Al-Khair Gadoon Limited (PSX: AKGL) was incorporated in Pakistan as a private limited company in 1990 and was converted into a public limited company in 1995.

The principal activity of the company is the manufacturing and sale of polyurethane foam and allied products including mattresses, sofa beds, furniture, pillows, bed sheets etc under the brand name “Five Star”.

Pattern of Shareholding

As of June 30, 2025, AKGL has a total of 10 million shares outstanding which are held by 337 shareholders. The company’s directors and CEO collectively account for 65.93 percent shares of AKGL followed by general public accounting for 16.21 percent shares of the company.

The spouse and minor children of directors and CEO have 14.75 percent stake in the company. Around 3 percent of AKGL’s shares are held by Banks, DFIs and NBFIs. The remaining ownership of the company is divided among other categories of shareholders.

Historical Performance (2019-25)

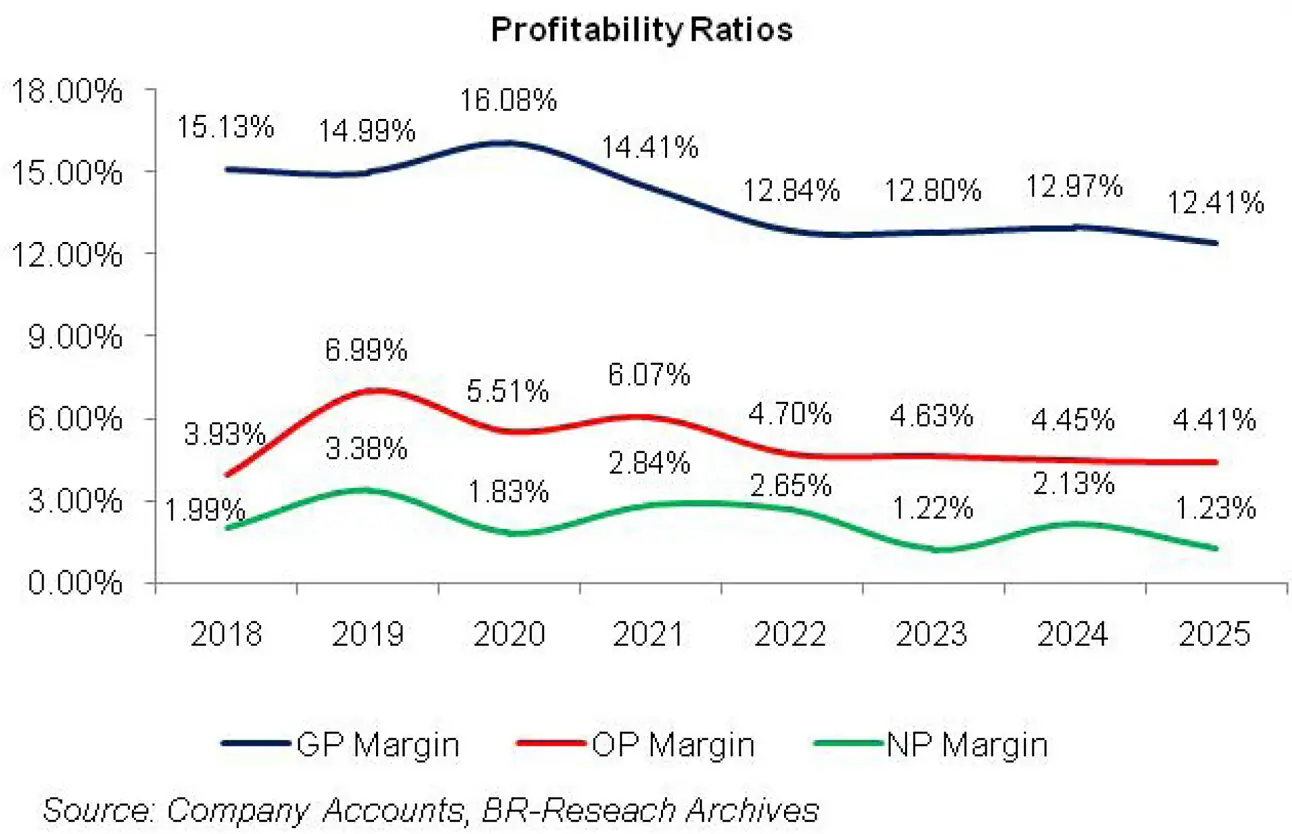

AKGL’s topline slid twice over the period under consideration i.e. in 2020 and 2023. Conversely, its bottomline dropped in three years i.e. in 2020, 2023 and 2025. AKGL’s margins have shown a cyclical pattern over the years; however remained range bound (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, AKGL’s topline rose by a splendid 55.18 percent year-on-year to clock in at Rs.574.52 million. This was the result of better sales volume, improved sales mix and full-year operations in 2019 versus 10 months operations in 2018 due to fire accident in the factory.

