Matco Foods Limited (PSX: MFL) was established as Matco Rice Processing Private Limited in 1964. The company was incorporated in Pakistan as a private limited company in 1990.

The company is principally engaged in the processing and export of rice, rice protein, rice glucose, pink salt, condiments and spices, dessert mixes etc. MFL is one of the largest rice exporters of the country with exports of its flagship brand “Falak” in over 65 countries across the globe.

Pattern of Shareholding

As of June 30, 2024, MFL has 122.4 million shares outstanding which are held by 1960 shareholders. Directors, their spouse and minor children have the majority stake of around 41.6 percent in MFL followed by associated companies, undertakings and related parties holding 35 percent shares of the company.

Local general public accounts for 17.11 percent shares of the company. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

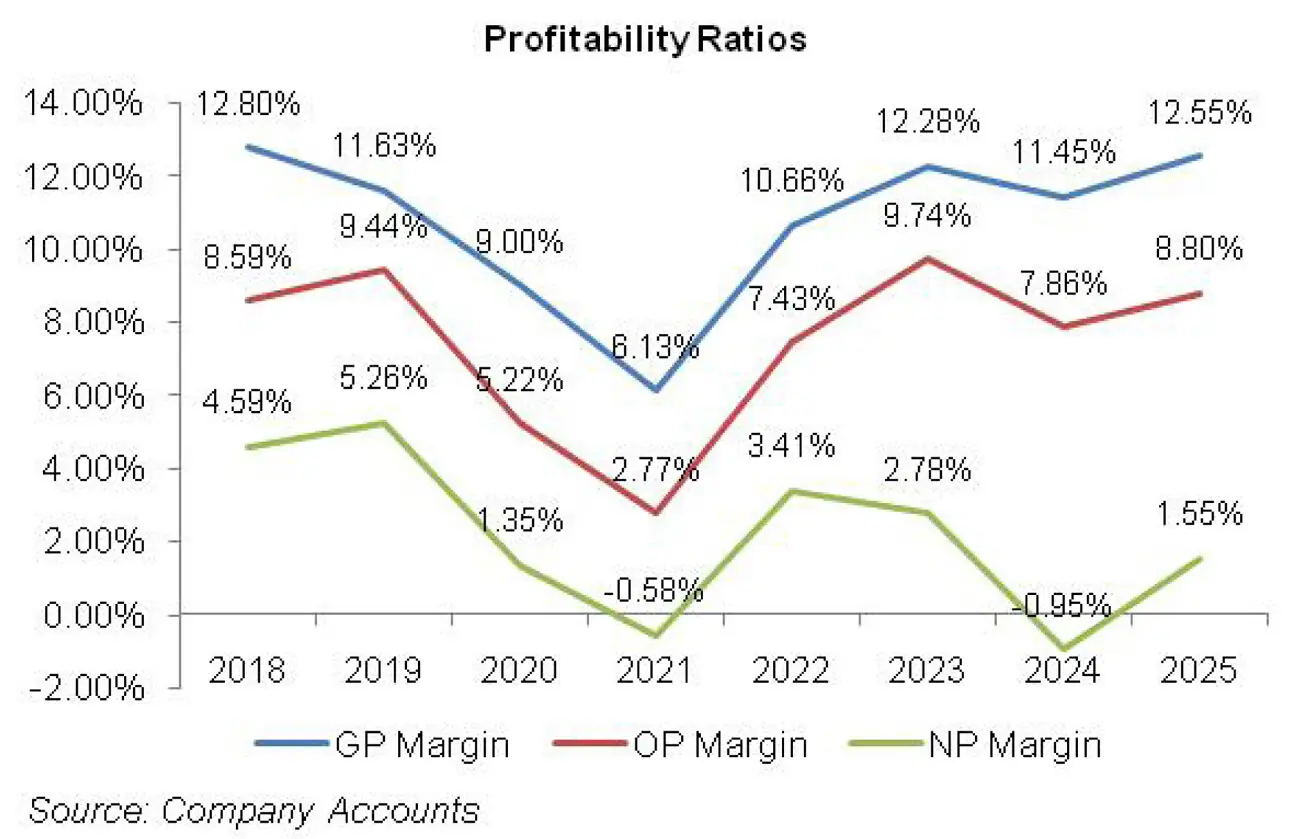

Except for a marginal dip in 2021 and 2025, the topline of MFL rode an uphill journey over the period under consideration.

