The central bank continues to act with reason and prudence. Afterall, there is no space for a rate cut when inflation has stopped falling and currency pressures remain unresolved. What is more revealing is that it had no other option. Without fiscal reform, monetary policy has reached its limit.

The institution did its part. It stabilized markets after a near-run on reserves two years ago, absorbed political interference, and brought some order back to monetary management. It earned credibility by staying consistent when few others did. But firefighting is not a growth plan.

Once the immediate danger passes, the same tools that saved the system start to weigh it down. Pakistan has now entered that phase.

The new mandate prevents the central bank from doing what politicians once demanded of it. It cannot stimulate the economy through cheap liquidity or backstop deficits disguised as “temporary support.” Those days are gone. Yet the fiscal side remains trapped in the same habits that caused the last crisis.

Islamabad refuses to let the currency find its level. Imports are still policed, and stability has become a substitute for direction. Policy is no longer trying to reach anywhere. It is only trying to hold still.

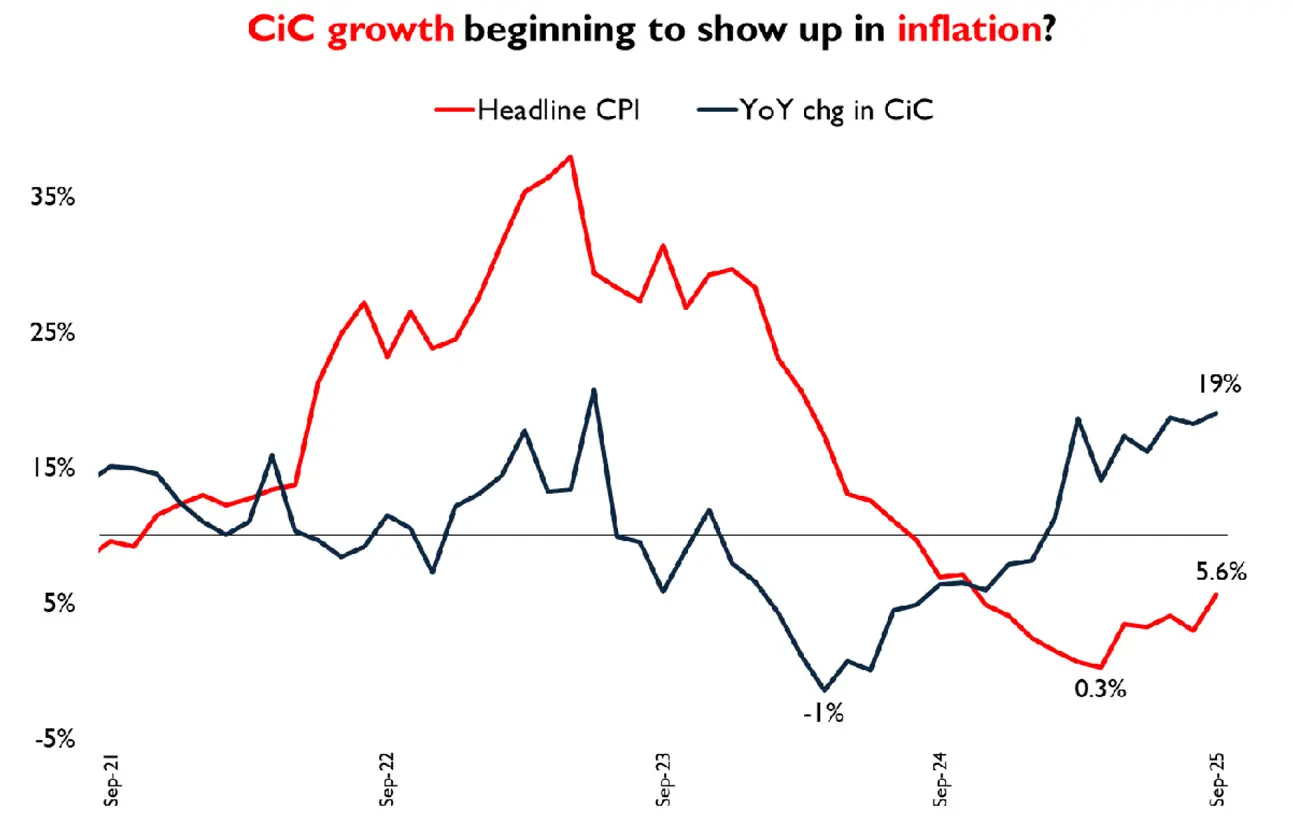

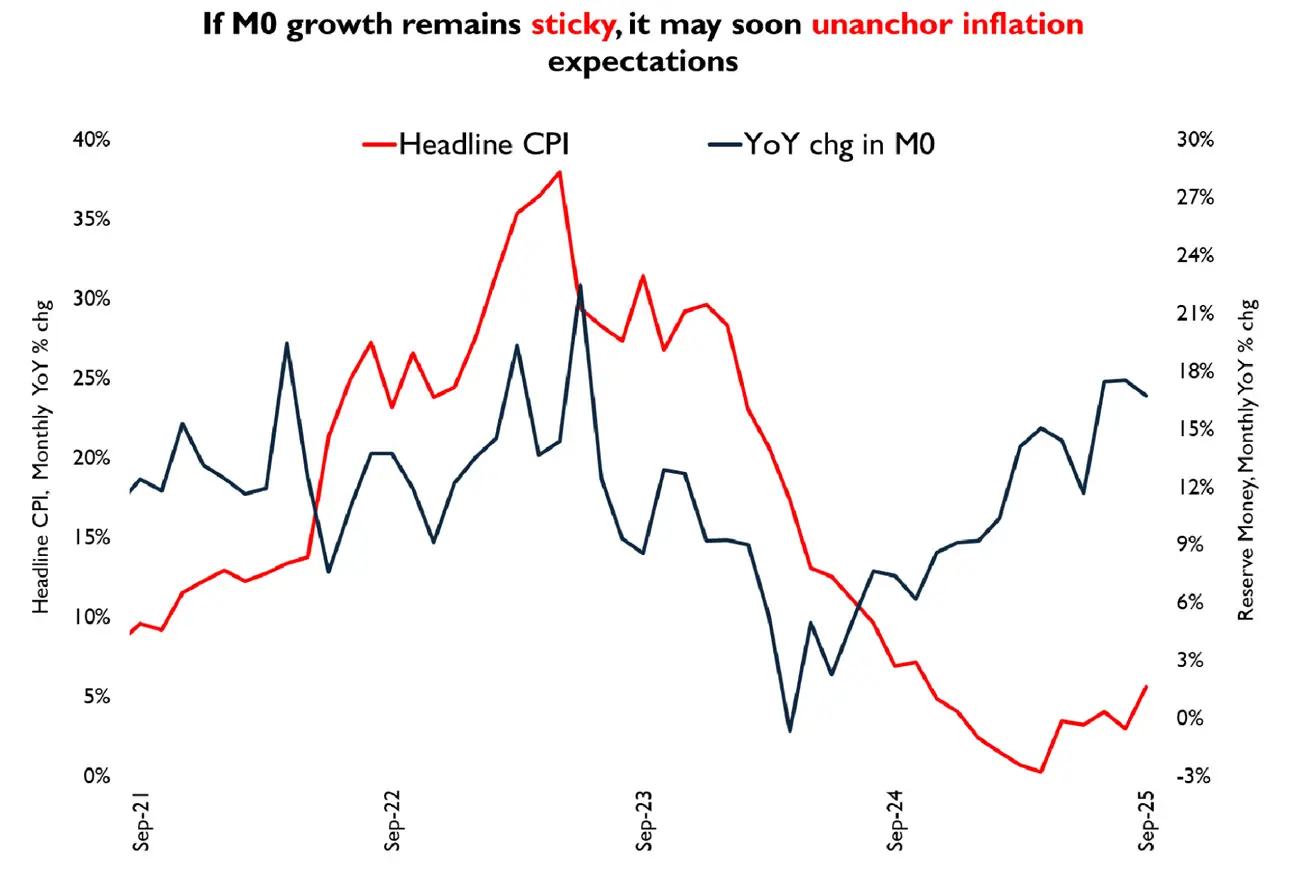

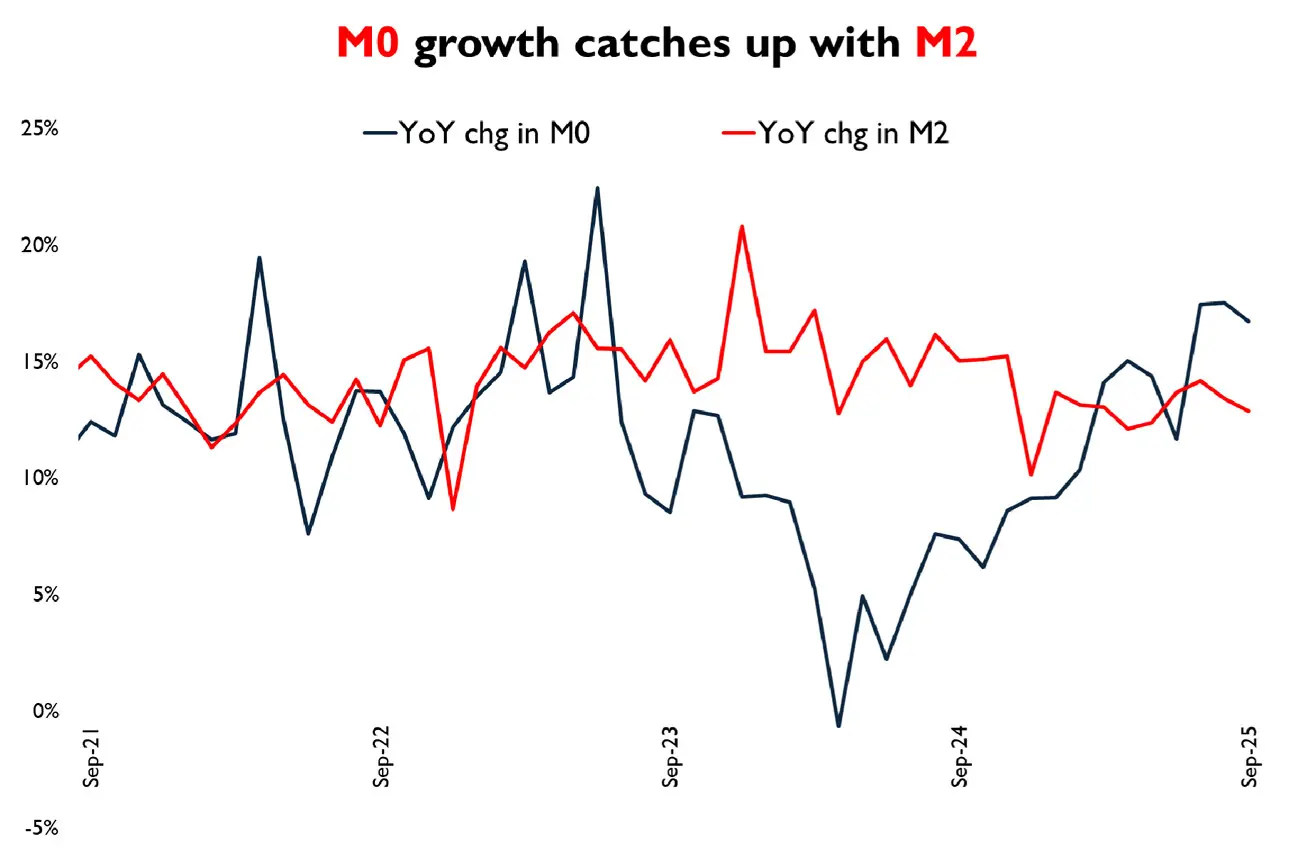