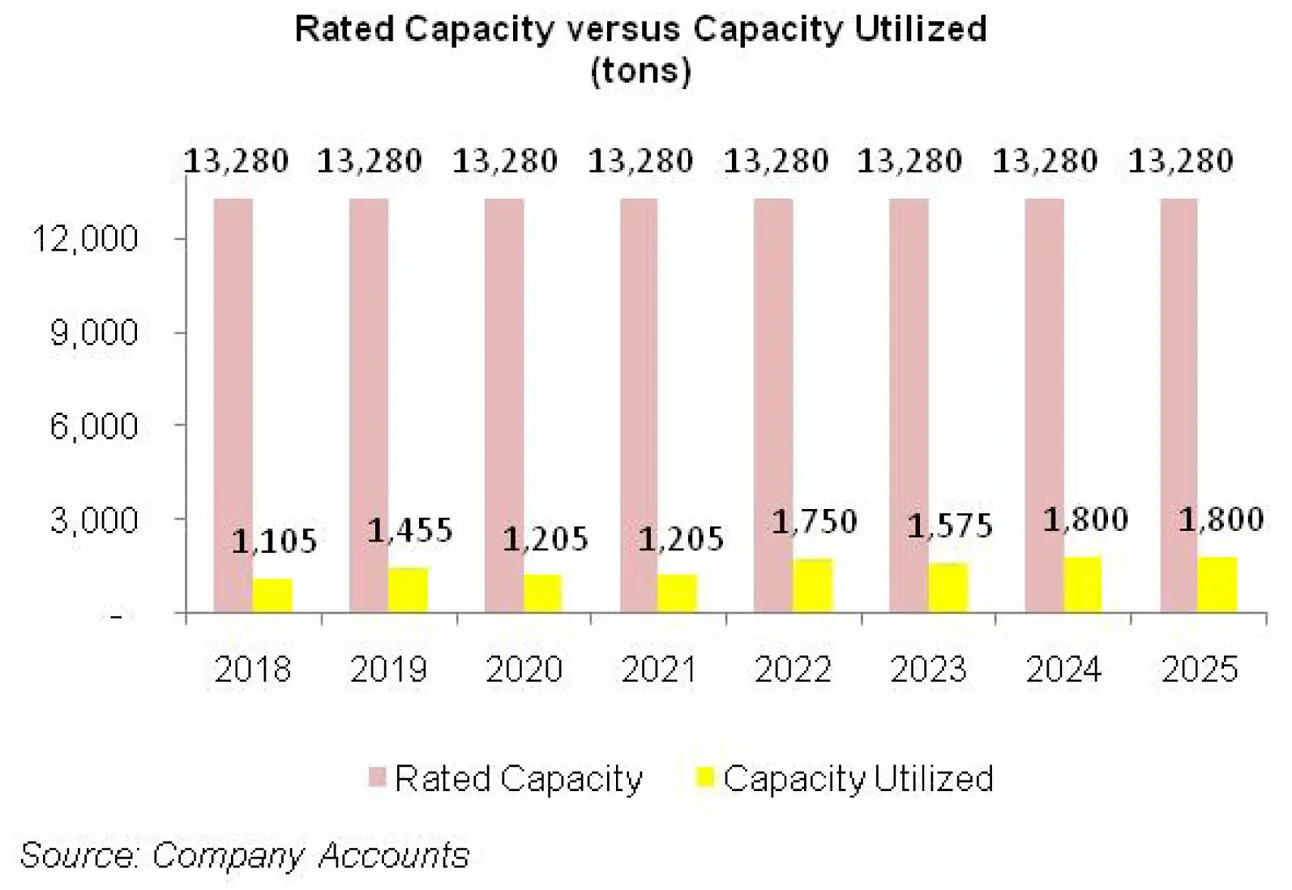

AKGL produced 1455 tons of products in 2019, up 32 percent from last year’s production volume due to rising demand. Cost of sales also escalated by 55.43 percent year-on-year as the cost of imported raw materials surged due to drastic depreciation in the value of local currency.

Gross profit improved by 53.77 percent in 2019, however, GP margin slightly fell from 15.13 percent in 2018 to 14.99 percent in 2019. Operating expense multiplied by 33.68 percent year-on-year in 2019 due to increase in payroll expense as well as advertisement and promotion budget.

The company posted net other expense of Rs.1.76 million in 2019, down 79 percent year-on-year. This was due to high-base effect as the company recorded loss on its fixed assets and materials due to fire accident in 2018. Operating profit rebounded by 176 percent year-on-year in 2019, culminating into OP margin of 7 percent versus OP margin of 3.93 percent recorded in 2018.

Finance cost surged by 265.94 percent in 2019 as the company increased its external borrowings for the import of raw materials and also because of higher discount rate. AKGL’s bottomline registered 162.90 percent growth in 2019 to clock in at Rs.19.39 million. This translated into EPS of Rs.1.94 in 2019 versus EPS of Rs.0.74 posted in 2018. NP margin also picked up from 2 percent in 2018 to 3.38 percent in 2019.

The incredible topline growth of 2019 was followed by a slide of 23.87 percent in 2020. AKGL’s net sales was recorded at Rs.437.36 million in 2020.