MFL’s bottomline registered growth in 2019, followed by a slump in 2020 and 2021 with net loss registered in the latter year. MFL’s bottomline recovered from net loss in 2022 and further strengthened in 2023. In 2024, the company recorded net loss yet again. In 2025, the bottomline was recorded in the positive territory.

MFL’s margins declined until 2021 except for an uptick in its net and operating margins in 2019. In 2022, the margins considerably rebounded. In 2023, gross and operating margin picked up further while net margin fell. This was followed by a slump in all the margins in 2024.

In 2025, MFL’s margins registered sound growth. The detailed performance review of the period under consideration is given below.

In 2019, MFL posted 16.96 percent year-on-year rise in its topline which clocked in at Rs.7863.05 million. The growth mainly came on the back of export sales on account of higher commodity prices in the international market coupled with Pak Rupee depreciation.

Besides, export sales volume also inched up by 2.45 percent in 2019. High cost of sales on the back of inflation, elevated energy prices and high commodity prices contracted GP margin from 12.80 percent in 2018 to 11.63 percent in 2019 despite 6.25 percent year-on-year improvement in its gross profit.

Distribution expense grew by 4.91 percent year-on-year in 2019. Lower payroll expense, allowance for ECL and shop rent diluted the effect of hike in the sales promotion and export charges incurred during the year.

Administrative expense spiked by 21.32 percent year-on-year in 2019 on account of higher payroll expense as the company increased its workforce from 673 employees in 2018 to 729 employees in 2019 on account of installation of rice glucose plant (phase 2).

Other income mounted by a massive 497.55 percent in 2019 as MFL recognized gain on sale of property, plant and equipment in 2019.

The company also recorded 109.91 percent higher exchange gain in 2019 due to relentlessly declining value of local currency Operating profit picked up by 28.50 percent in 2019 with OP margin growing from 8.59 percent in 2018 to 9.44 percent in 2019.

Finance cost escalated by 14.93 percent year-on-year in 2019 on the back of higher discount rate and increased borrowings. Gearing ratio surged from 47 percent in 2018 to 50 percent in 2019.

Net profit picked up by 34.24 percent year-on-year in 2019 to clock in at Rs.413.84 million. EPS grew from Rs.2.96 in 2018 to Rs.3.38 in 2019. NP margin also improved from 4.6 percent in 2018 to 5.26 percent in 2019.

In 2020, MFL’s sales to commercial industry such as hotels, tourism, restaurants etc came to a halt due to restriction on the movement of people and goods on account of COVID-19. Moreover, curtailed Hajj season also badly affected the export sales of the company in that region.

On the flipside, home-based consumption took a huge flight as people started stockpiling food and grocery items globally. Striking sales in the home-based industry bypassed the sluggish demand in the commercial industry, culminating into 43.58 percent year-on-year topline growth in 2020.

MFL’s net sales reached Rs.11,289.96 million mark in 2020. However, supply chain disruptions, high freight rates, Pak Rupee depreciation and increase in the prices of imported raw materials resulted in an increase in the cost of sales which squeezed the GP margin to 9 percent in 2020. Then restrictions on the movement of goods, containers shortage and spiraling ocean freight rates magnified export charges and commissions which pumped up the distribution cost by 28.58 percent year-on-year in 2020.