That would be defensible if the fundamentals supported it. Instead, broad money continues to grow in double digits. Currency in circulation has surged almost one-fifth over the year.

Deposits have stagnated. Reserve money remains high. This is not a liquidity shortage. It is a system with too much idle cash and no productive outlet. High rates coexist with loose money because the underlying economy is neither tightening nor expanding. It is drifting.

The result is a shallow equilibrium that looks calm but achieves nothing. Inflation is contained but not defeated. Growth is muted but not alarming. The exchange rate is steady but only because it is being held there. It is an economy running in place, performing stability without progress.

Policymakers can claim that inflation is within target and reserves are improving. But behind that narrative lies a credit system frozen by risk, and a fiscal machine that still cannot live within its means.

This is what happens when one side reforms and the other refuses. The central bank has been turned into a custodian of paralysis. It can watch the aggregates, adjust liquidity windows, and publish statements of restraint. It cannot set a new course when fiscal side contradicts every principle of market discipline. Both federal and provincial administrations remain addicted to control: currency, of prices, optics. SBP remains constrained by its own prudence. Between them sits an economy that neither side is willing to own.

This is not crisis, but it is not recovery either. It is suspension. The numbers do not show collapse because the controls are still in place. But the policy framework has lost its sense of purpose. Each quarter now looks like the last: modest growth, cautious optimism, and the same cycle of self-congratulation for avoiding a disaster that never ends. The system survives but does not reform. It stabilizes, tightens, waits, and repeats.

The real danger is that this becomes normal. An economy can survive volatility if it learns from it. It cannot live with inertia. The idea that macro stability is itself the goal has replaced the question of what comes after it. The central bank cannot answer that question. Its mandate ends where fiscal reform should begin. Until that bridge is built, the policy rate will stay high, liquidity will stay loose, and the economy will stay stuck.

The pause was necessary. But it also exposes the vacuum. Monetary policy has done its part. The next move must come from the fiscal side. Without it, the economy will remain in the same holding pattern: stable on paper, stagnant in reality, waiting for the next shock to decide what to do next.

Comments

Comments are closed for this article.