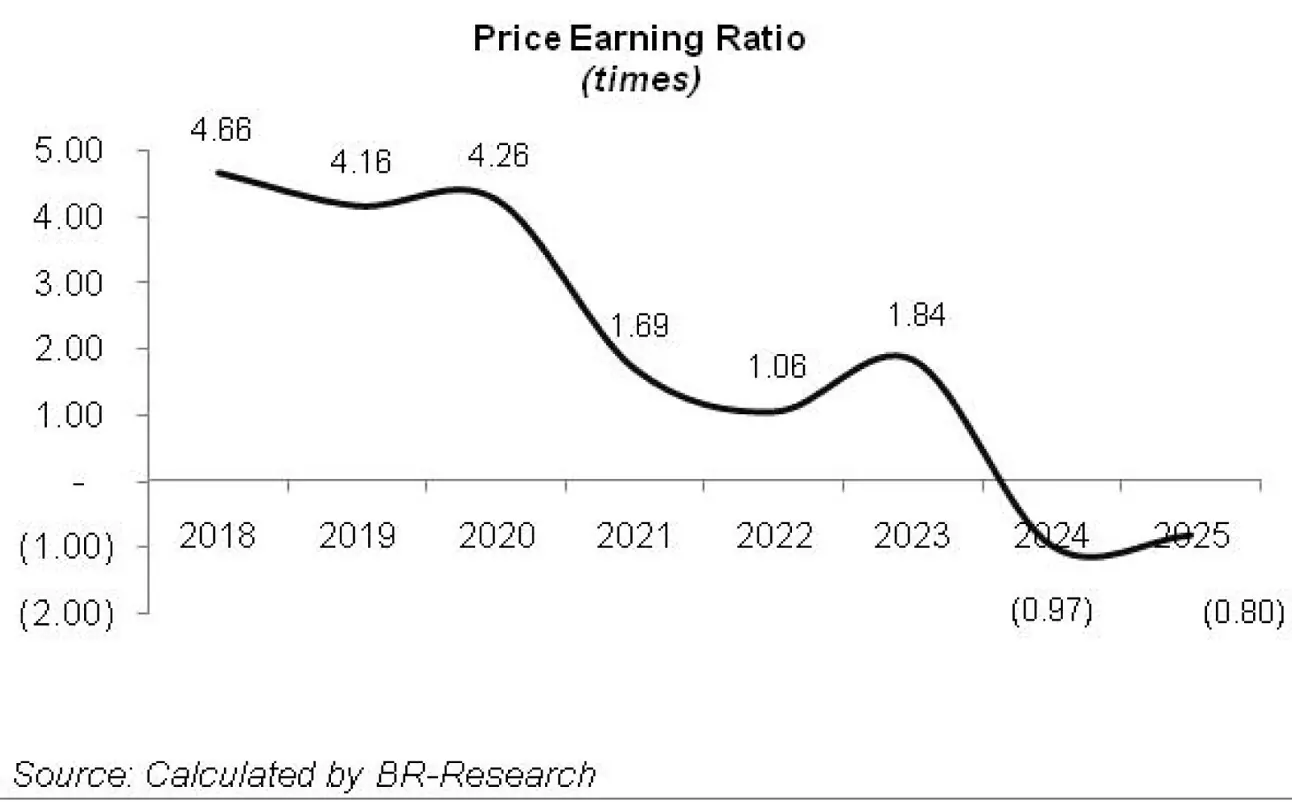

Finance cost surged by 53.82 percent in 2019 on the back of higher discount rate. CFL’s net profit posted 66.63 percent year-on-year growth in 2019 to clock in at Rs.113.194 million with EPS of Rs.9.12 versus EPS of Rs.5.47 recorded in 2018. NP margin also picked up from 1.53 percent in 2018 to 2.14 percent in 2019.

In 2020, CFL’s net sales slid by 5 percent year-on-year to clock in at Rs. 5023.57 million. This was due to reduced demand due to COVID-19 and a downtick in the prices of final product.

Cost of sales declined by 5.22 percent in 2020 which resulted in 2.70 percent shrinkage in gross profit. GP margin slightly grew to 7.95 percent in 2020. 1.10 percent decline in distribution expense in 2020 was the result of lower freight & insurance charges due to suppressed sales volume.

Conversely, administrative expense escalated by 10.27 percent in 2020 due to higher payroll expense while number of employees went down to 1039.

Other income multiplied by 125.51 percent in 2020 due to liabilities worth Rs.32.385 million written back during the year, higher rental income and elevated return on bank deposits recorded during the year.