The decline in sales was the result of combination of fiscal measures undertaken by the government to boost tax revenue coupled with the breakout of COVID-19 and the associated lockdown which halted the production activities of the company.

AKGL’s production volume slumped by 17 percent year-on-year in 2020 to clock in at 1205 tons.

Cost of sales shrank by 24.85 percent year-on-year in 2020 due to hike in the prices of imported raw materials as well as Pak Rupee depreciation. Gross profit declined by 18.35 percent year-on-year in 2020, however, GP margin ticked up to 16 percent on account of rigorous cost control measures and better product mix.

Operating expense increased by only 7.30 percent year-on-year due to inflationary pressure. AKGL posted net other income of Rs.1.23 million in 2020 as it sold its fixed assets at a gain and booked lesser provisioning for WWF and WPPF.

Despite keeping a check on its cost and expense, operation profit plunged by 39.96 percent year-on-year in 2020 with OP margin slipping to 5.51 percent. Finance cost shrank by 34.63 percent year-on-year in 2020 on account of a drop in AKGL’s short-term borrowings.

Bottomline plummeted by 58.75 percent year-on-year in 2020 to clock in at Rs.8 million. This translated into EPS of Rs.0.8 and NP margin of 1.83 percent in 2020.

AKGL’s topline registered a robust turnaround in 2021 as it grew by 83.54 percent year-on-year to clock in at Rs. 802.75 million. This was due to upward revision in the prices and better sales mix. Production volume was recorded at 1205 tons, same as last year.

