Privatisation of DISCOs is key, but is the environment conducive?

The government wants to pursue the privatisation of some of its ‘profitable’ power distribution companies, keeping in line with its commitment to the International Monetary Fund (IMF).

Detractors of privatisation may use some arguments, but the fact is that there will be few who would want the government more involved in private business, least of all, the complex power sector, where there are two very distinct tales of earnings.

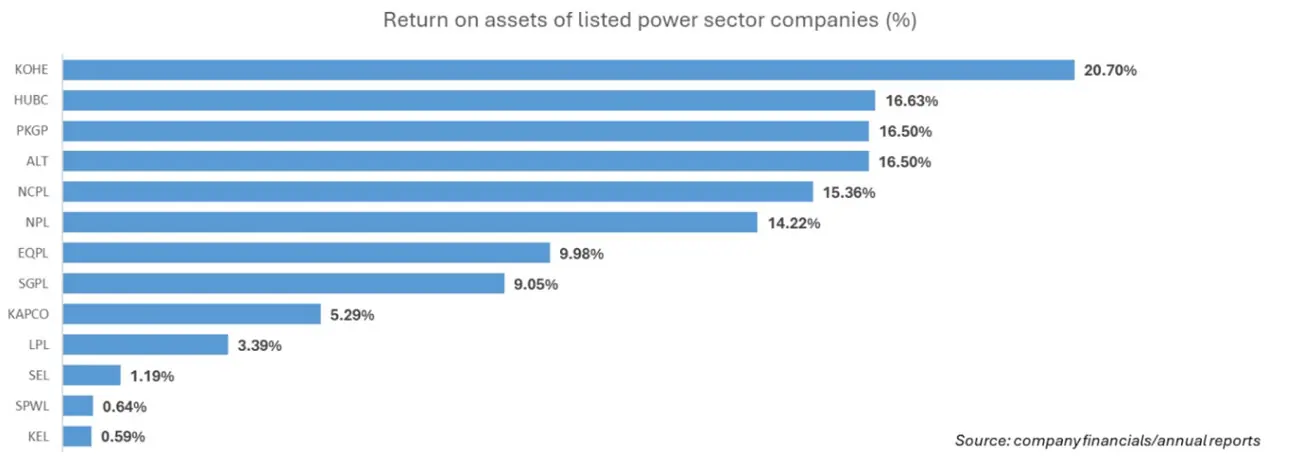

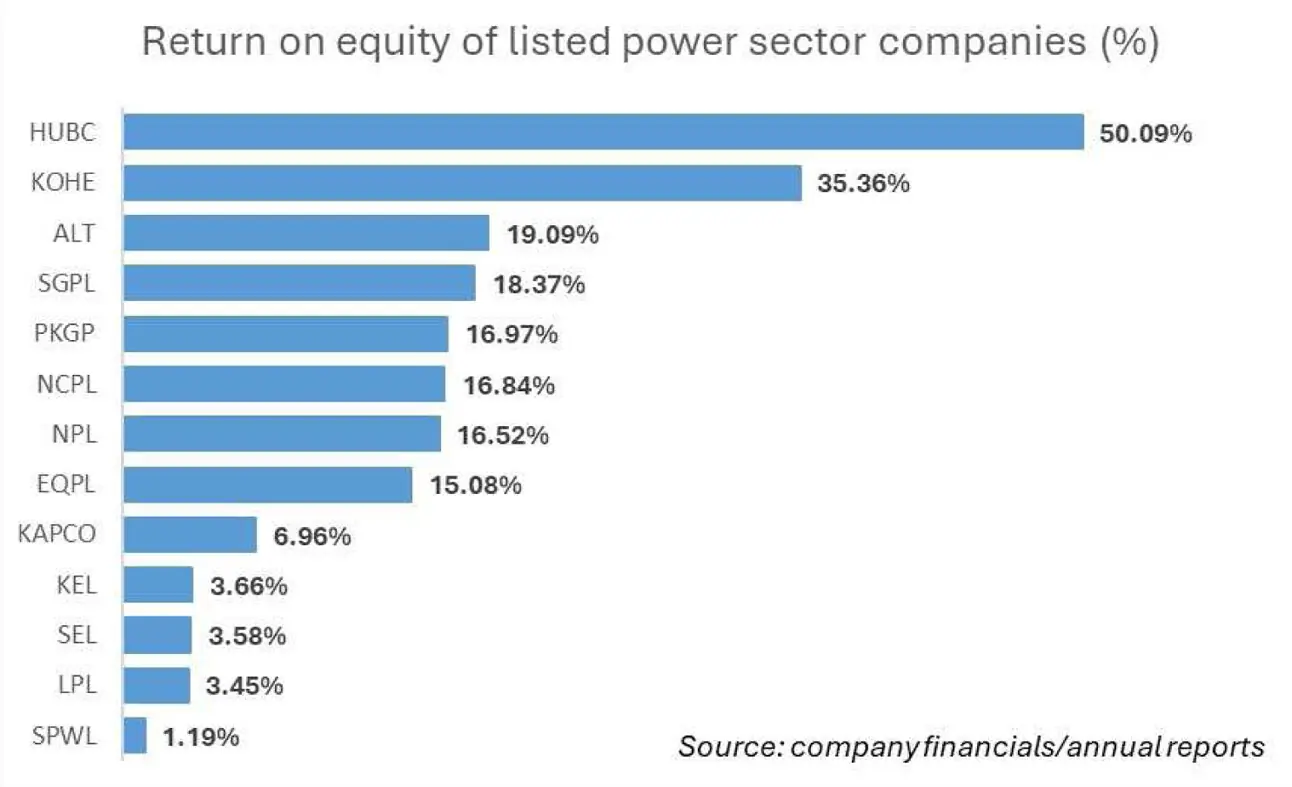

Let’s start with power producers who deal with the government. Engro Powergen Qadirpur offered a dividend of Rs 9.50 per share to its investors for the half-year that ended June 30, 2025. For a share price hovering around Rs30, the dividend yield for investors is better than that of most KSE-100 companies.

The company’s total assets of Rs 15.6 billion offer an excellent case for its returns. EPQL’s profit for the six months ended June 30, 2025, was Rs460 million. In the same six-month period of 2024, it was a phenomenal Rs1.61 billion.

Kohinoor Energy Limited recorded a profit of Rs1.6 billion in FY24, which was reduced to Rs723 million in FY25. In both cases, the company’s bottomline figure is around 15-16 percent of its revenue. This is a healthy margin. Nishat Chunian Power is an even better performer, with a profit of nearly Rs 5 billion in FY24, accounting for around one-third of its revenue.

One could use other comparisons, but Pakistan Stock Exchange (PSX)-listed power producers in Pakistan have done well over the years. They have been secured by sovereign guarantees, apparently because they helped the government set up power generation units when Islamabad was desperate and offered lucrative returns that would ensure they kept their plants running. Meanwhile, the number of electricity units sold decreased from 124,628.9 GW to 109,707.85 GW between FY22 and FY24.

In such a scenario, one would be led to believe that all companies associated with the power sector would be doing well. However, the situation changes drastically when one enters the customer-facing side of the business and when the government becomes the vendor instead of the client and Pakistan’s citizens become the customers.

In such a scenario, dissecting the financials of a company like K-Electric makes for an interesting case. It was just days ago that it released its FY24 reports to the PSX.