In 2020, the company also booked allowance of Rs.26.342 million on ECL. Other expense slumped by 44.90 percent in 2020 as no loss on revaluation of investment was recorded during the year. Operating profit inched up by 2.71 percent in 2020 with OP margin rising up to 5.87 percent.

Finance cost escalated by 16 percent in 2020 due to increased short-term borrowings and elevated discount rate for most part of the year. Net profit tumbled by 3.91 percent in 2020 to clock in at Rs.108.77 million with EPS of Rs.8.76 and NP margin of 2.17 percent.

CFL’s topline expanded by 21.25 percent in 2021 to clock in at Rs. 6091.013 million. This was the result on demand recovery post COVID-19. Prices of final product also greatly improved during the year resulting in a staggering rise in GP margin to 13.86 percent. In absolute terms, gross profit strengthened by 111.36 percent in 2021.

Distribution expense hiked by 12.13 percent due to higher local freight & insurance charges on account of elevated sales volume. 3.88 percent year-on-year uptick in administrative expense in 2021 was on account of higher payroll expense which was partially offset by lower travelling & conveyance charges incurred during the year. Employee headcount also increased to 1062 in 2021.

Other income slid by 3.69 percent in 2021 due to high-base effect as CFL wrote off liabilities in the previous year.

The company booked 43.46 percent lower allowance for ECL in 2021. Other expense magnified by 268.45 percent in 2021 due to higher profit related provisioning booked during the year. CFL recorded 140 percent higher operating profit in 2021 with OP margin clocking in at 11.63 percent.

Finance cost tumbled by 19.12 percent in 2021 due to monetary easing as well as better liquidity position which resulted in a decline in external borrowings. CFL’s gearing ratio fell from 43 percent in 2020 to 18 percent in 2021. Net profit increased by 317.61 percent in 2021 to clock in at Rs.454.239 million with EPS of Rs.36.58 and NP margin of 7.46.

CFL recorded the highest topline growth of 32.95 percent in 2022. Net sales clocked in at Rs.8098.145 million in 2022. This was the consequence of greater sales volume and higher prices. Gross profit swelled by 43.54 percent in 2022 with GP margin attaining its highest level of 14.96 percent. Distribution expense ticked down by 4.66 percent in 2022 on account of bulk orders.

Administrative expense surged by 17.35 percent in 2022 on account of higher payroll expense as well as elevated travelling & conveyance charges incurred during the year. This was due to higher fuel charges and inflationary impact while number of employees was cut down to 1058 in 2022.

Other income declined by 28.52 percent in 2022 as no gain was recorded on the revaluation of investment property, extinguishment of original GIDC liability and sale of investment in 2022.

CFL booked 32.50 percent lesser allowance for ECL in 2022. Conversely, other expense mounted by 47.82 percent in 2022 due to higher provisioning done for WWF and WPPF. CFL posted 43 percent stronger operating profit in 2022 with the highest OP margin of 12.51 percent.

Finance cost soared by 19.88 percent in 2022 due to monetary tightening and increased utilization of short-term financing lines. Gearing ratio also inched up to 20 percent in 2022. Net profit enhanced by 44.14 percent to clock in at Rs.654.722 million in 2022 with EPS of Rs.52.72 and NP margin of 8.1 percent.

After the year of global pandemic, 2023 was the first year when CFL posted a plunge in its topline. This time around, the decline was more intense to the tune of 15.44 percent. This resulted in net sales of Rs.6847.57 million in 2023.

Not only did CFL’s net sales slid, but its GP margin drastically fell to 0.43 percent in 2023 versus the highest level of 14.96 percent recorded in the previous year. Sluggish demand resulted in curtailed capacity utilization which drove up the cost of fixed overhead per unit and didn’t allow the overall cost of sales to drop by more than 1 percent in 2023.

In absolute terms, gross profit slumped by 97.59 percent in 2023. Distribution expense grew by a massive 56.42 percent in 2023 on account of higher local freight & insurance charges due to higher fuel prices. 6.28 percent increased administrative expense incurred in 2023 was the consequence of higher payroll expense, directors’ remuneration and vehicle running & maintenance charges incurred during the year.

Due to demand destruction and curtailed capacity utilization, CFL cut down its workforce by 36 employees to bring down the tally to 1022 employees.

Massive rise of 1345.23 percent in other income in 2023 was attributable to fair value gain on investment property designated as “held for sale” due to tighter operations.

Allowance for ECL also multiplied by 249.85 percent to clock in at its highest level of Rs.35.174 million in 2023. Other expense was tapered off by 87.45 percent in 2023 as no provisioning was done for WPPF along with much lesser provisioning for WWF done during the year.