Cost of sales spiked by 87.20 percent year-on-year due to an increase in global commodity prices. GP margin marched down to 14.41 percent in 2021 despite 64.45 percent improvement in gross profit in absolute terms.

AKGL posted 38.17 percent hike in its operating expense in 2021 as the number of employees significantly increased from 179 in 2020 to 211 in 2021. Higher provisioning for WWF and WPPF translated into net other expense of Rs.1.39 million in 2021. Operating profit grew by 102 percent year-on-year in 2021 with OP margin jumping up to 6.10 percent.

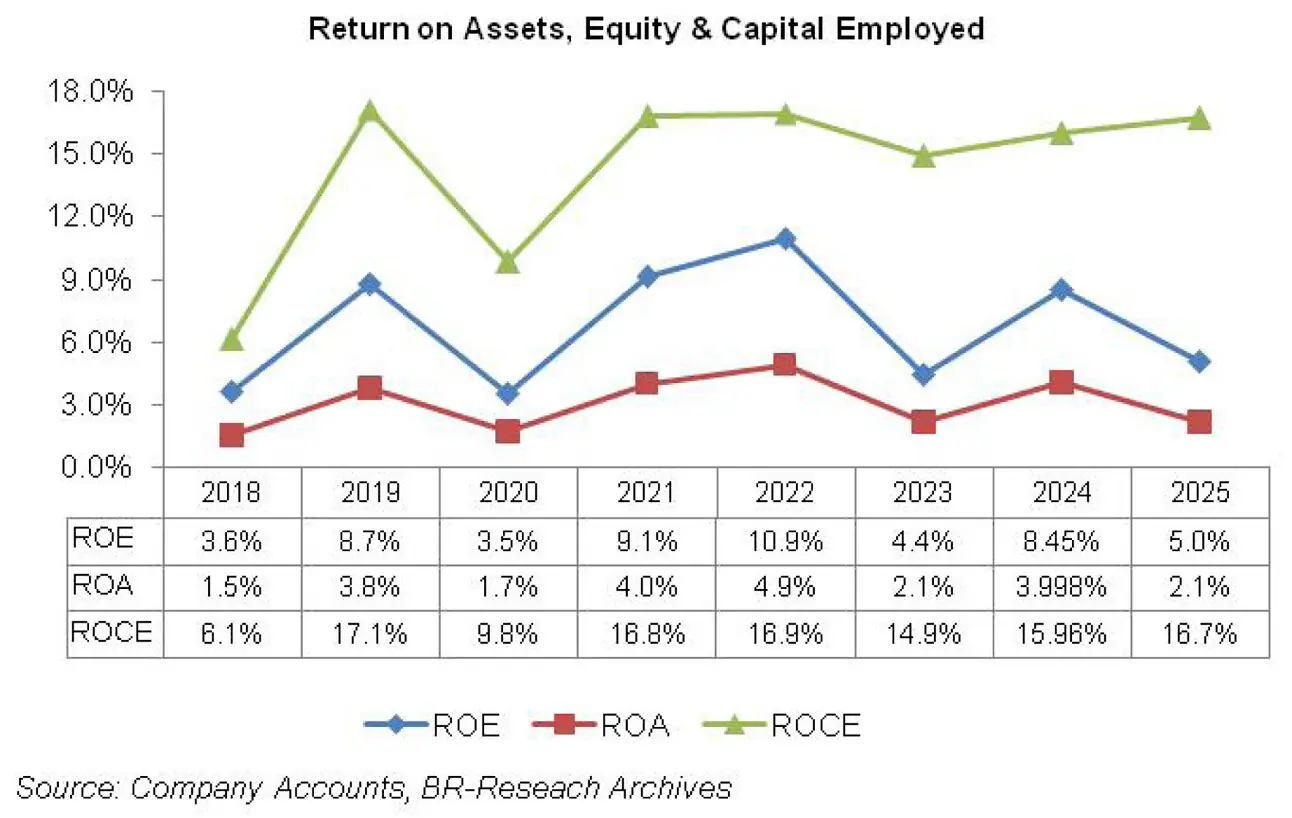

Finance cost ticked up by 5.29 percent year-on-year in 2021 despite discount rate cuts as the company obtained a long-term loan of Rs.14.45 million under SBP Refinance scheme for the payment of salaries and wages and also lease finance facility for plant and machinery. This coupled with twofold spike in short-term borrowings in 2021 when compared to 2020 drove up AKGL’s gearing ratio to 40 percent in 2021 versus gearing ratio of 26 percent in 2020.