The consolidated statement showed net revenue of Rs 557.1 billion in FY24. Still, the bottomline shows a profit of Rs 4.23 billion, which pales in comparison to the kind of earnings seen in the rest of the power sector, which deals solely with the government as its customer. KE’s profit for the whole year yielded a meager 3.6 percent return on equity, which is remarkably lower than the global or industrial benchmark typically seen with other companies. And, of course, there was no dividend.

One could argue that it may be KE’s own doing, but the rest of the DISCOs do not fare better either. Islamabad Electric Supply Company (IESCO), one of the shining beacons that the government is looking to privatize, made a measly profit of Rs6.5 billion in FY23 and a loss of Rs13.8 billion in FY22.

Remember that IESCO’s transmission and distribution loss for FY23 was 8.06 percent — the best among all that year — and yet, its financial loss due to this head was Rs 700 million. Remarkably, its recovery ratio for that year was an astounding 106.32 percent, 20 percentage points above the average for all companies.

IESCO’s accounts for FY24 have not been made public. Gujranwala Electric Supply Company (GEPCO), another one of those that is better than the average DISCO according to NEPRA’s benchmarks and is on the privatisation shelf, made a whopping loss of Rs17 billion in FY24.

The argument is simple: a power sector company that oversees millions of customers is unable to generate a substantial profit, even when it is close to regulatory standards, simply because there is not enough leeway. On the other hand, the same sector that has entities dealing solely with the government has had a joyous ride.

These companies are not random selections. They serve Pakistan’s cities, need to maintain distribution and transmission infrastructure, and are bound by regulations and compliance that ensure their earnings stay restricted. When the government decides what rates you will get electricity, what rates you can sell it, the power generation mix that will determine the tariffs, and the taxation on electricity bills, there is not much room left.

Any room left is occupied by those who still believe that electricity is a public good and should be distributed and transmitted for free. Perhaps DISCOs will earn better returns if their billions worth of property, plant, and equipment listed on their financial statements are Airbnb-ed.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.