Operating profit thinned down by 37.7 percent in 2023 with OP margin clocking in at 9.21 percent. OP margin of 9.21 percent recorded for 2023 was lesser than the OP margin recorded in the previous year, however, much bigger than the GP margin for the current year due to hefty other income.

Finance cost magnified by 105.3 percent in 2023 due to elevated discount rate and increased borrowings. Gearing ratio was pushed up to 25 percent in 2023. CFL posted 42.59 percent weaker net profit in 2023 to the tune of Rs.375.095 million with EPS of Rs.30.27 and NP margin of 5.5 percent.

CFL’s net sales dipped by 5.08 percent to clock in at Rs.6499.839 million in 2024. This was because of weaker demand during the year which forced the company to curtail its production. This resulted in low capacity utilization which didn’t allow the fixed cost to be absorbed efficiently, resulting in gross loss of Rs.249.321 million in 2024.

Distribution expense incurred in 2024 was 11.14 percent lesser than last year due to thinner sales volume. Conversely, administrative expense ticked up by 7 percent due to inflationary pressure which pushed up the payroll expense. This was despite the fact that the company streamlined its workforce from 1022 employees in 2023 to 900 employees in 2024.

Other income fell by 90 percent in 2024 due to high-base effect as the company recognized fair value gain on investment property in the previous year. Allowance for ECL also enlarged by 91.85 percent in 2024, mostly offsetting the other income. The company recorded operating loss of Rs.444.899 million in 2024.

Finance cost slid by 5.26 percent in 2024 due to decline in borrowings on account of halted production activities. It is to be noted that despite lesser outstanding borrowings in 2024, gearing ratio picked up from 25 percent in 2023 to 31 percent in 2024 due to tighter liquidity position. The company recorded net loss of Rs.758.435 million in 2024 which translated into loss per share of Rs.61.08.

In 2025 too, the demand of yarn was not encouraging enough. The company conducted trading sales of cotton and polyester during the year to sustain its topline. However, this didn’t prove to be fruitful, resulting in a drastic decline of 33.37 percent in the net sales of CFL which clocked in at Rs.4330.539 million in 2025.

Gross loss spiked by 42.95 percent to clock in at Rs.356.412 million in 2025. In line with lower sales volume, distribution expense fell by 14.72 percent in 2025.

Conversely, administrative expense inched up by 0.47 percent in 2025 due to higher payroll expense. This was despite the fact that the number of employees was considerably squeezed to 532 in 2025. Other income deteriorated by 10.80 percent in 2025 as no dividend income was recognized during the year and also because of lower interest income on saving deposits.

Allowance for ECL tapered off by 21 percent in 2025. CFL recorded 22.23 percent taller operating loss to the tune of Rs.543.799 million in 2025. Finance cost dipped by 26.83 percent in 2025 due to monetary easing. This was despite an increase in the outstanding long-term loans during the year which translated into gearing ratio of 45 percent.

Higher long-term loans were not only to support the company’s BMR activities but also due to restructuring on its short-term loans due to financial difficulties. Net loss inched up by 2.28 percent to clock in at Rs.775.712 million in 2025 with loss per share of Rs.62.47.

Recent Performance (1QFY26)

CFL kicked off FY26 on a gloomy note with a radical fall of 34.64 percent in its topline which clocked in at Rs.1011.742 million in 1QFY26. Due to curtailed capacity utilization, the company recorded gross loss of Rs.7.96 million in 1QFY26 versus gross profit of Rs.19.945 million posted in 1QFY25.

Lesser sales volume and curtailed operation translated into 73.54 percent and 4.67 percent plunge in distribution expense and administrative expense in 1QFY26. Other income ticked up by a paltry 3.23 percent in 1QFY26 probably due to higher rental income. Operating loss surged by 130.73 percent in 1QFY26 to clock in at Rs.37.64 million.

Monetary easing and lesser outstanding borrowings pushed down finance cost by 42.56 percent in 1QFY26. Net loss tapered off by 19.28 percent to clock in at Rs.77.905 million in 1QFY26. This translated into loss per share of Rs.6.27 in 1QFY26 versus loss per share of Rs.7.77 posted in 1QFY25.

Future Outlook

Subdued demand will continue to take its toll on the topline of CFL. Lower demand may not allow the company to attain price rationalization resulting in weaker margins and unpleasant bottomline. The company must diversify its product offerings and focus on value added products to support its financial performance.

Comments

Comments are closed for this article.