Net profit augmented by 185.10 percent year-on-year in 2021 to clock in at Rs.22.81 million. This translated into an EPS of Rs.2.28 and NP margin of 2.84 percent in 2021.

In 2022, AKGL’s net sales outshone the previous year by 43.98 percent to clock in at Rs.1155.80 million. This was despite intense competition in the industry and high cost of materials due to Pak Rupee depreciation and high energy charge. The company’s production volume was recorded at 1750 tons, 45 percent higher than last year.

High cost of sales resulted in the erosion of gross margin which clocked in at 12.84 percent in 2022 despite 28.33 percent taller gross profit recorded by AKGL in absolute terms. Operating expense spiked by 39.44 percent year-on-year in 2022 primarily due to exorbitant rise in utility charges, travelling and conveyance charges as well as advertisement and promotional expense.

Net other expense posted 91 percent hike in 2022 on account of higher provisioning for WWF and WPPF.

Operating profit picked up by 11.57 percent in 2022 while OP margin slumped to 4.7 percent. Despite multiple rounds of monetary tightening in 2022, AKGL was able to squeeze its finance cost by 1.33 percent in 2022 due to lower bank commission charges. Net profit grew by 34 percent year-on-year in 2022 to clock in at Rs.30.57 million with EPS of Rs.3.06 and NP margin of 2.65 percent.

AKGL’s net sales couldn’t sustain the economic and political headwinds and lost its grounds by 8 percent to clock in at Rs. 1063.50 million in 2023. The company’s production declined by 10 percent year-on-year in 2023 to clock in at 1575 tons. This was on account of reduced demand due to shrunken pockets of consumers owing to inflationary pressure.

Cost of sales also plummeted by 7.94 percent, resulting in a static GP margin of 12.80 percent in 2023. Operating expense inched down by 5.65 percent year-on-year in 2023 as the company significantly compressed its entertainment, advertisement and staff welfare expense.

Net other expense shrank by 78.45 percent in 2023 as the company booked lower provisioning for WWF and WPPF and earned income from bank deposits. Despite rigorous measures to drive down its cost and expense, AKGL couldn’t stop its operating profit from sliding down by 9.35 percent in 2023. OP margin marginally dropped to 4.63 percent in 2023.

Finance cost proved to be the Achilles heel for the company as it surged by 186.26 percent in 2023 on account of high discount rate. This was despite the fact that the company reduced its borrowings its 2023 which pushed down its gearing ratio to 24.85 percent from gearing ratio of 40.39 percent recorded in 2022.

Net profit eroded by 57.41 percent year-on-year in 2023 to clock in at Rs.13.02 million with EPS of Rs.1.3 and NP margin of 1.224 percent – the lowest among all the years under consideration.

In 2024, AKGL’s topline progressed by 20.22 percent year-on-year to clock in at Rs1278.49 million. This was on account of improved sales volume as well as sales value. Production grew by 14 percent year-on-year to clock in at 1800 tons in line with demand growth.

While high energy tariff, inflation and high material prices continued to pose challenges to the company, however, stability in the value of local currency of-late and price rationalization resulted in 21.83 percent year-on-year improvement in the company’s gross profit with GP margin ticking up to 12.97 percent.

Operating expense surged by 32.23 percent in 2024 which was the result of drastic spike in utility charges and payroll expense incurred during the year.