Administrative expense inched up by 12.91 percent year-on-year in 2020 on account of higher payroll expense as number of employees grew to 809 in 2020. Other income couldn’t lend the helping hand either and lost its ground by 47 percent year-on-year in 2020 due to high-base effect.

MFL also took a massive hit of 90.84 percent on the exchange gain front due to extreme volatility of exchange rates. This resulted in 20.66 percent plunge in operating profit with OP margin ticking down to 5.22 percent.

Finance cost grew by 27.14 percent in 2020 as discount rate was high in the first three quarters of 2020 coupled with increased working capital requirements of the company. Bottomline dipped by 63.29 percent year-on-year in 2020 to clock in at Rs.151.93 million with NP margin of 1.35 percent and EPS of Rs.1.24.

2021 proved to be even gloomier for MFL than the previous year as not only did its topline plummet by 6.50 percent to clock in at Rs.10,556.62 million, it also registered net loss.

While the global economy started showing signs of recovery post COVID-19, MFL faced hard time mustering export sales as freight charges grew by as high as 5 times in most of the export destinations of the company.

This severely affected the export sales of the company which dropped by 21 percent year-on-year in terms of volume to clock in at 41,066 MT in 2021. This resulted in a thinner GP margin of 6.13 percent in 2021. Low export sales reduced the distribution cost by 10.16 percent year-on-year on account of lower travelling, sales promotion and export charges.

Administrative expense registered 14.12 percent year-on-year growth in 2021 on account of higher payroll expense, provision for GIDC as well as elevated fee and subscription charges.

Other income and exchange gain performed really well during the year with year-on-year growth of 36.30 percent and 365.32 percent respectively. Higher other income was the result of gain on sales of operating fixed assets during the year while exchange gain was the result of exchange rate stability.

Operating profit tapered off by 50.34 percent in 2021 with OP margin drastically falling down to 2.77 percent.

Finance cost contracted by 22.11 percent in 2021 as low export orders meant lower working capital requirements and lesser short-term borrowings coupled with low discount rate during the year. The company registered net loss of Rs.60.87 million in 2021 with loss per share of Rs.0.50.

MFL recorded year-on-year growth of 17.23 percent in its topline which clocked in at Rs.12,375.92 million 2022. The margins which had been shrinking since 2019 gained back their momentum in 2022. This was on the back of improved export sales volume (42,114 MT), inventory gains and increase in average prices of rice glucose products.

GP margin was recorded at 10.66 percent in 2022 with 103.93 percent rise in gross profit in absolute terms. Distribution expense mounted by 23.27 percent year-on-year in 2022 on account of increased sales promotion as well as higher export charges and commission.

Administrative expense enlarged by 15.10 percent year-on-year in 2022 on account of higher payroll expense as the number of employees grew from 708 in 2021 to 750 in 2022 and also because of higher taxes, duty and fee paid during the year.

Exchange gain posted year-on-year growth of over 200 percent in 2022. Other income slid by 74.31 percent in 2022 due to high-base effect as the company recorded massive gain on sale of operating fixed assets in 2022.

Operating profit magnified by 214.32 percent in 2022 with OP margin jumping up to 7.43 percent. MFL recorded 42.17 percent higher finance cost in 2022 on the back of higher discount rate and increased short-term borrowings. 35.2 percent higher taxation incurred during the year was due to the imposition of super tax.

MFL posted net profit worth Rs.422.42 million in 2022 with NP margin of 3.41 percent and EPS of Rs.3.45.

With 61.50 percent year-on-year rise in net sales, 2023 proved to be the year of financial brilliance for MFL.

Net sales clocked in at Rs.19,985.40 million in 2023. While the company’s export off-take slid to 32,829 MT in 2023, down 22 percent year-on-year, Pak Rupee depreciation and increase in export prices of rice from USD 981 in 2022 to USD 1220 per ton in 2023 greatly improved the net sales of the company. This, coupled with the gain in inventory value resulted in 85.88 percent year-on-year growth in MFL’s gross profit in 2023 with GP margin touching its 5-year high value of 12.28 percent in 2023.

