Grid is learning to compete!

The "duck curve" persists, but overall grid demand has risen due to industrial consumers returning as gas prices increase. Solar continues to reshape load profiles, making timing and adaptation crucial for the grid's future.

- Industrial consumers returning to the grid.

- Solar's fundamental reshaping of grid load profiles.

- Time-sensitive tariffs for grid adaptation.

- Battery storage as the next major grid disruption.

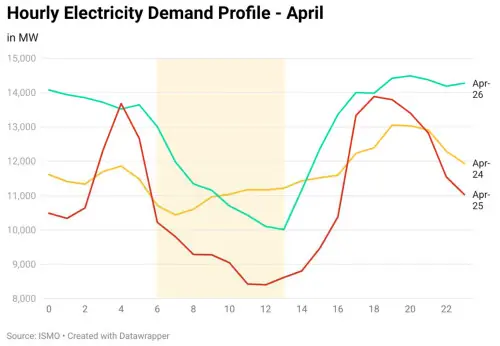

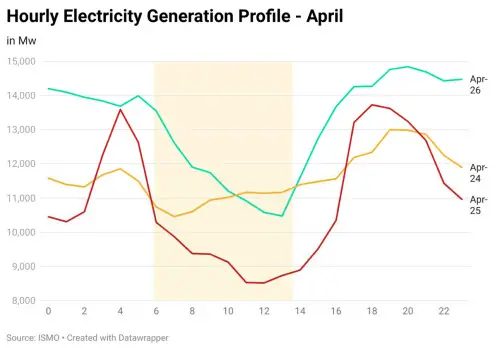

The duck is still here. If anything, it has grown older, heavier, and harder to ignore. Yet unlike a year ago, the story is no longer just about a deepening midday trough. The more interesting development is that the entire load profile appears to have shifted upward.

Grid demand in April 2026 is materially higher than the same period in the preceding years. The duck remains unmistakable, with solar generation continuing to hollow out daytime demand, but the absolute level of consumption has risen across much of the curve. That is not because households have suddenly rediscovered their love for grid electricity. Quite the opposite. The rooftop solar narrative continues to play out largely away from the grid’s line of sight, steadily chipping away at residential and commercial demand during daylight hours.

The difference this time is industry.

As gas prices for captive power have been pushed to levels that make self-generation increasingly uneconomical, industrial consumers are finding their way back to the grid. It is one of the more consequential policy shifts of recent years and, unlike many reforms, it is showing up clearly in the numbers.

Higher nighttime and shoulder-hour demand bears the fingerprints of returning industrial load. The system is carrying more energy, but it is doing so on a load profile that solar has fundamentally reshaped.

That distinction matters.

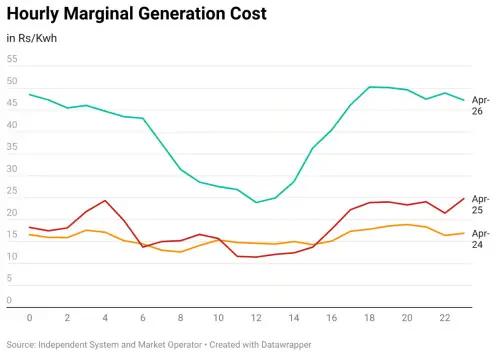

A few years ago, planners worried about insufficient demand growth. Today, the challenge is increasingly about when demand shows up rather than how much of it exists. The sun has become the dominant force determining the economics of grid operations for several hours every day. The demand curve says it. The marginal cost curve says it even louder.

The April 2026 marginal generation cost profile is a reminder that electricity pricing is no longer being dictated solely by fuel choices or plant efficiencies. Timing now matters as much as technology. The cheapest hours continue to coincide with periods of maximum solar penetration, while costs escalate rapidly as the sun sets and the system ramps to meet evening demand. The spread between low-cost and high-cost hours is becoming increasingly pronounced.

Part of that is structural. Part of it is geopolitical.

The recent volatility in international energy markets has pushed generation costs higher across the board. Wars rarely stay confined to battlefields; they eventually find their way into fuel invoices. But while external shocks may explain the level of costs, they do not explain the shape of the curve. That shape increasingly belongs to solar.

This is why the policy response over the next few years will matter far more than debates over whether rooftop solar has become “too successful.” The question is no longer whether solar is disrupting the grid. That debate is settled. The question is whether the grid can adapt quickly enough to remain the preferred platform for consumers.

The government’s proposed move towards more granular and time-sensitive tariff structures appears to acknowledge this reality. The direction is encouraging. Electricity prices that better reflect system conditions can improve utilization, flatten peaks, and reward consumption when surplus energy is available. But the details will matter. Tariff reform is only effective if consumers can clearly see and respond to price signals.

The broader principle is straightforward: the grid is now competing with the sun.

That competition should not be viewed as a threat. It should be viewed as an incentive to evolve. If grid electricity can meet or beat the economics offered by distributed solar solutions, it remains indispensable. It retains advantages in reliability, scale, flexibility, and convenience that individual systems struggle to replicate.

If it cannot, the next phase of disruption may arrive faster than many expect.

Battery energy storage systems remain expensive for mass adoption today, but the direction of travel is difficult to miss. Technology costs continue to decline globally. Performance continues to improve. The moment storage economics begin to work at scale, the conversation changes from managing daytime solar exports to managing consumers who can increasingly choose when to consume, store, and sell electricity.

The duck curve was the first warning.

Storage may well be the second.

Comments