The company cut down its workforce from 200 employees in 2023 to 190 employees in 2024. During the year, the company recorded net other income of Rs.5.14 million as against net other expense recorded for the past three years. This was predominantly the result of superior mark-up income from bank deposits.

AKGL’s operating profit picked up by 15.47 percent in 2024 with OP margin slightly ticking down to 4.45 percent.

The company was able to cut down its finance cost by 30.67 percent in 2024 despite high discount rate. Net profit mounted by 109.30 percent in 2024 to clock in at Rs.27.25 million with EPS of Rs.2.73 and NP margin of 2.13 percent.

In 2025, AKGL’s topline posted year-on-year growth of 9.43 percent to clock in at Rs.1399.04 million. This mainly came on the back of upward price revision to account for higher cost of sales. Production remained intact at 1800 tons in 2025. Cost of sales escalated by 10.13 percent in 2025 on account of higher labor cost, energy cost and cost of imported raw materials.

Gross profit ticked up by only 4.72 percent in 2025, however, GP margin ticked down to 12.41 percent. Number of employees was reduced from 190 in 2024 to 165 in 2025, however, inflationary pressure led to higher payroll expense during the year.

However, elevated payroll expense was counterbalanced by lower utility charges resulting in no significant movement in operating expense in 2025. Other expense shrank by 41.33 percent in 2025 due to lower provisioning done for WPPF and no loss incurred on the disposal of assets in. Other income also plunged by 52.41 percent in 2025 on account of lower mark-up income on bank deposits and no miscellaneous income recognized during the year.

AKGL recorded net other income of Rs.1.98 million in 2025, down 61.56 percent year-on-year. Operating profit inched up by 8.53 percent in 2025 with OP margin staying intact at 4.41 percent.

Despite monetary easing, finance cost mounted by 85.74 percent in 2025. This was due to increased short-term borrowings for the import of raw materials which led the gearing ratio surge to 52.02 percent in 2025. This led to 37 percent deterioration in AKGL’s net profit which was recorded at Rs.17.145 million in 2025. This resulted in EPS of Rs.1.71 and NP margin of 1.23 percent in 2025.

Recent Performance (1QFY26)

During the first quarter of FY26, AKGL posted a year-on-year dip of 1.77 percent in its topline which clocked in at Rs.277.79 million. This was due to lower sales volume due to withered purchasing power of its consumers.

Cost of sales couldn’t be controlled owing to increased input cost particularly elevated energy cost. This translated into 9.12 percent dip in gross profit in 1QFY26. GP margin fell from 12.10 percent in 1QFY25 to 11.19 percent in 1QFY26.

Inflationary pressure led to 42.41 percent escalation in administrative expense and 22.45 percent surge in distribution expense in 1QFY26.

Elevated operating expense might also be on the back of portfolio innovation measures undertaken by the management to add diversity to its revenue lines. Other income fell by a drastic 92.70 percent in 1QFY26 most certainly due to thinner mark-up income. AKGL posted 73.32 percent dip in its operating profit in 1QFY26 with OP margin clocking in at 1.39 percent versus OP margin of 5.10 percent posted in 1QFY25.

Finance cost tumbled by 4 percent in 1QFY26 due to monetary easing and lesser outstanding borrowings. The company posted net loss of Rs.10.21 million with loss per share of Rs. 1.02 in 1QFY26 versus net loss of Rs.0.13 million and loss per share of Rs.0.01 posted in 1QFY25.

Future Outlook

Sustained period of high inflation has considerably taken its toll on the sales volume of the company by reducing the purchasing power of local consumers. In such case, better trade partnering with customers, product mix management and superior pricing strategy through operational efficiency may result in improved demand.

International market for polyurethane foam is also showing great potential on account of rising demand of smart homes, focus on energy conservation and expanding automobile industry. AKGL may also capitalize on the enlarging global market to offset muted demand in the home market.

Comments

Comments are closed for this article.