Distribution and administrative expense mounted by 54.91 percent and 58.36 percent respectively in 2023. Elevated distribution expense was on the back of higher travelling expense, sales promotion and export commission incurred during the year.

Higher administrative expense was the consequence of escalated payroll expense as MFL hired 219 new employees during the year which took the total employee count to 969 in 2023. MFL performed quite well in terms of other income and exchange gain which grew by 171.33 percent and 103.81 percent respectively in 2023.

MFL recorded 111.77 percent higher operating profit in 2023, translating into an improved OP margin of 12.28 percent. Finance cost surged by 204.83 percent in 2023 on account of record higher discount rate coupled with increased external borrowings during the year.

Gearing ratio escalated from 55 percent in 2022 to 58 percent in 2023. This coupled with additional super tax imposed during the year somewhat diluted the bottomline growth. MFL’s net profit rose by 31.53 percent year-on-year in 2023 to clock in at Rs.555.618 million with EPS of Rs.4.54. NP margin eroded to 2.78 percent in 2023.

MFL’s net sales surged by 38.58 percent to clock in at Rs.27,695.67 million in 2024. While soaring inflation, high interest rates and challenging economic and political conditions took its toll on the purchasing power of consumers leading to constricted local demand, stronger net sales were driven by 25 percent higher rice exports achieved by the company during the year.

High cost of sales resulted in a thinner GP margin of 11.45 percent in 2024 despite 29.26 percent higher gross profit in absolute terms. Distribution expense mounted by 66.31 percent in 2024 on the back of higher export charges and sales promotion expense incurred during the year.

Administrative expense also surged by 20.73 percent in 2024 predominantly due to higher payroll expense on account of inflationary pressure and also because of workforce expansion from 969 employees in 2023 to 1006 employees in 2024.

Other income boasted 60.86 percent year-on-year growth in 2024 on the back of higher scrap sales. MFL recorded 53.83 percent lower exchange gain in 2024.

Operating profit ticked up by 11.79 percent in 2024, however, OP margin dipped to 7.86 percent.

Finance cost enlarged by 89.78 percent in 2024 due to higher discount rate and higher working capital related borrowings. MFL recorded net loss of Rs.262.46 million in 2024 with loss per share of Rs.2.14.

Recent Performance (2025)

In 2025, MFL’s topline dipped by 3.76 percent to clock in at Rs.26,654.38 million. This was due to stability in the value of local currency and the decline in commodity prices in the international market.

Conversely, MFL’s export volumes demonstrated resilience in 2025. Focused raw material procurement and better absorption of fixed cost resulted in 5.53 percent uptick in gross profit in 2025 with GP margin marching up to its optimum level of 12.55 percent. Distribution expense inched down by 10.34 percent in 2025 due to lesser budget allocated for advertisement and promotion.

Administrative expense escalated by 19.93 percent in 2025 due to inflationary pressure, increase in compliance cost and the company’s ongoing investment in improving its technology, governance and human resources. Efficient utilization of financial assets resulted in 4.27 percent uptick recorded in other income in 2025.

Exchange gain also strengthened by 51.88 percent in 2025. MFL recorded 7.76 percent higher operating profit in 2025 with OP margin jumping up to 8.80 percent.

Finance cost tapered off by 17.37 percent in 2025 due to lower discount rate. MFL posted net profit of Rs.413.897 million in 2025 with EPS of Rs.3.38 and NP margin of 1.55 percent.

Future Outlook

MFL has a strong presence in the international market with robust volumes and efficient supply chain management.

While demand remains strong, higher cost of sales and stability of Pak Rupee can slash the company’s margins. Besides, adverse weather conditions will also continue to pose challenges to the quality and quantity of the company’s output.

Comments

Comments are closed for this article.